Is Zomato’s valuation justified?

New Round of Funding

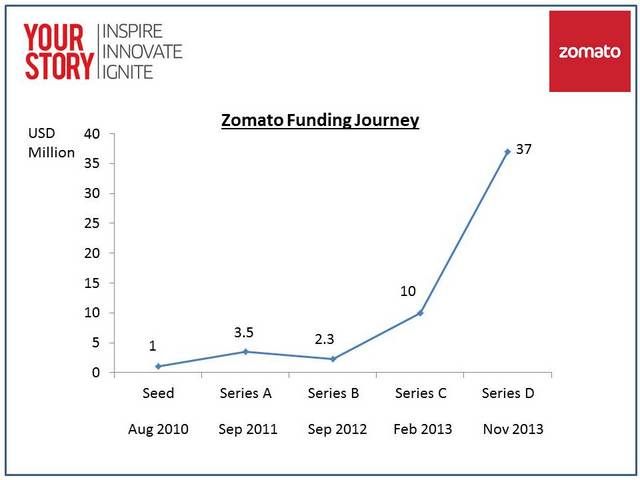

When Zomato recently raised USD 37 million from Sequoia Capital and Info Edge at a valuation of USD 161 million, it was good news for the Consumer Internet startup ecosystem in India. On average, Consumer Internet startups have a lower ticket size when it comes to investments, and to be fair, there have been very few startups that have survived for 3-4 years and reached a good scale to be considered successful. Further, a common grouse of the entrepreneur community is that the lion’s share of any VC fund in India is taken up by e-Commerce startups, leaving very little to the other sectors.

Zomato’s current state is straightforward:

- Revenues of ~USD 2 million (INR 11.5 crore) in fiscal year ended March 31, 2013

- Advertising revenues were ~95% of total revenues; the rest of the revenue was from event ticketing and restaurant booking

- Also launched a printed food guide, sold exclusively on Flipkart and is claimed to be profitable irrespective of number of copies sold, because of the prior ad sales in the guide

The projections are as follows:

- Monthly revenues are close to hitting USD 0.5 million (INR 3 crore) run rate as of now

- The funds are planned to be used for deeper expansion in Brazil, Turkey, Indonesia, UK and South Africa. Plans are also on to expand into 22 more countries over the coming 2 years

Comparisons with Yelp

For the uninitiated, Yelp is the biggest local business listing, reviews and recommendation site globally. Started in 2004, it went public in 2012 on NYSE with a valuation of USD 898 million.

- Yelp claims 100 million unique visitors while Zomato claims 15 million

- Yelp has expanded to include numerous categories including health, medical, beauty, spas, home services etc. (think of it as JustDial web), while Zomato has focused and gone deep in the restaurant listing space

- Yelp has a community / social networking feature to let users connect while Zomato has kept its focus on accurate and up-to-date listing

- Yelp has a projected 2013 revenue of USD 238 million with a valuation of USD 4.4 billion; Zomato has a projected 2013-14 revenue of USD 5 million with a present day valuation of USD 161 million

- Yelp generated ~80% of revenue from ads while Zomato generated ~95% of revenue from ads

So is the valuation of Zomato unrealistic, simply obtained as a reflection of what Yelp has been able to get globally? What justifies this high valuation? Are we missing something?

Where is Zomato better positioned?

- Given that Zomato was founded in the middle of the smartphone era, it has consistently done a great job on the mobile app, driving direct traffic to the app. Further, the app has not been monetized yet, leaving a potential rich source of revenue

- Zomato’s direct traffic has grown to reach 35% and traffic from social is 12%. Why is this important? Because Google these days aims to scrape and provide as much information on the search display page itself, in an attempt to keep the user on Google properties. This means, lesser traffic to the site from which Google pulled that data, which in turn means lesser traffic to the website which was making money through ads. Compare this to Yelp, which gets 75% traffic from Google, and you know why Yelp could be in trouble. In fact, Google had tried buying out Yelp for USD 500 million back in 2009

- Going deep in a niche – restaurants & catering in this case – across the world is a sustainable longer term bet than trying to be everything to everybody, which made Yelp lose its focus. This focus will hold it in good stead, since Google is already trying to be the biggest local listing service

Our view

- For Zomato’s valuation to be justified to a certain degree, it has to generate ad revenues quickly from the new geographies, without giving it the usual gestation period for a new market.

- The dependence on ad revenues has to be brought down from the current 95%

- The restaurant booking / lead referral fee feature has not been actively sold till now, thus contributing a tiny portion of the revenues. Presumably, it was a pilot with a select few restaurants. It can potentially expand this service to eat into the market share of the global take-away ordering service Just-Eat, which has raised USD 129 million till date and has a projected revenue run rate of ~USD 95 million.

- Ensure focus on maintaining and growing “direct traffic” that does not pass through Google, so that advertisers see value in Zomato.

- Lastly, Zomato should stay away from recommended reviews and review filtering mechanism given the low transparency in such an offering. Yelp for example is facing several lawsuits from local businesses which have accused it of “filtering” out some of the positive reviews they did not advertise on Yelp. This, despite Yelp claiming that the filtering is a curation service run by algorithm with no manual intervention.