How blockchain assists banks in the KYC Process?

Everything is going digital. Be it filling up of forms, taking court dates or uploading documents for verification. NEFT, IMPS and UPIs have made financial transactions easy by just making a single click.

Yes, it is all set, but still, one thing remains. How come bank will know about the details of the gentleman or a pretty lady who has approached to open a bank account? The banks apparently do not believe in your identity till you provide an authentic document that clearly gives your entire detail. Had it been the last era, the executive from the bank would have visited the office and home to verify the details furnished to the bank by the person. But with a dawn of ever-changing technology, banks have connected themselves with the central data repository which verifies everything of a person in few seconds.

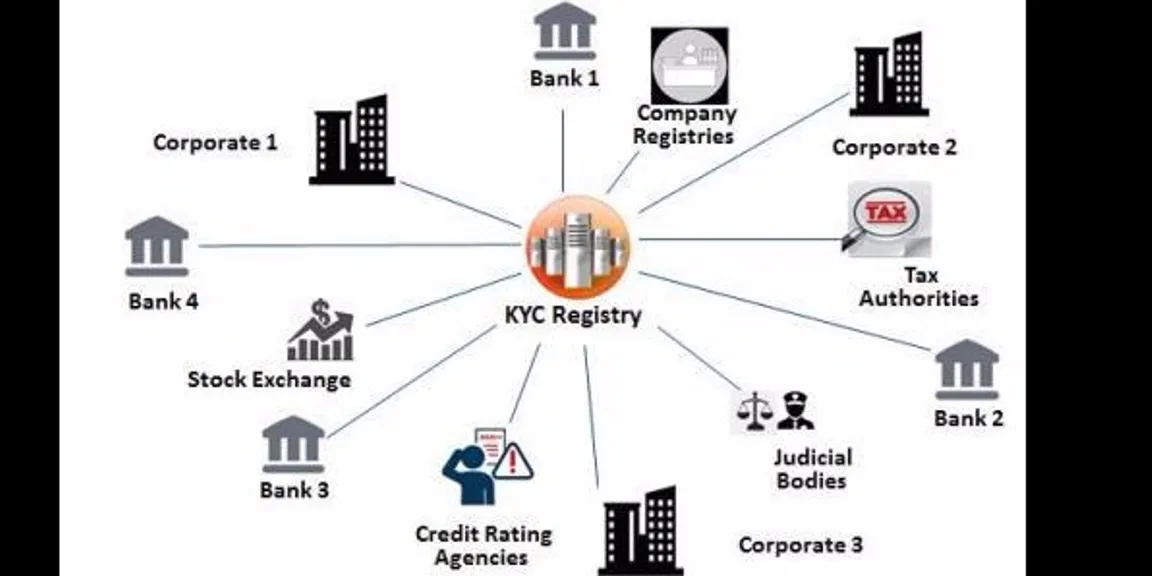

Illustration : Various Deployments of KYC Registries #

Image Src: https://www.finextra.com/blogposting/13903/kyc-and-blockchain

Provocations in Performing KYC

Performing KYC is an onerous task and takes more time than other tasks at the same par. The label of onerosity is tagged to the process because of its repetitive nature with engrossed inconsistencies. The other reason that pronounces it more difficult is a hard-nut exchange of data between internal and external disparate systems.

Extensive documents requests by the bank to the customer who has opened the account in a different bank in the same jurisdiction miffs the customer. In such case, their is no change in response to the customer.

Banks and the financial institutions are seeking the best solution for reducing the operational costs without compromising on the quality. Due to highly competitive market, the bank with advanced technology implementation shows swifter client boarding with minimum regulatory standards.

Understanding KYC and its indispensable Prerequisites – Blockchain Perspective

Before making any individual an important customer of the bank, the bank has to verify the identity of the person to ensure non-indulgence in any sort of illegal financial transactions like Financial terrorism. To get the verification done, the banks run Know Your Customer (KYC) process. Here the customer has to provide the details required to leverage the bank facilities in each Line of Business (LOB) to ensure non-involvement in Anti-Money Laundering (AML) and Countering the Financing of Terrorism (CFT).

With the implementation of the Blockchain technology, doing KYC is easier than ever as it allows the LoBs to securely share KYC details of the individuals over it. This blockchain-based secure search can also be leveraged to share customer profiles and alerts, which can trigger faulty procedures whenever required.

Blockchain – The Last Resort to KYC concerns

The banks and financial institutions prefer private-permissioned blockchains. In private blockchain, neither the trust is required nor the token is needed. The trust is achieved by signing the contracts which are published in the blockchain network for the audit trial. In a permissioned network of Blockchain specifically, one identity can read and write the information/data.

There are two ways of scope for the implementation of the Blockchain technology.

Intra Banks: The KYC performed by one bank can be used by the other branch of that bank in the same jurisdiction to make the process hassle free and continuing the services to the customer.

Inter Bank: The KYC performed by one bank can be leveraged by the other bank to make the process of opening bank account swifter. It requires the agreement between the participating banks to maintain the trust and integrity.

Financial institutions like banks have foreseen the secure future of financial transactions in the blockchain technology. Many organizations have started providing Blockchain-as-a-Service (BaaS) to ease off the process by facilitating low-cost, rapid and fail-fast systems. The entire system is backed-up by a cloud-platform following the compliance required in the industry.

References:

https://azure.microsoft.com/en-in/solutions/blockchain/

https://securityintelligence.com/why-blockchain-as-a-service-should-be-on-your-radar/

https://stratumn.com/pdf/use-cases/KYC.pdf

https://www.linkedin.com/pulse/kyc-blockchain-rajesh-kumar

https://www.westpac.in/media/12714/faq_on_kyc___aml.pdf