Term sheets: striking the balance between arithmetic and chemistry!

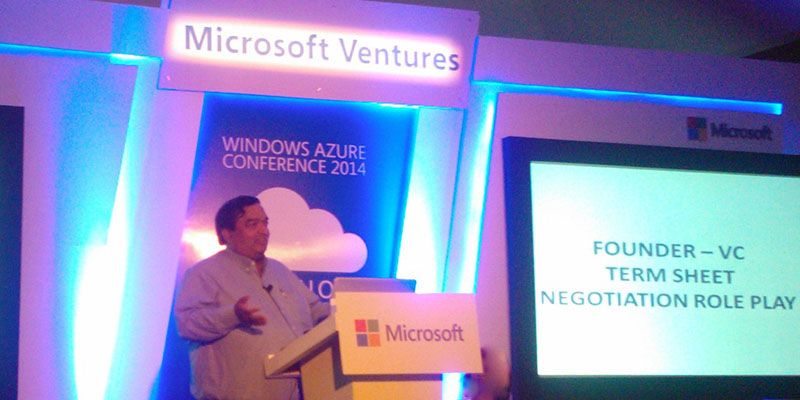

The Microsoft Ventures Startup Conclave kicked off in Bangalore on March 21 with an insightful and humorous role play on the term sheet process, which revealed the importance of getting the numbers right as well as a good working relationship between founders and investors.

It featured Ravi Gururaj, chairman of Frictionless Ventures, pitching a hypothetical music startup, and Sharda Balaji, a legal counsellor and investment advisor, as well as founder of NovoJuris; Balaji played the role of an investor.

The context

A term sheet is regarded as a non-binding preliminary codification of terms between a startup founder and an investor. It signals intent, avoids surprises and injects a sense of urgency. “It sets expectations on both sides and identifies gaps. A finite deadline is set to reach a formal agreement, failing which the two sides part ways,” explained Gururaj.

The parties

Founders enter into term sheets with investors because they are looking not just for funding but for industry connections with a player who understands the industry, and give references to customers, partners and mentors.

The investor, on their part, is interested in the startup team, market potential and disruptive defendable technology. Further down the read, the seed investor is looking to make handsome gains in future Series B and C rounds of investing.

Both sides are strongly motivated to seal a deal, and have had meetings already; credentials have been checked out from both sides.

Success tips for the startup founder

The founder must know how to make a good pitch – addressing use case scenarios, addressable market, marketing strategy and up-selling strategy. Competitive positioning and team composition should be addressed in detail.

For example, a music startup can defend its position of going after the long tail of the market with many niches, not against the big players in the main markets. “It helps if in this case you can say A.R. Rahman is your angel investor and brand ambassador of your music startup,” joked Gururaj.

It also helps to have some comparables before the founder goes into a discussion with the investor. “It’s great if you can say that you are like WhatsApp,” joked Gururaj.

Success tips for the investor

The investor should check on legal and IP issues in the startup’s domain – which can be quite tricky in the case of music startups. “Talk to the startup’s lawyers and assess the legal outlook for the domain,” Balaji advises investors.

Contention points

Typical points of disagreement between founder and investor are valuation figures, skin in the game, ESOP structures, investment stakes, tranche periods, board positions and gestation periods – quite a long list!

The founder and investor may disagree on choice of directors on the board. “Will the investor be OK if my music startup gets a board member from Sony? And will they accept the founder as chairman of the board?” asked Gururaj.

The investor also needs reassurance that the startup founder has enough ‘skin in the game’ and will not lose interest down the road. The investor will also be uncomfortable if the founder refuses to be replaced by a more professional CEO. The founding team itself should be willing to build a larger team which is strong and committed, through ESOP structuring.

Some investors prefer funding tied to performance milestones. “But founders see this as drip irrigation,” joked Gururaj – a single tranche is enough, it motivates the team and sends the right signal.

Understanding the imbalance: knowledge and experience

For any term sheet deal, founders should understand that investors have much more knowledge and experience in this domain. “VCs do this for a living, every single day – but a founder may enter into such a deal once every few years,” observed Gururaj.

Many aspiring founders are unaware early on that the investor will deduct their legal fees from investments made, and may have a say in salaries of the founders and employees. Participation rates also have different implications: 1X gives investors the full invested amount back in the event of a successful sale, and 2X will give them twice as much – followed by a further return in proportion to the equity ratio. Interest on invested funds also goes back to the investor, in addition to dividends.

“No wonder you as a founder have to master the art of sliding the bars of ownership percentage and post-funding valuation for an investor – and go for a massive Series A round,” concluded Ravi Gururaj.