Big Tech’s AI infrastructure arms race

Big Tech is locked in an AI infrastructure arms race, pouring hundreds of billions into data centres, custom chips and power in a long-term bet on competitive advantage that brings rising risks of overcapacity, energy constraints and investor scrutiny.

The surge in Big Tech capital expenditure (capex) in the AI era has highlighted a fundamental shift in the digital economy: the world of software and code is now inseparable from the hard, physical realities of power grids, cooling systems and silicon.

Innovation is no longer constrained solely by talent or algorithms, but by the number of gigawatts a firm can secure and the volume of advanced chips it can deploy.

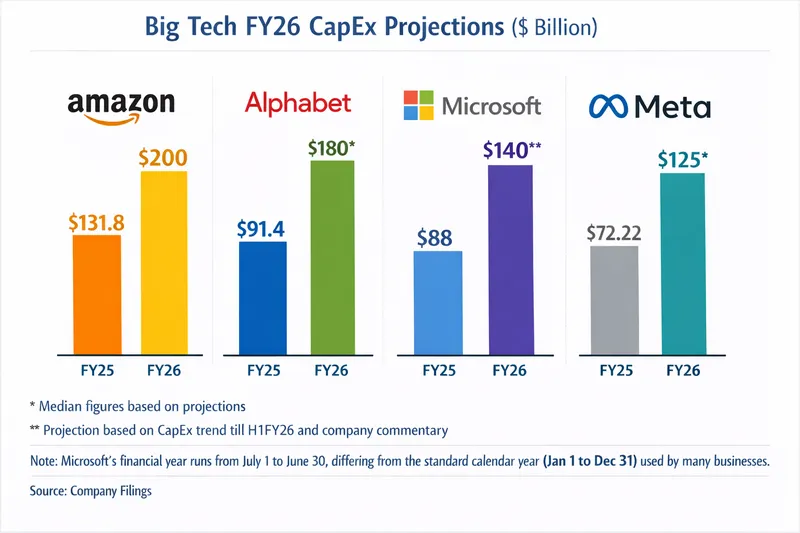

The scale of this financial reallocation is striking. Based on projections for the 2026 fiscal year, Amazon is expected to lead the group with around $200 billion in capital expenditure, followed by Alphabet at roughly $180 billion, Microsoft at about $140 billion and Meta at close to $125 billion. The combined capex of these firms is expected to exceed $600 billion.

By comparison, the consensus estimate among Wall Street analysts for the group’s 2026 capital spending stands at $527 billion, according to a Goldman Sachs Research note published in December 2025.

Alphabet and Meta’s FY26 capex figures are median projections, while Microsoft’s FY26 estimate is based on capex trends through the first half of the year and management commentary. Microsoft’s financial year runs from July 1 to June 30 rather than the calendar year.

“With such strong demand for our existing offerings and seminal opportunities like AI, chips, robotics and low Earth orbit satellites, we expect to invest about $200 billion in capital expenditures across Amazon in 2026, and anticipate strong long-term returns on invested capital,” Andy Jassy, Amazon’s president and chief executive, said during the company’s most recent earnings call.

Compute as new factory

This unprecedented spending reflects a shift in how technology executives view their business models. Data centres are no longer treated as back-end support infrastructure, but as the primary factories of the AI era. These factories produce units of machine intelligence, often measured in ‘tokens’, the basic units of AI output. Their productivity is assessed not in items per hour, but in tokens per watt, latency and utilisation rates.

The physical scale is vast. In its most recent quarter alone, Microsoft added nearly one gigawatt of total capacity to its global infrastructure footprint, highlighting the industrial dimensions of the AI build-out.

A critical nuance in this spending lies in the type of assets being acquired. Microsoft has disclosed that roughly two-thirds of its current capex is directed towards short-lived assets, primarily GPUs and CPUs, to meet immediate AI demand. The remaining third is invested in long-lived assets such as land, buildings and data-centre shells, which are expected to support revenue generation for 15 years or more.

This distinction is essential for understanding the durability of the investment cycle. While chips may need replacing every few years, the underlying power, land and buildings form a long-term foundation for the next phase of digital growth.

Silicon sovereignty

To contain costs and improve efficiency, the major players are increasingly moving away from total reliance on third-party hardware suppliers. They are pursuing what analysts describe as ‘silicon sovereignty’, the in-house design of custom AI accelerators.

This vertical integration allows companies to optimise the entire technology stack, from silicon through systems to software, improving performance while lowering total cost of ownership.

“The key metric we are optimising for is tokens per watt per dollar, which comes down to increasing utilisation and reducing total cost of ownership using silicon, systems and software,” Satya Nadella, Microsoft’s chief executive, said on a recent earnings call. He added that Microsoft had achieved a 50% increase in throughput in one of its highest-volume workloads through such optimisation.

Each hyperscaler now has a flagship project. Alphabet has introduced Ironwood, its seventh-generation tensor processing unit, designed specifically for large-scale inference. Alphabet said the chip is significantly more power-efficient than previous models while delivering a step-change in compute performance.

Amazon has said its custom chips, Trainium and Graviton, have reached a combined annual revenue run-rate of more than $10 billion, while Meta is expanding its MTIA silicon programme to support ranking and recommendation systems. Microsoft has also launched Maia 200, its second in-house AI accelerator.

By owning the silicon layer, these companies reduce exposure to supply-chain bottlenecks and can tailor hardware precisely to the needs of their proprietary models.

Infrastructure gap

The scale of the challenge extends well beyond chips. To meet global demand for computing power by 2030, data centres are expected to require around $6.7 trillion in total investment worldwide, of which approximately $5.2 trillion will be needed for AI-capable facilities, according to McKinsey & Co.

Industry researchers increasingly warn of an infrastructure gap. The binding constraint is no longer simply access to chips, but the capacity of electricity grids to support them. In some regions, the wait for a new grid connection now stretches to seven years.

The energy implications are unprecedented. By 2035, power demand from AI data centres in the United States alone could increase more than 30X, according to estimates from Deloitte. At the rack level, high-performance AI systems are expected to consume close to 1,000 kilowatts per rack by the end of the decade, rendering traditional air-cooling systems obsolete.

As a result, liquid-to-liquid cooling is rapidly becoming standard, with industry experts arguing it is the only viable way to manage the extreme heat generated by modern GPUs, while also reducing physical space requirements.

Although data centres themselves can often be built in one to two years, power plants and transmission infrastructure typically take close to a decade to complete. This mismatch is pushing hyperscalers to become energy innovators, investing in long-term renewable contracts, geothermal energy, modular nuclear designs and even carbon-capture technologies to secure reliable power supplies.

Shift towards agentic AI

Why are technology firms willing to commit such vast sums to infrastructure facing so many constraints? Executives point to the anticipated rise of agentic AI.

Agentic systems are designed to act autonomously, including planning, reasoning and executing multi-step workflows on behalf of users, rather than responding to single prompts.

“We are now seeing a major AI acceleration,” Meta chief executive Mark Zuckerberg said on a recent earnings call. “We are starting to see agents really work. This will unlock the ability to build completely new products and fundamentally transform how we work.”

Early commercial applications are already emerging. Amazon has said its agentic shopping assistant, Rufus, was used by more than 300 million customers and contributed nearly $12 billion in incremental annualised sales last year. Microsoft, meanwhile, has said that more than 80% of Fortune 500 companies are now using its tools to build AI agents, for tasks ranging from travel planning to sales qualification.

Investor scrutiny

Despite rapid technological progress, financial markets are becoming more discerning. Investors are increasingly concerned about the risk of ‘stranded assets’ if demand for paid AI services fails to grow as quickly as infrastructure supply.

While Big Tech firms possess the balance sheets to fund this expansion, they are now being rewarded or penalised based on how clearly they can link capex to revenue growth.

Alphabet, Google’s parent company, closed 2025 with what chief executive Sundar Pichai described as “a tremendous quarter”, as annual revenue surpassed $400 billion for the first time. The company also sharply increased its capital investment plans for 2026 to accelerate AI development.

Some experts argue that the sector is not yet in a speculative bubble. Goldman Sachs Research notes that current AI-related capex amounts to roughly 0.8% of GDP, well below the 1.5% peak reached during the telecom investment boom of the late 1990s. AI hyperscaler spending would need to approach $700 billion annually to match that historical extreme, the bank estimates.

“The strong balance sheets of the largest hyperscalers — and their recent willingness to deploy them — support the outlook for continued capex growth,” Goldman Sachs analyst Ryan Hammond wrote in a recent report.

Calculated gamble?

The current capex boom is ultimately a race for strategic positioning in what may prove to be the most transformative technology of a generation. It is a calculated gamble that the intelligence produced in these new factories will be valuable enough to justify the trillions spent on the silicon, steel and energy required to sustain them.

The AI infrastructure race displays bubble-like characteristics, with rapid capital flows, hype and sharp valuation swings, yet it is also anchored in genuine demand for compute. The outcome is therefore conditional, not guaranteed, and will hinge on how effectively today’s vast investments are converted into durable revenues tomorrow.

Edited by Affirunisa Kankudti