Cashfree Payments

View Brand PublisherThe next frontier of D2C growth isn't marketing. It's the payment option not being offered

How a gap in India's payment method has been quietly capping D2C conversion rates, and what's being done to close it.

For India's D2C brands, the hardest part of growth isn't reaching customers. It's converting the ones already in the funnel. Brands have cracked discovery, poured resources into performance marketing, and built loyal audiences across channels. And yet, a meaningful share of high-intent shoppers still don't complete their purchase. Not because the product isn't right or the checkout is too slow. But because paying the full amount upfront, at that exact moment, isn't always an option.

This is the D2C EMI gap. It has been quietly capping conversion rates, suppressing average order values, and pushing brands to over-invest in acquisition to compensate for high-intent drop-off that was never inevitable.

Cashfree Payments and Snapmint are partnering to close it.

The gap UX alone can't fix

For a long time, checkout optimization was treated as a UX problem. Reduce the steps, pre-fill the details, speed up the payment flow. Cashfree Payments' One Click Checkout has been solving precisely this problem, delivering measurable improvements in conversion for D2C brands by removing the friction of re-entry and slow payment processing.

But once the UX layer was optimized, a second, deeper problem came into view. A problem that no amount of interface improvement could solve.

India has over 700 million UPI users. Yet credit card penetration remains below 5% of the population. Traditional EMI, which runs on credit cards, is out of reach for the vast majority of online shoppers. A customer who wants to buy a pair of headphones priced at Rs 3,500 but doesn't want to spend that amount all at once faces a choice that has nothing to do with the interface: pay in full now, wait for a sale, or leave.

The friction isn't in the checkout flow. It's in the payment options being offered. And this is exactly where a large portion of high-intent drop-off actually lives.

“With more D2C merchants on our platform, one thing they wanted us to solve was conversion. Our consumer research told us this was largely a UX problem, so we built One Click Checkout to solve it by personalising the checkout for their users. Once that was solved, our next challenge was to help merchants grow their business. That meant making the checkout experience complete, and affordability is what completes it. If we could give more consumers access to the products D2C brands sell through the right payment methods, we could expand the pie for our merchants. That's where our partnership with Snapmint came in,” said Nitin Pulyani, SVP and Head of Product, Cashfree Payments.

What the partnership unlocks

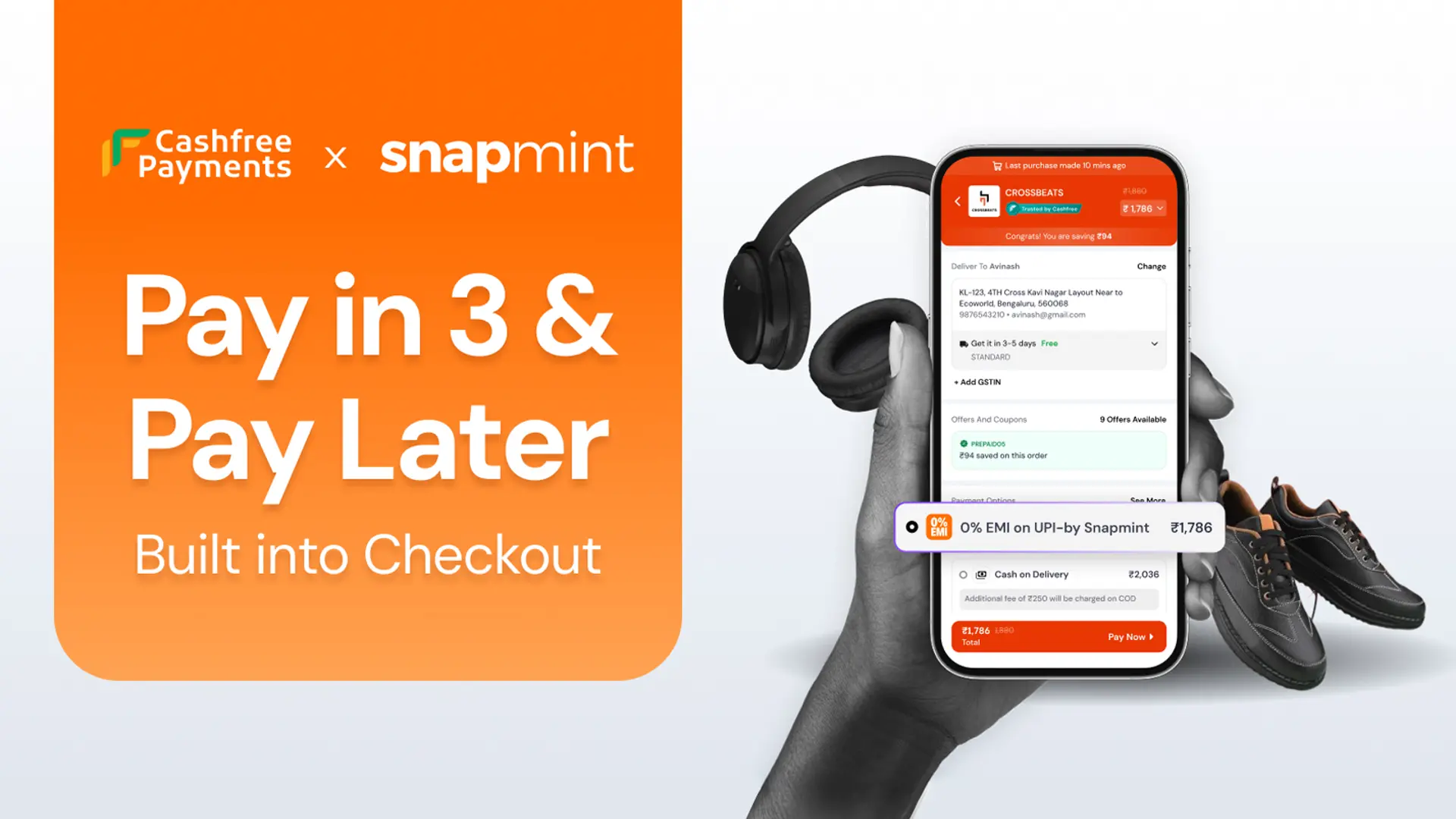

Snapmint is India's Pay in 3 and Pay Later platform, offering 0% EMI payments via UPI. It serves over 50 million users in over 2,600 cities and powers flexible payments for more than 2,000 brands. It is now natively integrated into Cashfree's One Click Checkout.

The roles in this partnership are distinct and deliberately so. Cashfree owns the checkout infrastructure, the technical layer that makes a fast, seamless purchase experience possible. Snapmint owns the EMI payment product, the consumer credit layer, and the merchant relationship on the financing side, including underwriting the entire credit risk. Merchants receive full upfront settlement; Snapmint absorbs the repayment risk entirely. The partnership works because each does what the other can't.

Through this integration, D2C brands on Cashfree can now offer their customers Pay in 3 and 0% EMI on UPI, with instant approvals and flexible repayment tenures, built directly into their existing checkout flow. For brands already using Cashfree Checkout, no front-end changes are required. Once enabled from the Cashfree Dashboard, the option surfaces at checkout automatically. The full onboarding process takes between three and five working days.

"The biggest shift we’ve seen over the last few years is that merchants no longer view payment flexibility as a finance product. They see it as a growth lever. When customers can choose how they pay, conversion, order value, and customer reach all move in the right direction," said Abhineet Sawa, Founder, Snapmint.

The buyer this partnership reaches

The customer segment this partnership reaches is one that has largely been invisible to traditional EMI products. In cardless-first India, where most online shoppers are UPI-native but credit-card-absent, payment flexibility has never been a given. Younger shoppers, non-metro buyers, and first-time credit users in Tier II to Tier V cities represent a significant and growing share of India's online shopping population. Until now, flexible payment options simply weren't built for them.

For D2C brands operating in higher-ticket categories like electronics, fashion, home, and lifestyle, this is a meaningful unlock. Price is the primary reason customers abandon at checkout in these categories. Breaking a purchase into installments removes that hesitation without requiring the customer to have a credit history or a card.

The impact for brands already using the integration reflects this. Checkout conversion has improved by 20-30%, average order values have risen by 30-40%, and return-to-origin rates for orders paid through Snapmint EMI have stayed below 2%, pointing to stronger order quality alongside higher volume.

Checkout as growth infrastructure

The most forward-looking D2C brands in India are beginning to treat checkout not as the final step of a transaction, but as a strategic layer of their growth infrastructure. The payment options a brand offers are as much a part of the customer experience as the product itself.

This shift in thinking is what makes the Cashfree and Snapmint integration structurally significant. One Click Checkout addresses the friction of re-entry and slow processing. Snapmint addresses the friction of paying upfront. Together, they build a conversion architecture that tackles the two most common reasons a ready-to-buy Indian shopper doesn't complete a purchase.

For brands that have already optimized their marketing funnels and their checkout UX, this is the next layer. Not more spend on acquisition, but a smarter conversion architecture at the moment that matters most.

The bigger picture

India's D2C market is maturing. The brands that scaled on the back of performance marketing are now looking for more durable growth levers. Checkout infrastructure, specifically the ability to offer the right payment flexibility to the right customer at the right moment, is increasingly one of them.

The Cashfree and Snapmint partnership is a bet on that idea. It treats payment flexibility not as a nice-to-have feature but as a structural requirement for converting the next hundred million Indian online shoppers, many of whom are UPI-native, credit-card-absent, and willing to buy if the experience meets them where they are.

For D2C brands still treating checkout as an afterthought, this partnership makes the case that the conversion gap they're trying to close through more marketing spend may already be waiting to be solved at the final step.