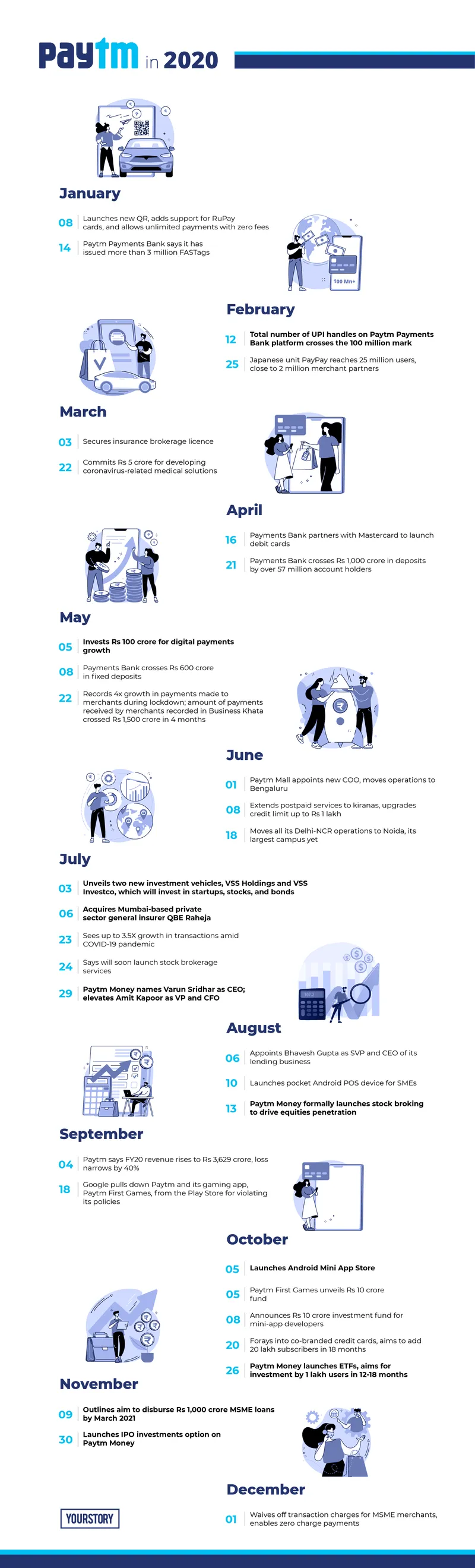

From the unbanked to struggling MSMEs, Paytm wraps up 2020 with a focus on financial inclusion

It has been a busy year at Paytm. From expanding its wealth management offerings on Paytm Money to developing an app platform in India, for India, 2020 saw the company reach new heights in the market.

2020 has been a busy year for .

Despite COVID-19, the fintech giant hit new and significant milestones in its pursuit of financial inclusion for a billion Indians. From getting deeper into the insurance sector to expanding its wealth management offerings, the company has foraged hard for domains it can expand into against the background of a global pandemic, and its efforts have paid off in this ever-changing, uncertainty-ridden world we now live in.

Paytm has said in the past - and it keeps recapitulating as often as it can - that financial inclusion is at the heart of everything it does, whether it is providing a full-stack digital savings bank account for India’s 190 million unbanked habitants, or helping 63 million MSMEs get access to institutional financial services such as loans and bookkeeping facilities.

What drove this kind of concerted effort that ultimately helped Paytm pull off the growth it did in 2020 was keeping a steady finger on the pulse of evolving consumer needs and demands, and meeting those demands in the simplest, easiest way possible while keeping its financial inclusion aim in its line of sight.

Here's a look at some of Paytm's key milestones in 2020.

Breaking new ground in wealth management

Combining the various parts of the financial world — investment banking, wealth management, insurance, personal and business banking — into one easily accessible, tech-driven and most importantly, a user-focussed application helps put the power to control one’s finances back into their own hands. And this democratisation of finance has been Paytm’s biggest firepower in 2020.

Two things that corroborate that narrative are Paytm’s launch of stockbroking services in September this year, and then its IPO investing service earlier this week.

To provide some context — investment banks and stockbrokers had long enjoyed a monopoly when it came to putting money in capital and debt markets before fintechs came along and disrupted the sector. The Goldman Sachs and JPMorgans of the world derived most of their revenue from their trading desks.

Fintechs like Paytm have helped change the meaning of wealth management and investing today by providing a heuristic approach to mutual funds, stocks, and IPO trading. They’ve also made these tools accessible to the common man, at affordable prices.

When Paytm launched its stockbroking service in September, it wasn’t the first to provide that service in India — did that nearly a decade ago. But where Paytm beats out its competitors is its ability to cross-sell products across its various assets.

For example, while for any other online brokerage, acquiring a new customer would typically cost more in terms of advertising, marketing, and onboarding dollars, Paytm manages to avoid that by targeting users on any of its various platforms. It’s cheaper for the startup to turn a kirana store owner that uses Paytm’s business app onto its wealth management platform, Paytm Money, than it would be for an online stockbroking platform to add a new user.

Also, it’s easier for Paytm to shop around its offerings beyond metro or urban areas because it has already built a strong base in lower-tier cities — a first-mover advantage that many up and coming fintechs don’t have today.

By allowing users to invest in stocks, Paytm has helped the common man become part of the economy’s growth story, and with IPO investing, a part of a company’s growth story.

Bolstering the SMB sector

Paytm stepped up when it came to supporting SMBs facing existential crises due to the pandemic — whether it was launching an Android all-in-one POS machine that enabled contactless payments, or helping them access quick loans devoid of predatory interest rates.

In December, the fintech startup announced that it would waive off all charges on merchant transactions. Essentially, merchants will no longer have to pay anything to accept payments from Paytm Wallet. Additionally, Paytm said it will absorb Rs 600 crore in MDR (merchant discount rate, a fee paid by merchants to their banks for allowing them to accept digital payments) to support MSMEs and help free up capital they can use to expand their businesses.

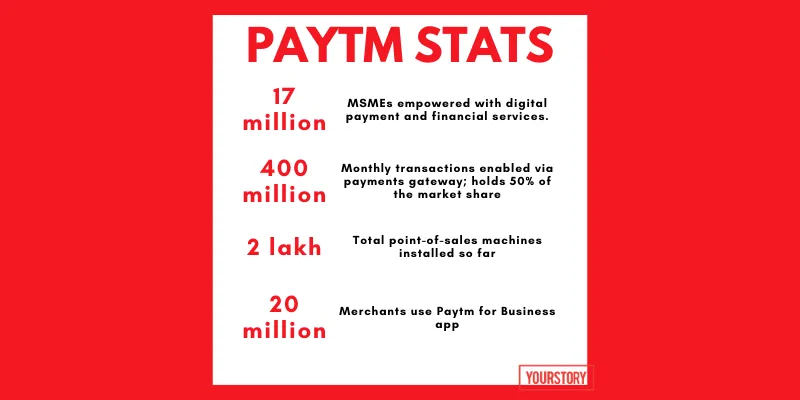

Paytm’s various initiatives to help the SMB sector successfully navigate the pandemic is expected to benefit more than 17 million merchants in its ecosystem. By March 2021, the startup has said it aims to disburse Rs 1,000 crore in collateral-free loans under its ‘merchant lending programme’. For the 63 million small businesses in India, collateral-free loans is a dream-come-true because of the shortcomings of this largely unorganised sector when it comes to keeping credible, verifiable financial records.

Most loans that SMBs get from banks and informal lenders are inundated with hefty interest rates and compulsory collaterals.

Growth in key numbers

Paytm reported major growth in key numbers such as the total number of users, transaction volumes and values, as well as added more new users versus 2019 — starkly antithetical to its peers, as well as others in the startup community.

The startup has handled 100 million UPI transactions this year, 350 million wallet transactions and added 60 million more bank accounts, official data from the company showed.

Revenue rose to Rs 3,629 crore in FY20, while burn rate reduced by over 60 percent in the last 18 months, Paytm said.

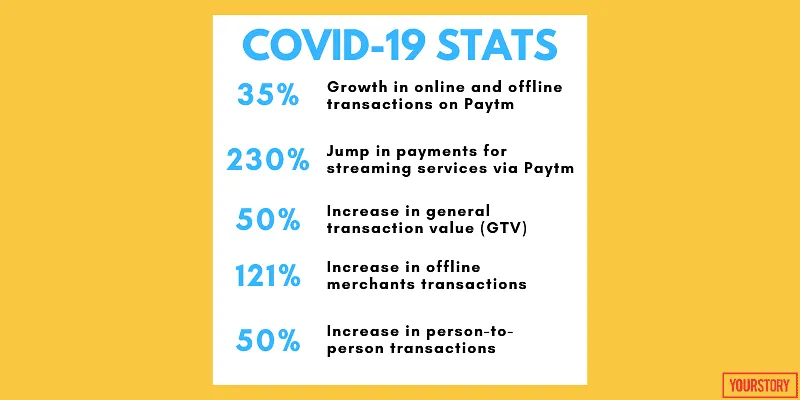

Contactless, digital payments that helped eliminate the need to handle and exchange cash also helped power the growth in Paytm’s key numbers. But an even bigger factor that accelerated the adoption of digital payment methods was the growth in ecommerce, especially during the lockdowns as everyone took to online shopping in a bid to limit contact with other people.

With its ever-expanding suite of services, Paytm is now heavily targeting the lower-tier markets where it has a considerable presence.

Super app dreams

Paytm is often touted as India’s first super app-in-the-making, and rightfully so — from financial services and online discovery platform for small, neighbourhood stores, to an ecommerce and ticketing platform, the startup does it all.

Already among the most valuable financial startups in the world, Paytm’s rapid expansion into different sectors in order to broaden its consumer base has helped it compete with Indonesia’s GoJek and Singapore’s Grab, two of the biggest super apps in the world.

With Paytm First Games, the startup’s ambitions finally came to a head. Over the last seven months of the coronavirus pandemic, the company has built a solid gaming consumer base that rivals some of the biggest players in the industry.

The launch of its Mini App Store — a platform inside the fintech giant's own app that lists applications of other companies — bolsters Paytm’s super app offerings without the company really having to develop its own logistics chain. The app platform was launched in retaliation to Google's 30 percent commission decision via Play Store billing, which was protested by a lot of Indian companies and app developers.

Paytm put up Rs 10 crore of its own money to fund mini-app developers on its platform, and has said it will distribute these apps for free on its flagship platform.

More than 300 app-based service providers such as Decathlon, , Park+, , , , Domino's Pizza, , and , among others have already joined the mini-apps programme.

With its eggs in so many baskets already, what the fintech giant gets up to in 2021 remains to be seen. A Bernstein report recently said that Paytm, along with a few other unicorns, could head for listing on an Indian bourse via an IPO next year, although Vijay Shekhar Sharma has said that he will consider an IPO after 2021, once the company starts generating cash.

Edited by Saheli Sen Gupta