Built for the ‘ineligible’: This fintech startup is providing digital credit cards to low-income individuals

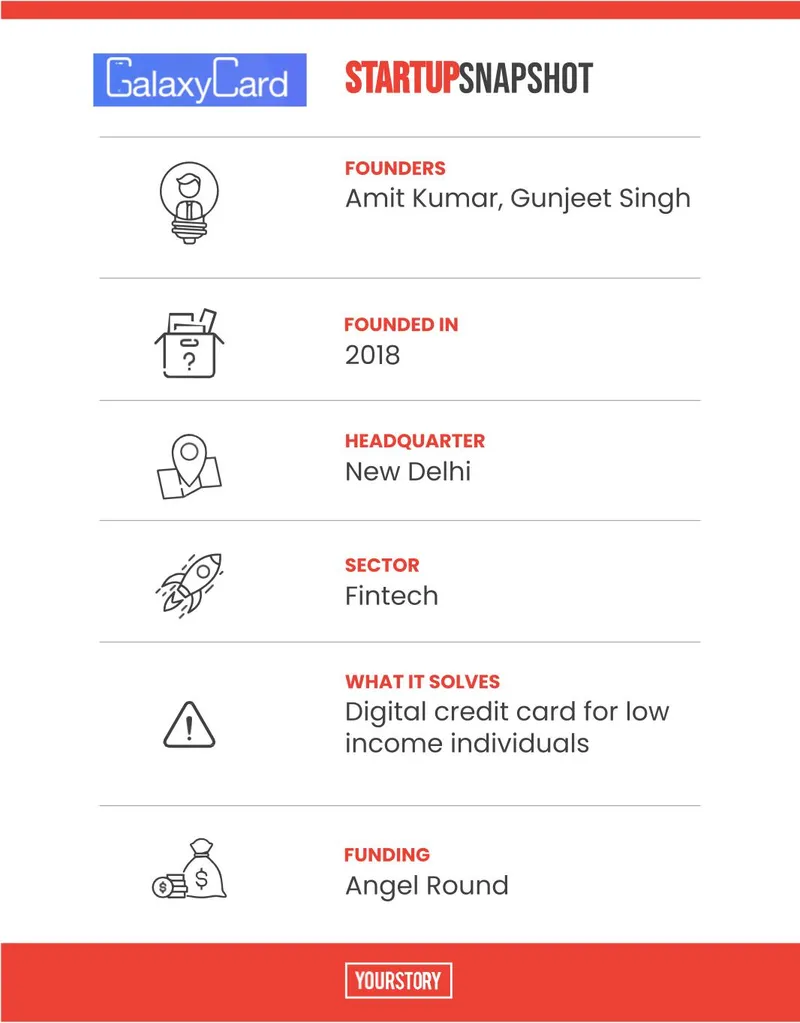

Using proprietary tech and alternative data, Delhi-based fintech startup GalaxyCard is providing instant digital credit cards for low-income individuals.

What determines the eligibility of a credit card holder? A typical bank approves a Tier I or II candidate who has a stable income of at least Rs 30,000 per month, with a strong credit score or some sort of history with financial institutions.

But what about the 400 million+ people across India’s smaller towns who do not fall under the said benchmark? Though a lot of institutions have started to dole out credit cards for lower-income segments, many continue to remain reluctant due to the high cost of acquisition, technical processes, and risk evaluation.

Moving away from age-old parameters to evaluate an eligible customer, new-age fintech startups are using alternative data and leveraging technology to create better risk profiles and offer credit.

One such player is Delhi-based GalaxyCard, which entered this space in 2018, and has managed to reach across 700 towns.

The startup provides instant digital credit cards (ticket size from Rs 1,000-Rs 25,000) within three minutes. In contrast, availing of a physical credit card from a traditional bank could take up to 4 weeks.

works on multiple channels like UPI (scan and pay), in-app services (bills payments), and even offline without a POS/swiping machine.

At present, the startup is leveraging UPI’s wide reach but plans to eventually launch its own network of vendors. It claims to have issued over one lakh digital credit cards (out of about five lakh sign-ups on the platform) to date, clocking an annual revenue of over Rs 1 crore in FY21.

By end of September 2021, it said its disbursal touched Rs 3 crore per month, which is expected to grow by about 70 percent month-on-month.

Why the traditional reluctance?

GalaxyCard is the brainchild of Amit Kumar, who had previously launched mobile-based payment application startup Eashmart, which was later acquired by PayUMoney in 2014.

Following his multiple stints as a product manager, he co-founded GalaxyCard with his friend Gunjeet Singh, who was closing down his own logistic startup Truckload at the time. Gunjeet is now working with as a business manager.

The idea began during the founders’ respective stints at their startups. Their low-income staff would often ask them for an advance on their salaries to meet daily expenses and sometimes, medical emergencies.

“The major use case for this group is to absorb financial shocks in terms of cash flow management, say bills and everyday expenses, in case their salary is delayed or their income flow is obstructed by a few days. In such a case, the only option left is borrowing from informal sources. This is what GalaxyCard is out to solve,” says Amit.

Their research revealed that for a bank, the cost of giving out a credit card is about Rs 5,000 per customer.

“When you are selling a credit card at that cost, the way of recovering this would be if somebody is spending at least Rs 30,000 per month in three years. If your income is less than Rs 30,000, how do you spend that money? It becomes an unviable business for a bank,” he explains.

The founders broke down the acquisition cost of the banks into multiple cost heads and realised that the onboarding cost was high primarily because of two reasons. One, the document correction was physical and second, they were all competing with the same 40 million target people and trying to sell credit cards to them.

When you operate in such an overcrowded market, you have to up the game and throw some rewards just to make your card attractive and hence gain a long-term revenue-earning customer for yourself.

“We thought, lets chuck out this 40 million target customer group and focus on the next 400+ million people who have been waiting for a credit card but are not being catered by the banks as they have not participated in formalised institution lending and don’t have much of a credit score,” says the founder.

The startup began by doing away with the physical onboarding, bringing down the customer acquisition cost to almost Rs 200, creating a viable business model.

The rules of underwriting too have been modified by the fintech industry, further reducing this acquisition cost using technology as everything is evaluated by the algorithm.

Analysing risk parameters with alternate data

GalaxyCard looks at multiple parameters before offering a credit card. “You cannot weigh everyone on the same scale. People are different; they come from different geographies, families, livelihoods. There is no single way to access them all,” says Amit.

Hence, looking at traditional credit scores, bureau reports, past repaying history etc., was not the solution and would not work in this case.

This paved the way for alternative data where the lender evaluates a user’s profile by looking at factors like the number of dependent family members, assets, type of social circles of a user, stability of the income, use of credit, and so on.

Based on these multiple data points, the beneficiaries are classified into different segments of risks, and are subsequently underwritten.

The whole process has been automated. Once the data is fed into the system, the proprietary tech platform, which is available in multiple languages, evaluates it and creates a risk/underwriting model for the startup. The entire process, right from signing up to the evaluation of data and credit card approval, takes three minutes.

“Simply looking at the bank statements and how much salary is earned, which has been done by banks for ages, is not enough for lending in low-income segment. Instead of looking at how much a customer earns, we look at how stable the income is and where it is being spent,” says Amit.

The founder says that more than technology, it is important to understand why a customer is defaulting or could end up late. “If you could resolve that and lend accordingly, a successful business model can be created,” he adds.

Revenue model

The startup’s revenue model is similar to what a typical bank follows, except in smaller ticket sizes. The credit limit starts from as low as Rs 1,000 to a maximum of Rs 25,000.

A user can start at Rs 1,000, and as the system gathers more data (how the money is spent, repayment time, overdue, other sources of income, dependency, etc.), the limit goes on increasing to Rs 5,000 and subsequently Rs 25,000, but remains below the total ‘steady’ income of the user.

The ‘bump up’ is based on the financial status of the user’s disciple, and is well scrutinised by the platform to keep the risks low.

“The system allows us to be vigilant. If we see the spending pattern of a credit card holder changing, the transactions will automatically get declined,” says Amit.

The users are charged a basic commission fee on credit. There is a one-time late penalty of 7-10 percent along with an interest (based on the duration of delay) on the amount overdue. There is also a one-time fee for an upgrade on the credit limit.

The repayment can also be converted into EMIs, on which the platform charges an interest.

The startup also offers add-on subscription-based products like a virtual card number (in partnership with banks), which can be used for certain online transactions. A subscription fee is charged on the same.

Multiple players, different purpose

A lot of fintech startups have erupted in the overall lending space, including P2P platforms, BNPL players, and other small-ticket loan providers. However, Amit argues that each player has its own set of differentials and a product offering based on user requirements.

“For instance, Slice recently launched a credit card of Rs 2,000, but their audience lies in people who transact online. We have multiple BNPL players, who are again going for more online audience than offline. It is a model of deferred payment and is more about connivence,” he says.

Therefore, the ultimate goal of all the players might be the same but the audience, their purpose for credit differs along with the business models.

Having said that, the startup faces direct competition from traditional banks, including HDFC (MoneyBack Credit Card), SBI (SimplyCLICK Credit Card) and ICICI (Coral Contactless Credit card), which have come up with credit cards specifically for low-income groups.

Also, a slew of startups like , Dhansamruddhi and offer simple products while BNPL fintechs platforms like , and are indirect competition to the startup, depending on customer’s requirements and usage of money.

Future outlook

Currently, GalaxyCard is focusing on team building. It has raised a funding of $5,00,000 in total from seed and angel funding rounds led by JITO Angel Network and other marquee angel investors including Gopi Latpate, Samyakth Capital, and Anant Agarwal.

The startup now plans to scale up with a target of having three lakh GalaxyCard holders in the near future.

“Until now, our major focus was on how we can scale up while not being in a position where our NPAs shoot up. We have attained a safe position in our underwriting model and are confident that our maximum NPAs would not cross the threshold that we are good with, which is quite lower than the break-even point for us. So, we are unit economics profitable there,” the founder signs off.

YourStory’s flagship startup-tech and leadership conference will return virtually for its 13th edition on October 25-30, 2021. Sign up for updates on TechSparks or to express your interest in partnerships and speaker opportunities here.

For more on TechSparks 2021, click here.

Edited by Saheli Sen Gupta