Was 2016 truly the year of Indian financial technology services?

Investments in fintech doubled. Lending startups saw three times more inflow of funds. But it seems 2017 may not be just the year of payments, despite demonetisation.

While you might be tempted to dispute it, most would agree that the past year has seen a lot of drumming around the financial services space. However, a great chunk of it was for initiatives whose groundwork had been laid years ago and which now seem to be reaping the benefits.

For example, the year kicked off with the grand launch of the Unified Payments Interface (UPI) in February, which rides on the Immediate Payment Service (IMPS) infrastructure, whose framework was laid a couple of years ago. Also worthy of note is the India Stack, which actively came together to unleash its potential with the launch of UPI.

Launched by the National Payment Corporation of India (NPCI), the UPI allows you to make payments using your mobile phone as the primary device for transactions, through the creation of a ‘virtual payment address’, an alias for your bank account.

And at the end of the year was the recent announcement of demonetisation, which gave payment service providers the biggest used-case in the history of the country for the subscription to digital payments.

It seems that there hasn’t been a better time for financial services startups . Indian payment majors like Paytm have already claimed that they are en route to achieving goals originally set for 2020 by next year.

But with the rising buzz, was this zeal reflected in the investment flow into the Indian fintech segment?

The investment scenario

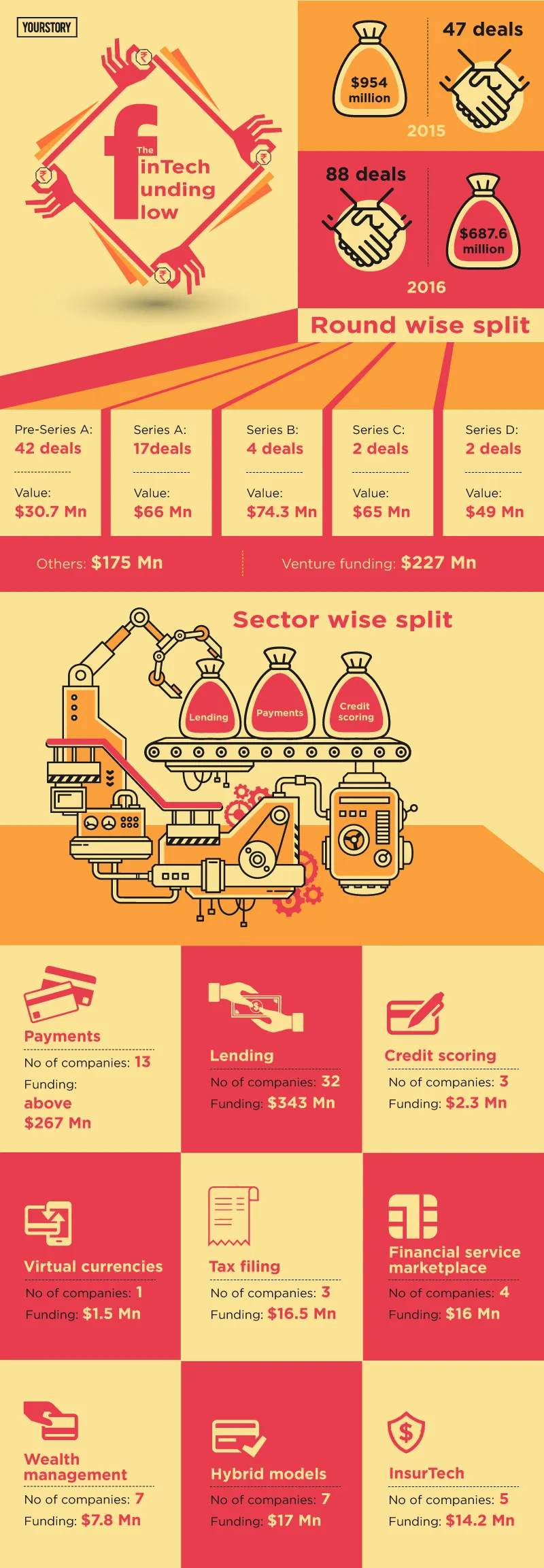

According to YourStory Research, the Indian financial startup ecosystem saw more than $687 million poured into the space across 88 deals. This may seem low when compared to 2015, for which investment stood at $954 million across 47 deals, however, one needs to understand that a large chunk of that amount, close to $575 million, was Alibaba-backed Ant financial Services Group’s investment in Paytm’s parent company, One 97 Communications.

So, if the massive Paytm deal is left out of consideration, investment in the Indian fintech scene has risen by over $300 million, an 81 percent rise across sectors.

Further dissecting the investments, one sees that there were 42 pre-Series A deals closing an approximate $30.7 million; 17 Series A deals amounting to $66 million; four Series B deals amounting to $74.3 million; and two Series C and Series D deals, raking in close to $65 million and $49 million respectively.

Venture contributed to $227 million, while other deals, whose rounds weren’t disclosed, contributed to $175 million of the total funding.

Where is the money going?

On diving deeper into the sub-sectors of Indian fintech, one sees that the results aren’t extremely surprising.

Payments and Lending continue to be the forerunners in receiving attention from Indian investors, with multiple other hybrid business models emerging in the financial space.

Here’s a look at how the sub-sectors have fared in terms of funding:

Payments

No. of companies funded in 2016: 13

Funding in 2016: above $267 million

Funding received in 2015: $725 million (including One 97 Communication’s $575 million funding)

Average round size in this sector:

Pre-Series A: slightly above $1 million

Series A: $3.4 million

Series C: $32.5 million

This year, Indian payment majors like Paytm and MobiKwik both raised funding from Taiwanese semiconductor company MediaTek.

Investment in both these companies formed a major chunk of the investment in this sub-sector, raking in almost $150 million together.

The other known startups that raised funding this year were payment solutions and platforms JusPay and TransServe, online payment gateways RazorPay and CCAvenue, as well as cross-border payments service Remitware Payments.

But 2016 showed that payments isn't the only equivalent to fintech investments.

Lending

The Lending category has seen various new business models come into play, including peer-to-peer lending, micro-loans, crowd-funding (sourcing), and even capital provision for SMEs. There has also been a great deal of activity around the theme of financial inclusion.

No. of companies funded in 2016: 32

Funding in 2016: above $343 million

Funding received in 2015: approximately $124 million

Average round size in this sector:

Pre-Series A: approximately $1.45 million

Series A: approximately $5.1 million

Series B: approximately $18.5 million

The rise of digital payments has led to an outburst of lending startups in the ecosystem. Clearly, lending seems to be king, with the investments in this space almost tripling when compared to last year. And with the recent demonetisation, there seems to be no stopping the advance of the segment.

Even banks see a rise in credit in the coming few months, in spite of being hit in the immediate aftermath of demonetisation.

In fact, 2016 saw the Reserve Bank of India (RBI) also introduce a discussion paper, with inputs from industry players, charting the future course of action for the P2P lending market.

There has also been a host of startups getting funded in the SME lending space as businesses start to figure out alternate routes of funding, with the current restructuring in investments. Business models around invoice discounting for working capital have also seen some interest from investors.

Some of the key ones that seem to have been funded this year include InCred Finance, IntelleGrow and KredX (invoice discounting).

In an early interview with YourStory, fintech veteran and Managing Partner at Prime Venture Partners Sanjay Swamy said,

“The next wave of fintech companies will be coming in the credit lending space, with multiple credit-based products in the market (including credit scoring).”

The lending majors that sought funding this year were Capital Float ($25 million), IFMR Capital ($75 million in two rounds), Neo Growth ($35 million), LendingKart ($32 million) and InCred Finance ($74 million).

Credit scoring

No. of companies funded in 2016: 3

Funding in 2016: $2.3 million

Average round size in this sector:

Pre-Series A: $360,000

Series A: $2 million

The credit scoring segment is a bi-product of lending and digital payments. Further, with the rise in activity around digital payments, it is likely that we will see more such business models coming up next year.

This year saw three startups - CreditSeva, CreditVidya and DataSigns - garnering investments from Kalaari Capital, Pix Vine Capital and other angel investors.

Virtual currencies

No. of companies funded in 2016: 1

Funding in 2016: $1.5 million

Bitcoin is still a revolutionary concept in India, especially in the wake of demonetisation, with a good chunk of the population in the country just starting to understand the potential of digital payments.

This year, Bitcoin startup Unocoin raised a pre-Series A round of $1.5 million from Blume Ventures, Mumbai Angels, ah! Ventures, Digital Currency Group, Boost VC, Bank to the Future and Funders Club.

Tax filing

No. of companies funded in 2016: 3

Funding in 2016: $16.5 million Average round size in this sector:

Pre-Series A: approximately $1.45 million

Series A: approximately $12 million

Tax filing is another category that seems to be picking up in terms of the entry of new startups. Although focused on consumer filings, the major business models in this space have been around B2B tax advisory.

This year, ClearTax was at the forefront of receiving funding from investors like Sequoia Capital and SAIF Partners, receiving above $15 million in investments over three rounds of funding.

Financial service marketplace

No. of companies funded in 2016: 4

Funding in 2016: $16 million The rounds in this sector were predominantly pre-Series A, with companies like FinanceBuddha, Deal4Loans, RenewBuy (online insurance comparison marketplace) and iServe Financial Services receiving funding.

Wealth management

No. of companies funded in 2016: 7

Funding in 2016: $7.8 million

Average round size in this sector:

Pre-Series A: approximately $375,000

Series A: approximately $2.3 million

This sector also saw active investments pouring in and is expected to see a lot more disruption with the use of technology.

Key players that raised capital this year included RKSV ($ 4 million), Fisdom ($1.1 million) and investment banking platform Banker Bay ($ 2 million).

Hybrid models

No. of companies funded in 2016: 7

Funding in 2016: approximately $17 million

Average round size in this sector:

Pre-Series A: approximately $575,000

Series A: approximately $2.9 million

This was a key segments to watch, with multiple players endeavouring to find the right balance between sectors like technology, healthcare and fintech.

With the coming of demonestisation, there will surely be a rise in startups that place themselves right in between the realm of fintech and other sectors.

This year, there were startups like AffordPlan, which makes health services affordable, Active.ai, which is a conversational banking platform, and TrueBalance, which is a phone balance checking and recharging platform, raising Series A funding.

InsurTech

No. of companies funded in 2016: 5

Funding in 2016: approximately $14.2 million

Average round size in this sector:

Pre-Series A: approximately $1.4 million

Clouded majorly by pre-Series A deals, insurance technology is touted to be a promising sector for 2017. Just this week, Finance Minister Arun Jaitley announced that the category of Life Insurance was one of the biggest gainers of demonetisation.

Not included above are investments in the alternative technology firms Celerix and Sessame Software, which provide hardware accelerated technologies and core banking solutions to the finance space.

But with the number of deals rising overall, was there much logic and restructuring in fintech investments this year?

Sanjay is of the opinion that there was, and says,

This year, the bar was raised, and companies had to prove a lot more to raise investments. Mistakes and irrational funding, which happened in 2015, didn’t happen this year, and now, the bar is much more reasonable for raising funds.

So, what do the experts think?

According to Mridul Arora, Principal, SAIF Partners, 2016 has definitely been the time for Indian fintech companies. And he cites three major things happening in this space.

Firstly, from a regulatory and administrative point of view, the space seems to be building a core infrastructure that wasn’t there before. This essentially indicates the UPI and IMPS, which are basic public commodities on which businesses should be riding and benefiting.

Secondly, demonetisation has given a huge boost to digital, and Mridul believes that customers and merchants are by and large using digital mechanisms and getting comfortable with them. However, how much of that change is sustainable still remains to be seen.

Thirdly, the fintech ecosystem today has enough entrepreneurs and experience. This leaves the space in a position to thrive, with more competition and innovation.

Mridul predicts that next year will see the entry of a lot more startups in the fintech space.

When asked about the large rise in fintech startups and funding, Bala Srinivasa, Partner at Kalaari Capital, said,

India is still a country that has a large market to be penetrated in terms of financial services. This is totally unlike the West, which is focused only on changing consumer behaviour. Therefore, there is a huge potential in Indian markets for fintech startups.

Further, looking at the short-term impact, he agrees that there will be an increase in penetration of financial services, leading to an increase in baseline, hence supporting the emergence of a new normal.

But what more can we expect from fintech in 2017? And which sectors will see more attention coming their way?

Sanjay gives us an answer. He says,

- We will see UPI 2.0 coming in, and the user will have a lot more flexibility and features.

- We will have next–gen payment companies that will be experimenting more with the application of payments.

- We are also seeing early stage pickup in the wealth management space. So, we will see applications of robo-advisory also coming in.

- The top categories will be payments, lending for SMEs, and wealth management. We will also see companies leverage data from payments in a big way. Savings will be another interesting space that might have the investors’ attention.

Co-founder of Citrus Pay Jitendra Gupta seems to agree with Sanjay, and lists the three areas he thinks will see significant growth. He says,

“Lending will provide a huge opportunity to tap into next year. And consumer lending, especially, continues to be a space where nobody has been able to build scale. So we might see three or four big players coming out of there. ”

Further, he believes that there will be a lot more startups emerging in the robo-advisory space, with the wealth advisory sector overall evolving.

He adds,

If 2016 was the year of UPI adoption, 2017 will be the year of UPI build-up, with multiple companies leveraging the platform.

Meanwhile, Pranav Pai, Founding Partner, 3one4 Capital, says,

“Investments will be bullish in fintech. But models might change. The focus will be more on companies providing stock advisory platforms and financial planning product offerings, which will become more robust. SME lending will gain attention, as will alternative norms of funding and SME lending. Even models around bill or invoice discounting will become more robust.”

What will be the major trends for 2017?

While 2016 saw a rise in investments and the ascendance of new sub-sectors within the space, here are some predictions from YourStory for what we might see from fintech in 2017:

- Payment companies and digital wallets will not just do payments

We received a brief indication of this earlier this month when we saw Paytm unleashing their payments bank strategy and tying up with the UPI. Under the same, Paytm, which will become a payments bank soon, will partner with several banks to float deposits and cross-sell bank products to make money through the transactional data on its platform.

Jitendra says,

“In fintech, payments is just an entry point, with margins made on transactions being thin. In this case, sustainability becomes a huge challenge. Therefore, payments is now becoming a data play, and 2017 will see this play coming across more effectively.”

Hence, the digital wallets of the future will use data for cross-selling more financial products.

- Robo-advisory will finally hit the horizon

Although the wealth management space has been looking at robo-advisory (automating investing decisions) for a while, it will become more mainstream and facilitate users better with their investment decisions in the coming year.

- Payment sector’s e-commerce moment

With the impact of demonetisation , payment companies are getting more aggressive in the market. Paytm already had a mandate for hiring 20,000 on-ground staff this year. Hence, payment companies will get hot on hiring and marketing, as well as on building their brands.

- Lending will become the sector to watch out for in 2017

2016 has already seen three times added inflow of investments in the lending space. 2017 will see even more activity in the space, with a steady rise in data around digital payments.

More and more consumers will look to these consumer lending startups for accessing credit. Further, with startups looking at different routes of funding, invoice-discounting and SME lending will be spaces to watch out for.

- Credit Scoring will become more mainstream

As a part of the network effect, with lending rising and more data available from digital payments, credit scoring will see more activity, and more players will be resorting to innovative routes to extract data.

- Consolidations

2016 saw one of the ecosystem’s biggest acquisitions when PayU India acquired CitrusPay. E-commerce companies like Shopclues and Flipkart acquired payment platforms Momoe and PhonePe respectively.

With the heat rising, we might see a lot more consolidations in this space, owing to the maturity of the industry. And watch out! Some of this consolidation could happen in the digital wallets space.

- The entry of foreign players

With Stripe already in India, 2017 might see other payment and fintech majors entering the Indian market and tapping into its potential.

- Fintech getting a new regulatory body?

In the recently released Watal Report, constituted by the Ministry of Finance, it has been suggested that digital payments regulation be made separate from the function of central banking.

Further, it has already stated the need to update the current Payments and Settlement Systems Act. Also, the RBI earlier announced the easing of two factor authentication by card networks through login features.

Jitendra says,

Today, when the RBI makes rules, it keeps the banks in mind. So, they don’t think of payment services as widely as digital banking. Hence, this restricts the scope of innovation in the space. With the formation of a separate regulatory body, payment service providers (PSP) can do a lot more, with systemic risks being addressed.

On the other hand, Pranav comments,

The RBI will not be discharging the fintech function anytime soon. What might happen is that it might set up special committees to look into fintech and its various sectors. In the case of P2P lending regulations, the RBI set a good precedent by talking to the industry players. Hence, it might continue this, and we will see more industry participation through special committees in industry guidelines.

Hence, with digital payments being the flavour of the moment, demonetisation will surely lead to change in regulations for the fintech industry.

With old high currency notes ceasing to be legal tender, and fintech making leaps overnight, it will be interesting to see how the fintech industry matures overall.

So, what do you think? Will 2017 be the year of fintech as well?