As global car makers plan to shift to EVs, what this means for the Indian auto industry

Global data shows that around one-third of car makers will not make any internal combustible engine cars post 2025, and by 2040 this number will reach 40 percent.

In the global auto industry, transition to EVs is happening at a rapid pace. Data based on the announcements made by global OEMs show that 76 percent of global car makers have firm plans in place for their migration to EVs. Hence, there remains little doubt on the successful transition from internal combustible (IC) engines to EVs. Global data shows around one-third of car makers will not make any IC engine cars post 2025, and by 2040 this number will reach 40 percent. It is clear that this will lead to a significant change in the next 20 years. We also foresee that many OEMs, especially Japanese car makers, will advance their plans soon.

With 76 percent of the global car market shifting to electric vehicles by 2050, there remains little doubt on the success of EVs. By 2025, one third of the car market would have changed to EVs, and by 2040, this would reach 40 percent. Car majors like Toyota, Honda, and GM would have exited IC engines completely by then.

Indian market scenario:

The Indian car market is quite unique. It has been dominated by the brand at number one, and Hyundai at number two for nearly three decades now. The fight has always been for the third spot. Maruti commands a formidable 50 percent market share, while Hyundai+KIA has almost 25 percent share of the 2.5 million car market. This is the world's fourth largest car market and has been growing consistently at around 10 percent YOY prior to the pandemic.

Indian car makers’ market share 2020:

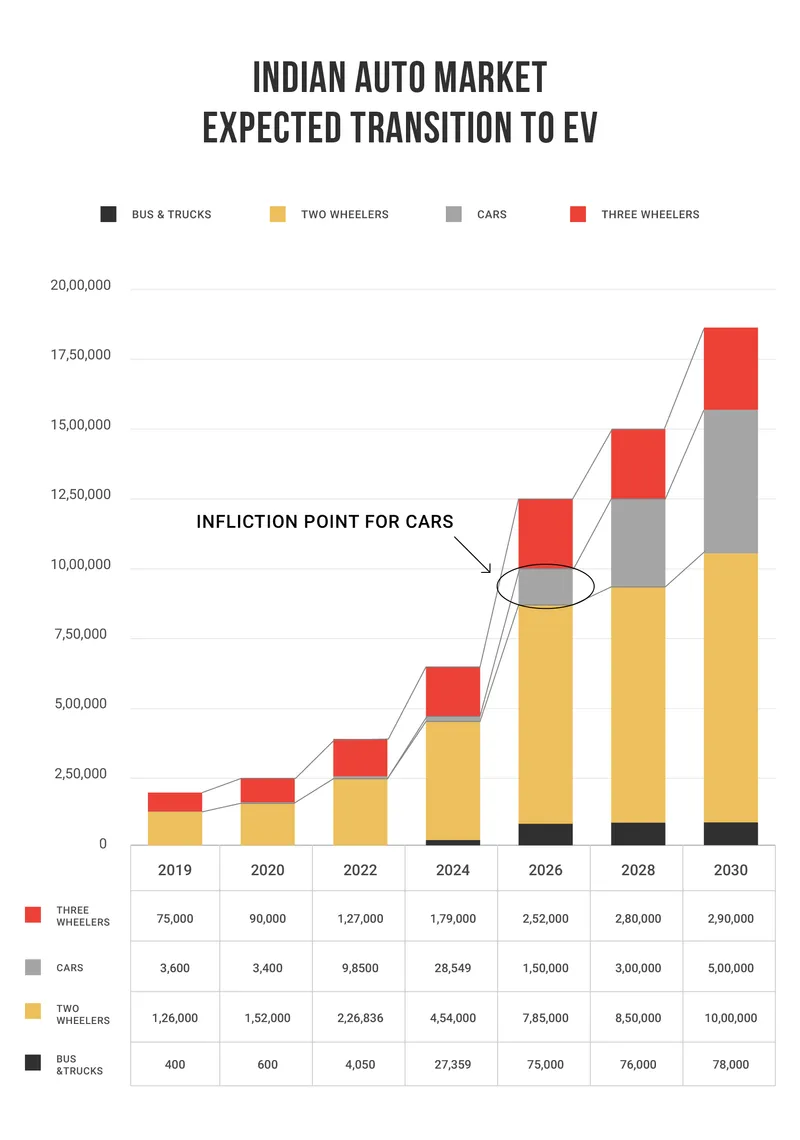

Indian car makers' EV trajectory:

In the Indian market, with Maruti Suzuki being the dominant player, they have to take the lead for any technology or product category introduction to bring scale. This has been seen in several car features, for example, auto transmission, where even today not more than 30 percent of cars have auto transmission. Since Maruti did not introduce the feature, we found that no other car maker took the lead. With Maruti and Hyundai (+KIA) commanding a lion’s share of 75 percent, it is almost impossible for other car makers to make a new category or a technology disruptor product. This is the case with EV, for now, with Osamu Suzuki publicly making a statement against EVs for India.

With EVs being a disruptive technology, there is a need for a lot of investment in the manufacturing and infrastructure segments like charging, grid metering, protocol management etc., apart from battery manufacturing. This ROI on this investment could only be realised over years of consistent volumes. It seems

Maruti Suzuki does not want to play the investor role in EV category. However, as Hyundai has already announced plans for India, we do see them taking an initiative here. With the success of Hyundai+KIA in the SUV category, they seem to have breached the impregnable wall of Maruti Suzuki. Electric cars would be attractive to them to widen this crack.

One silver lining for Indian car market though is the introduction of cars from . Tata seems to have completely taken an unexpected lead in the market by launching Tata Nexon and Tigor. Recently, there is also news of Tata coming out with a premium car with 1000 Km range.

Well, it would be interesting to see Tata again taking a shot at disrupting the market after the spectacular failure of Nano.

What could be the enablers for EVs in India:

Automotive employs a long supply chain for its manufacturing. Suppliers and their sub suppliers play a major role along with several support functions such as logistics, warehousing etc. As pull comes from OEMs for switching to EVs, the entire supply chain will get realigned to this new technology.

The following points can be summarised as enablers to the change:

a) The supply chain switch:

While Maruti Suzuki seems to be completely reluctant to introduce EVs in the Indian market, there is an argument that it shall be forced to do so by supply chain inability to support IC engines. With more than 76 percent of the world’s leading car makers already making serious plans to switch to EVs, the suppliers have begun to follow suit. We find major suppliers like , Mahle, , Magna etc. already starting to exit mainstream fuel injection and powertrain businesses. In India, most of these players are present either on their own or in collaboration with Indian partners. As they exit the IC engine businesses globally, it is definitely going to impact Indian operations as technology back up for future models will not be available. As most OEMs plan new models and platforms 5-10 years in advance, it is critical to keep abreast of technology changes. Most of the R&D and technology support to Indian entities is provided by the global R&D centres.

Hence we expect global supply chains switching to EVs to have a positive impact on the Indian EV industry.

b) Government regulations:

The Indian government has been quite consistent in tightening the emission norms for vehicles, and is expected to bring in new norms for mandatory real time emission monitoring systems in cars soon. This would make the IE engine vehicles, specially diesel ones, very tough to beat the norms as well as make them expensive. At the same time, there are incentives rolled out for EVs. This would put pressure on car makers to switch to EVs soon.

c) Unseen competition:

The EV technology is a complete disruptor. It’s a technology play with IT, battery and charging players as stakeholders. The spectacular success of has proven the point beyond doubt that technology integration is the key to success of the EV. It's just not mechanical assembly of parts any more. The car is a huge computing device on wheels. Modern electric cars have as much as 50 percent of electronics and software content in them, measured by value. As time goes by, and we have IOT, AI maturing, the software content will increase exponentially.

Therefore, it would be safe to assume we will see competition coming from unexpected quarters. Consumer electronics device makers, and technology service providers would be in the business of car making. Powered by new age technological advancements, they have a great chance of making it a success. This will surely make Maruti Suzuki rethink on their EV roll out plans.

“The Indian car industry structure is unique, with 70 percent share being held by two companies. Unless they bring out their EVs, mass scale transition may not happen. So far, only Hyundai has shown inclination to shift partially, and Maruti has taken a negative position. However, in the ever changing world, they may be proven wrong in their assessment of the Indian market EV potential”

We do see a slower transition in cars up to 2025, post that the inflection point will be reached and we will see an exponential growth. We expect the EV car market in India at 0.5 million in 2030, which would be 12 percent of the car market.

While the other formats of two-third wheelers will see a rapid transition to EVs, we are definitely going to see interesting developments in the Indian car market too. IC engines are on a short lease of life for sure.

It’s a matter of who blinks first!

Edited by Anju Narayanan

(Disclaimer: The views and opinions expressed in this article are those of the author and do not necessarily reflect the views of YourStory.)

MOST VIEWED STORIES