Taming the dragon: Should India look at all foreign investments with a hawk’s eye?

Not viewing all Chinese investments with the same hostility and defining criteria to segregate genuine investments from hostile attacks could be considered by the government; speed with clarity is a must.

Dhruv Sethi

Monday May 18, 2020 , 5 min Read

Press Note 3 of 2020, released by the Department for Promotion of Industry and Internal Trade (DPIIT), altered India’s foreign direct investment (FDI) outlook towards its prying neighbours.

With the declared objective of curbing opportunistic takeovers of Indian companies, the DPIIT revised the FDI policy to bring investments from adjoining countries under the government-approval route. It was hailed as a protectionist measure, coming close on the heels of its foreign counterparts such as Germany, Spain and Italy announcing similar measures. It was understandably instigated by People’s Bank of China shoring up its stake in HDFC Ltd.

Out of India's seven bordering nations, China's FDI contribution, as per the DPIIT's data, stands at Rs 14,846 crore between April 2000 and December 2019.

Breaking down the policy

The revised policy took a statutory form only on April 22, 2020 by an amendment to Rule 6 of the Foreign Exchange Management (Non-debt Instruments) Rules, 2019 (NDI Rules) relating to investments by persons residing outside India.

This amendment modifies the existing FDI Policy 2017 by subjecting investments from contiguous countries to government approval as opposed to an automatic route.

Taking China as the base case, this means a Chinese citizen or a corporation based in China cannot invest in India without seeking a government approval. This extends to a Chinese entity or citizen which is the beneficial owner of an investment in India.

Besides covering fresh FDIs, it prescribes government approval even when a Chinese entity/citizen acquires “beneficial ownership” of an existing or future FDI in India through a transfer of ownership, “directly or indirectly”.

Other than that, the existing stakes held by Chinese investor(s) in Indian companies remain unaffected.

For the time being, foreign portfolio investors and foreign venture capital investors from China are out of the fray.

Next steps

With fresh FDIs or transfer of existing/future FDIs requiring government screening, what follows?

The existing standard operating procedure (SOP) for processing FDI proposals notified on June 29, 2017 by the DPIIT kicks in. The investor applicant will be required to submit the investment proposal online on the Foreign Investment Facilitation Portal (FIFP) with a lengthy batch of documentation.

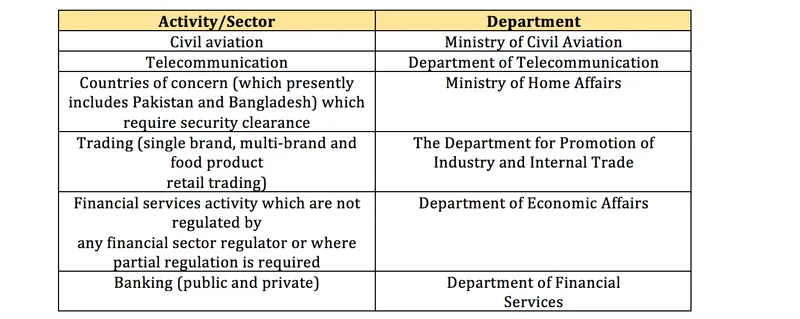

Once the proposal is filed, the DPIIT identifies the competent authority and transfers the proposal to it. For some important sectors below, the competent authorities are:

The DPIIT will also forward the proposal to the Reserve Bank of India (RBI) for comments from a FEMA perspective. The proposal will then reach the desks of the Ministry of External Affairs and the Department of Revenue.

Investments from countries of concern, presently including Pakistan and Bangladesh (though other land-sharing countries like China do not figure yet), requires the Ministry of Home Affairs’ security clearance.

All proposals are to be examined from the point of view of the prevalent FDI policy, press notes, FEMA/ RBI notifications/ guidelines issued from time to time.

By the time a decision is reached, either way, the whole process is expected to take around 10 weeks, if all goes well.

Muddy waters

Besides the layered and cumbersome approval process, the revised policy lacks clarity on the yardstick for approving or rejecting an investment proposal, leaving it to the unguided discretion of the ‘Great Indian Babu’.

Moreover, the widely-worded policy seeks to embrace subsequent rounds of funding in existing FDIs or where rights or bonus issues are being contemplated by the Indian company. Clarity is lacking on this front too.

Terms “beneficial owner” and “beneficial ownership” are undefined in the amendment to the NDI rules. The threshold limit for constituting beneficial ownership is equally wanting. Though the concept of “beneficial ownership” as defined under the Companies Act 2013 read with Companies (Significant Beneficial Owners) Rules, 2018 may come to the rescue, but the government needs to clarify that.

The Indian government’s criterion for what amounts to “indirectly” transferring ownership, which vests the beneficial ownership in a Chinese entity/citizen is equally missing. For instance, would a Spanish company (S), that is indirectly owned by Chinese company (C) or is its subsidiary, require government approval to invest in India? Perhaps, yes. Should it not be stated in clear terms?

While the amendment is introduced to Rule 6 alone, Rule 9 of NDI Rules, which permits transfer of equity instruments between two persons resident outside India, remains untouched, creating further doubts.

Need of the hour

In most sectors like e-commerce, automobile, private banking sector etc. that attracted Chinese investments, the government’s previous policy had permitted investments under the automatic route, with a sectoral cap of at least 49%.

Indian unicorns and start-ups, dependent on future funding from Chinese investors, should not be starved, if the government has decided to tame the Chinese dragon.

A speedy decision on investment proposals is, thus, key to keep Indian ventures afloat. Perhaps, not viewing all Chinese investments with the same hostility, and defining criteria to segregate genuine investments from hostile attacks may be considered. Speed with clarity is a must.

Not all is lost though. On the bright side, this revised outlook does seem like a temporary measure which only tames the Chinese Dragon, not slay it.

(Edited by Apoorva Puranik)

(Disclaimer: The views and opinions expressed in this article are those of the author and do not necessarily reflect the views of YourStory.)