TiE Bangalore business hackathon: 14 steps for startups to overcome growth barriers

TiE Bangalore recently presented a workshop for early stage entrepreneurs to help them with business hacks for rapid growth. The three-hour session featured entrepreneurs posing questions to the facilitator, innovation coach Akshay Cherian of MetaResults, who himself asked probing questions on the founders’ assumptions, tactics and business models.

A founder should know how to pitch to customers, employees and investors – each of which need a good story and proposition. Drawing on his experiences, clients and participant inputs, Cherian provided a range of useful tips to founders.

The workshop participants were founders from sectors as diverse as education and energy to leather goods and auto parts. Here are my Top 14 takeaways from the free-flowing discussion at the event.

1. Mindset > Skillset

Some startups are ‘lifestyle’ choices, and are meant for personal and professional satisfaction and not necessarily industry domination. Others are built to take off on an exponential growth trajectory, with venture funding. Some spaces are already crowded with many players, others are untapped. Even crowded spaces may have too many players with similar strategies – leaving the room open for ‘out of the box’ thinking.

Founders should therefore figure out which of these spaces and approaches is best for them. “What unique insights do I bring to the market” is a key question founders should ask themselves, advised Cherian. “Innovation is about having the guts to own a burning problem,” he added. Once you have the right mindset, the next steps are building internal and team skillsets.

2. Frame > Problem

Don’t waste your energy solving the wrong problem - learn how to ask the right questions, advised Cherian. Knowing how to frame the question and to probe repeatedly will yield useful clues on the market direction, competitive positioning and price points. For example, ed-tech startups should have clarity on whom exactly they are competing with: textbooks, teachers, or tuition centres, and who their ecosystem partners are: libraries, mobile operators or parents. “Be different from your competition, not just better than them,” Cherian said.

3. Approach > Assumption

Founders should learn how to unearth stereotypes in their industry, and question the foundational assumptions. This will open up new approaches to products and profits. This technique has been used right from the days of sugar-free sweeteners, which questioned the basic assumption that sweet taste comes only from sugar.

4. Niche > Mass Market

Drawing on Lean Startup principles, founders should begin with the most specific profile of the initial customer segment, grow this sub-niche into a niche, and only then work out a mass market angle if relevant. “First dominate a micro-niche. Start narrow. Have the courage to get focused,” Cherian urged. Many founders unfortunately make assumptions about their customers without investing time and effort in understanding their psychology. Mass market success is not for all startups; there is plenty of opportunity in niches as well.

5. Business Model > Technology

Successful startups have a good business model, and not just an innovative technology. This calls for new kinds of creativity on how to package, deliver and price offerings. For example, Cherian’s innovation coaching company uses a mix of up-front fees, money-back guarantees and post-service revenue share based on actual results delivered, thus differentiating himself from generic consultants.

6. Complaints > Compliments

You learn the most from customers dissatisfied with your offerings – and those of your competitors. A Google search on customer complaints about your competition is a terrific source of insights on what is needed, advised Cherian. “Ask yourself how you would solve these problems differently,” he said.

7. Effort > Success

Not every approach you try will work, and not every potential customer will sign up for your offering. Much has been said about having the courage to learn from failure, but this also takes a lot of effort. Sometimes the amount of effort taken to reach success almost seems disproportionate, particularly when it comes to dealing with customers who may seem clueless or irate. “Talking to customers is irritating and time consuming. Make your peace with it,” Cherian said.

8. Position > Price

Competing only on price is not a long-term strategy for success. “Discounting is a good tactic but only as part of a bigger plan,” Cherian said. Building a better moat calls for better value propositions and market positioning other than price – such as better customer service, more peace of mind for brands, and a long-term relationship beyond the immediate sale.

9. Borrowing > Inventing

At times, it is not necessary to invent everything yourself – there are a lot of great ideas out there which you can borrow and build on. Creativity expert David Murray’s book ‘Borrowing Brilliance: The Six Steps to Business Innovation by Building on the Ideas of Others,’ shows how it is possible to derive new value by borrowing, combining and enhancing the thousands of business ideas out there. (See also my review of the related books ‘Innovators’ DNA’ and ‘Steal like an Artist.’)

10. Phase > Timeline

Don’t just sequence activities, recognise the changing phases of activities. Going from ‘Zero to One’ and then from ‘One to N’ are different kinds of activities with correspondingly different organisational structure, roles, culture and performance metrics (well explained in the book ‘Startup Leadership’ by Derek Lidow). How a startup gets its first 100 customers is different from how it gets its second million customers.

11. Many tricks > One trick

Many startups fall victim to ‘one trick pony’ syndrome – they come up with one great idea but are either unable to come up with great ideas after that, or are unable to cannibalise their idea when other new ideas are discovered. A startup must have a way of building and growing a steady innovation pipeline, or a practice of ‘unrelenting innovation,’ in the words of innovation guru Gerard Tellis.

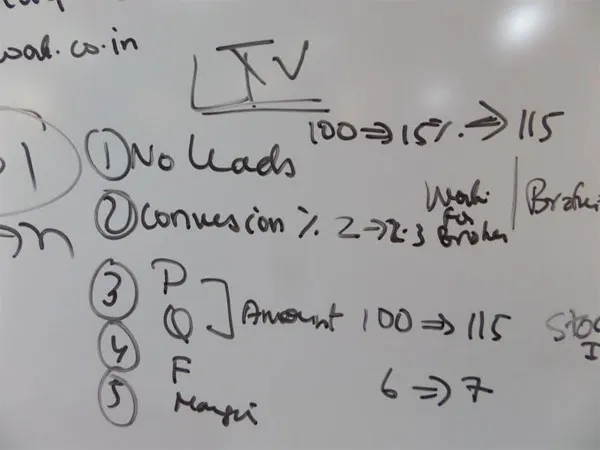

12. LTV > OTV

Many startups do not extend customer engagement beyond the first sale, and end up in a mad rush to acquire new customers. Their biggest success factor is right under their nose – the life time value (LTV) of their existing customers. LTV is a combination of number of leads, number of conversions, price quantity, frequency and margin. Increasing each of these five components by a factor of 15 per cent leads to compounding effects, and profits can double after a year, advised Cherian.

13. Learning > Education

“The Indian education system teaches you to be good employees or managers, but not how to create a new business. But that’s not an excuse for not knowing enough to start up in this day and age,” reminded Cherian, pointing to numerous free resources for founders to learn about business. These include Lean Canvas and Platform Thinking. Cherian’s company MetaResults has also published a free e-book called Great Work, a fiction format collection of three stories about the use of design thinking in the business and social sector.

14. Network > Individual

“Learn how to network with other entrepreneurs,” concluded Cherian. Many startup events offer useful guidelines and checklists for aspiring founders (see for example my startup question banks for app developers and retail entrepreneurs). Peer networks are unique for founders in the value they offer via stories and tips from fellow entrepreneurs, and also build connections that last long and deep in the startup voyage; a good example here is the Founders’ Friday Startup Mixer hosted by YourStory.