Evolution, innovation and democratisation: Trends that defined the past decade for Indian startups

In the 10 years leading up to 2020, several factors set the Indian startup ecosystem on its path to success. Riding on these factors, a few trends and developments paved the road for a new generation of startups. Here are seven key developments and trends that shaped the Indian startup ecosystem.

In the history of the Indian startup ecosystem, the period between 2010 and 2020 will be remembered as the decade of democratisation. Before this period, starting up was considered a taboo, a path filled with risk and uncertainty.

But now startups are synonymous with innovation, creativity and mass problem-solving capabilities. They are seen as a gateway to India’s dream of becoming a $5 trillion economy with technology adoption at its core.

In the past 10 years, this ecosystem ventured into unchartered territory and achieved several milestones: from boasting more than 50,000 tech startups and raising billion-dollar funding deals to India becoming the third-largest startup ecosystem, from building digital and tech infrastructure in the country to promoting women and student entrepreneurs.

In effect, the ecosystem has become the most-sought-after opportunity for marketers.

Although the COVID-19 pandemic led to a historic contraction in India’s economic growth in 2020, startups braved the storm admirably. Not only were there several technologies and research innovations, but newer strategies to build more sustainable and revenue-oriented businesses also emerged during this period.

Whether it was setting up coronavirus testing laboratories, streamlining domestic logistics or undertaking the integration of technologies at the core in minimal time, Indian startups were at the forefront of innovation, inducing a wave of democratisation in the ecosystem.

“There is no doubt that we are seeing a stronger focus on underlying business economics, both from the founders and investors; there’s also a focus on monetisation, which always got pushed to the latter years of a startup’s life,” said LetsVenture founder Shanti Mohan, “For pandemic-toughened founders, every customer contract sealed, every new user signed up has taught them that the product and value proposition comes first, everything else later.”

India saw 11 startups joining the unicorn club in 2020, with fintech company raising its valuation to $5.5 billion while spinning off as an independent entity from . The government’s COVID-19 package of Rs 20 lakh crore (US$260 billion) offered relief, particularly to MSME startups.

The ecosystem also received much-needed support from stakeholders to stay afloat. In April, independent advisors, investors, supporters and mentors of the startup ecosystem came together to launch the Action COVID-19 Team (ACT). ACT Grants, a Rs 100-crore programme, aims to seed more than 50 initiatives through grants to combat the economic fallout of the pandemic in India.

In the 10 years leading up to 2020, several factors set the Indian startup ecosystem on its path to success. Riding on these factors, a few trends and developments paved the road for a new generation of startups.

Here are seven key developments and trends that shaped the Indian startup ecosystem in the past 10 years:

From ecommerce to deep tech and space tech, the expansion of the sectoral landscape

India’s first internet startups took flight between 1995 and 2000, notably with the launch of Rediff.com (1996), Fabmart.com (1999) and (2000). But it was only with the advent of ecommerce players such as Flipkart, , and Amazon from 2010 onwards that the consumer internet ecosystem gathered pace.

At that time the Indian economy was recovering from the 2008 global financial crisis. There was also deeper internet penetration, job instability, the youth developing an affinity for technology and the entry of the Gen C (always connected) into the ecosystem. All these factors played a crucial role in laying down the foundation for India’s startup ecosystem.

Ecommerce paved the way for the growth of traditionally unorganised sectors; it also gave birth to niche categories in different domains.

For example, with more consumers shopping online, card payments and NEFT/IMPS transactions grew during 2010-2015. Doorstep delivery of products boosted the logistics industry’s prospects. What started primarily with books, stationery and electronic equipment, gradually expanded to other product categories, allied services and deeper integrations.

Between 2010 and 2015, the key sectors were ecommerce, edtech, manufacturing, health tech, automotive and enterprise tech. Closer to 2020, investor hopes rode high on sectors integrating new-age technologies such as deep tech, adtech, insurtech, media and entertainment tech, space tech, defence tech and drone tech.

“Edtech, content, SaaS, healthcare, fintech and ecommerce are sectors where we expect significant behavioural shift to fully digital solutions,” said Lightspeed India partner Hemant Mohapatra. “Even deep tech is growing quickly, with companies tackling challenging problems in AI and satellite/space tech. I feel the founder and venture ecosystem in India for 2021 will be a very, very exciting place.”

The infographic below offers a holistic view of the current sectoral landscape for internet and tech startups in India.

Image courtesy: YS Design

Outlook 2021: Given the evolution of the startup ecosystem and deeper internet penetration, Indian entrepreneurs will continue exploring more niche areas in every sub-sector. Also, during the pandemic, industry focus shifted to integrating technology at each step to streamline various processes, particularly for MSMEs, a trend that is expected to continue in the new year.

![[Year in Review 2020] A look at some of the top YourStory exclusives that made a mark](https://images.yourstory.com/cs/2/11718bd02d6d11e9aa979329348d4c3e/Story-01-1609235327649.png?fm=png&auto=format&h=100&w=100&crop=entropy&fit=crop)

Policy decisions to fuel the entrepreneurial spirit

Over the years, governments in India took several initiatives to boost entrepreneurship. However, a dramatic shift in the ecosystem occurred after the Narendra Modi government first took charge in 2014.

During 2014-2020, his government has taken several steps to encourage Indian entrepreneurs. It launched more than 50 startup schemes, introduced several laws, made policy amendments and hosted competitive events for startups to showcase their ideas. Due to these proactive interventions starting up became a viable career choice.

Also, enforcement of demonetisation, the introduction of Goods and Services Tax, initiating public welfare schemes such as setting up toilets in rural India, a focus on agriculture, attempts to make India “aatmanirbhar” as well as amended FDI policies that now require investors from countries with which India shares a land border, including China, to get prior government approval have opened up several growth and scale opportunities for Indian startups.

Here is a timeline of the key policy decisions and initiatives taken by the Modi government to boost the startup ecosystem.

Outlook 2021: With India’s economy expected to shrink nearly 10 percent in FY21, the government’s focus is on reviving growth and building the required infrastructure. It may take more decisions keeping in mind the startup ecosystem’s expectation of improved ease of doing business, friendly tax regimes and tech-focused policies.

November 2016 demonetisation, a turning point for fintech startups

The rollout of United Payments Interface (UPI) in August 2016 followed by demonetisation in November that year gave Indian fintech startups the much-needed fillip. Between 2016 and 2020, there were several developments in the sector. A few key ones are listed below:

- Rollout of payments bank, Aadhaar Pay, BHIM, QR code

- Paytm becoming a decacorn ($16 billion valuation) with international operations and an umbrella of fintech products and services

- Addition of four more fintech unicorns in the last two years: Razorpay, Billdesk, PhonePe and PolicyBazaar

- Entry of international players such as Google, Amazon and WhatsApp

- Extension of fintech business models from lending and neobanking to regtech and API-based banking as a service

- Growth in adoption of digital services across banking, insurance and wealth management sectors

- Greater adoption of technologies such as blockchain, artificial intelligence, machine learning and data analytics

**The infographic below does not depict an exhaustive list, but a few examples. The names have not been placed on basis of any criteria.

Image courtesy: YS Design

Outlook 2021: Neobanking or digital-only banking with increased adoption of cryptocurrencies will be the activity to watch out for in the Indian fintech sector. Further, the need for better security, channels to reach the masses, and deeper technology integrations will spur more collaborations and strategic partnerships.

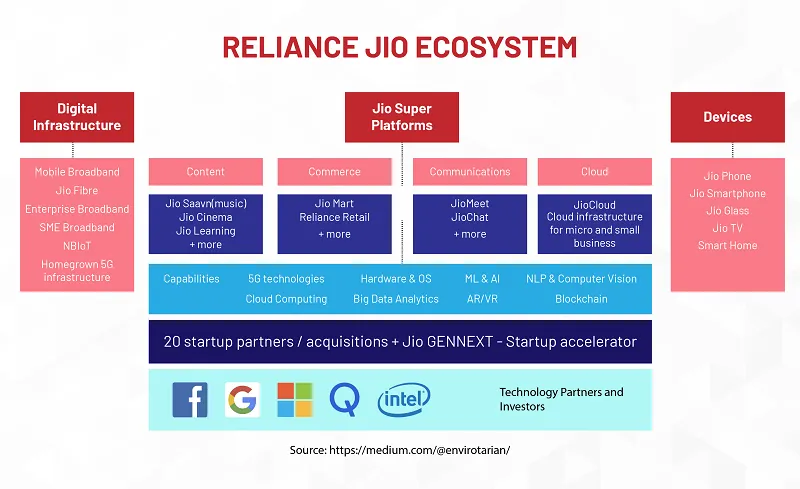

Entry of Reliance Jio, an inflexion point for India’s digital ambitions

Within 83 days of its launch in India in 2016, Reliance Jio reached a subscriber base of 50 million. Its subscriber plans included low data charges and led to deeper internet penetration in rural and remote areas.

Jio also brought the blue-collar workforce under the umbrella of digital inclusion, thus widening the market for internet startups in the country.

Today, the Mukesh Ambani-led firm has extended its arms to every corner: from broadband to OTT, communications to cloud, online commerce and offline retail, and from bidding for 5G to promoting Indian startups.

In 2020, it raised over $15 billion from technology majors such as Facebook, Google, Intel, Qualcomm and other investors.

Image courtesy: YS Design

Outlook 2021: Reliance claimed to have become net debt-free in 2020 and aims to list in the next few years. Its rise will mean more capital and support for Indian startups. At an AGM held in July 2020, Ambani invited even more startups to join forces with the company through its digital arm.

Mergers and acquisitions that changed the outlook for the Indian startup ecosystem

Until 2014, mergers and acquisitions (M&A) in India primarily revolved around conglomerates in sectors such as telecom, energy and power, financial services, manufacturing and industrials such as automotive, machinery, mechanical engineering, hydraulics, automation and controls.

Flipkart’s acquisition of Myntra at a deal value of $300-$330 million broke away from that pattern and consequently changed the perception of stakeholders towards Indian startups in terms of M&As.

Image courtesy: YS Design

The ecosystem has since seen international companies acquiring Indian startups. US-based Walmart’s acquisition of Flipkart for $16 billion at a valuation of $21 billion is the biggest such deal among Indian startups.

The rising number of M&As also made investors eye larger ticket-size funding in lieu of better exit opportunities.

Image courtesy: YS Design

COVID-19’s impact on several businesses saw startups taking the M&A route as a way to bridge gaps in capabilities rather than adopting a competitive strategy. BYJU'S acquisition of WhitehatJr was one such key deal, wherein K-12 learning got merged with skill-building.

Outlook 2021: More M&A deals are expected in the startup ecosystem to foster a collaborative rather than a competitive strategy. This will help weed out less sustainable business models and bring more innovative, personalised products and services to the market.

From M&As to IPOs, the march of Indian tech companies

In 2007, India saw the launch of 108 initial public offerings (IPOs) following the government’s efforts to liberalise the economy and encourage privatisation. However, since 2011, the numbers have fallen dramatically. The factors influencing listing activity were market volatility, political uncertainty, increase in venture-led funding and M&As gaining traction as exit routes.

2020 trends

- More tech IPOs: More internet and technology companies went public this year. Of the 22 companies that listed in 2020, three were internet and tech firms—up from just one in 2010, when MakeMyTrip made its market debut.

- More debuts on Indian markets: While in previous years, a few of the IPOs of Indian startups launched on Nasdaq and NYSE, in 2020 many big tech companies listed on Indian stock exchanges BSE and NSE.

- Reduced time period to file for an IPO: There was a time when companies took 20 years to file for an IPO; that has now narrowed to just three-five years.

Image courtesy: YS Design

Outlook 2021: Experts expect around 10 Indian startups to list in two-three years. Also, with increased adoption of technology, India is likely to see more tech IPOs in the next few years. Indian unicorns most likely to make their market debut in 2021 are Flipkart, , , , , , , , and .

Getting startup valuations right

Overvalued companies, particularly unicorns and decacorns, incurring huge losses drew a lot of criticism for years. This led to a key development over the last decade: founders diluting their shareholding that put them at risk of losing control of their startups.

The Snapdeal-Flipkart merger fiasco is a prominent example of how investors can dominate their way into a company’s business.

Image courtesy: YS Design

2020 trends

- Focus on profitability: Amid the economic fallout of the COVID-19 pandemic, metrics such as unit economics, profitability, expansion, scaling and sustainability became the benchmarks for potential investments.

- Better funding-valuation ratio: Compared to BigBasket that raised a hefty $656 million to become a unicorn in 2019, startups that joined the club in 2020 did so by raising much lower amounts. They include Nykaa ($104 million), ($208 million) and ($212 million).

Outlook 2021: India is expected to have 100 unicorns by 2025, despite the huge impact of COVID-19. Indian startups are gradually looking for investment models other than equity funding. This includes crowdfunding, revenue-based financing, venture debt and bank loans. With bootstrapped startups and turning unicorns, the new generation of startups is expected to focus on building revenues from the inception stage itself and not depend on venture capital for survival.

![[Year in Review 2020] These top 25 startup stories are sure to inspire and motivate you](https://images.yourstory.com/cs/5/80396100-2d6d-11e9-aa97-9329348d4c3e/Startups1565934694157.png?fm=png&auto=format&h=100&w=100&crop=entropy&fit=crop)

Road ahead led by democratisation

The 2010-2015 period saw the emergence of a large number of Indian startups with business models aping those of their counterparts in the West as well as back home. The proliferation of such startups led to funding distress in 2016-17 and made investors cautious.

The startups that survived and those that launched later understood the value of technology. The pandemic had the same impact, just that its magnitude was almost 10 times as much.

The past one year has not only seen the most innovative side of startups in all areas but to a large extent democratisation too. The key areas to highlight are:

Key sectors

Sectors such as edtech, OTT, digital marketing, hyperlocal delivery and services, SaaS and work-from-home tools are expected to grow rapidly. Also, MICE (meetings, incentives, conferences, events), retail and fitness will increasingly move online and flourish as initiatives to provide support to stakeholders gain traction.

According to Paula Mariwala, Founder and Co-president of Stanford Angels, the work-from-home trend has led to a shift in the workforce from large cities to small towns. Hence, workforce demographic as well as consumer profiles will change substantially. This will give rise to some new opportunities in several sectors.

Women entrepreneurs

The past 10 years have seen the rise of women entrepreneurs. According to the Makers India Report 2020, there are 297 women entrepreneurs running 285 tech startups in India, compared to 27 women entrepreneurs who ran 26 tech startups in 2010.

Many women are now actively operating their small businesses through social commerce platforms such as WhatsApp and Facebook. Home tuitions, cloud kitchens and home chefs are other business models popular with women.

Technology adoption

The biggest and most democratic trend has been the accelerated adoption of technology, say industry experts. Jio’s entry that shook up the market in 2016-17 is having a larger impact now; to some extent, analysts expect the medium-term implications to manifest from 2022 onwards.

Tech adoption and reliance have risen by a notch among the 100 million population living in metro cities. Consumers in Tier II and III cities have moved to the transacting layer and slowly but surely will become more digitized.

Most importantly, the MSME sector, which had largely resisted large-scale tech adoption earlier, is slowly crossing over.

Karan Mohla, Partner at Chiratae Ventures, sums up the trends accurately: “A true digital-first economy cannot be based on just ecommerce growth; other businesses too have to move beyond traditional practices. In large part due to the unique and challenging circumstances in 2020, these businesses adopted tech to suit their changing needs as well as those of customers.

“One of the changes in the outlook of founders is the desire to solve the large and endemic problems of India. It is very encouraging to see several experienced and high achievers from scaled startups venture out in their personal capacity to pursue these opportunities. These dynamics are an emerging trend and something that excites all types of investors. However, from an investor standpoint, these opportunities have to be understood from the first principles basis as there may not be global examples.”

(Edited by Lena Saha and Meha Agarwal)