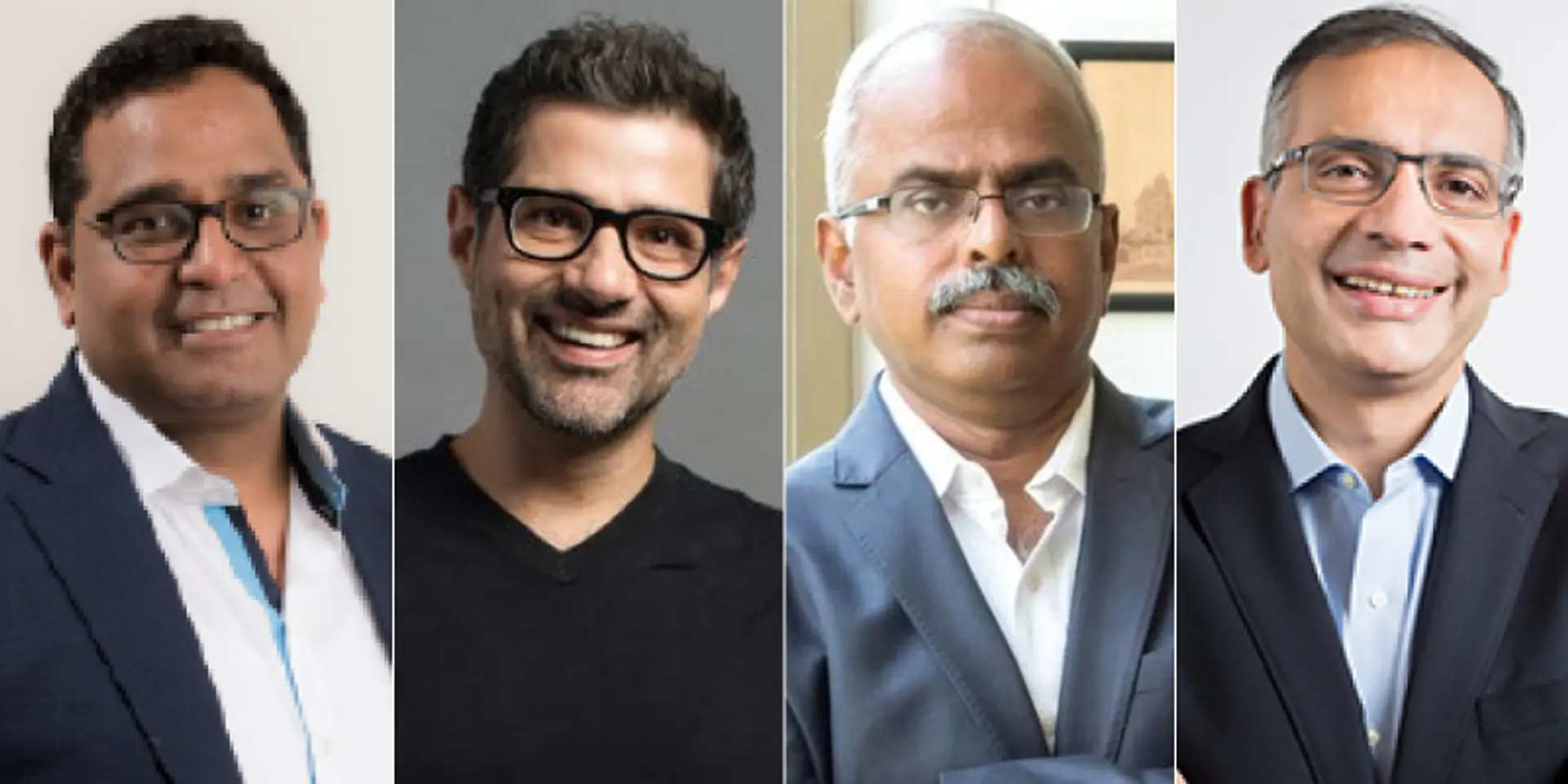

How to build a business in India - founders of Paytm, MakeMyTrip, BookMyShow, Thyrocare share their stories

Some of India’s most successful startup founders - MakeMyTrip’s Deep Kalra, Paytm’s Vijay Shekhar Sharma, Thyrocare’s Arokiaswamy Velumani and BookMyShow’s Ashish Hemrajani - share their learnings of what it takes to build, grow and sustain a business and eventually make it a wealth-creator.

Billion-dollar valuations and funding rounds of a few hundred million seem to be fast becoming the startup ecosystem’s definition of success. While it is natural to celebrate investor validation and the growth that funding enables, it doesn’t necessarily define success.

Real success lies in not just keeping a business afloat but scaling it, making it sustainable, and eventually profitable. And keeping it that way in a rapidly changing world. And that daily struggle is one that’s rarely talked about.

The blurb of the book, The Hard Thing about Hard Things, by Ben Horowitz, Co-founder of Andreessen Horowitz, one of Silicon Valley’s most respected and experienced entrepreneurs, nails it:

“While few people talk about how great it is to start a business, very few are honest about how difficult it is to run one.”

Every one of the four founders that YourStory spoke to agreed that starting up was the easy part. The rest of the journey, they said, can’t be made without a long-term vision and a serious commitment to that vision.

Beyond the spotlight and the noise around entrepreneurship, you realise that survival in a market like India, where regulations, pricing and even converting a customer, all demand one thing that entrepreneurs typically don’t have - time.

Beyond the passion, the drive, the soaring valuations and funding rounds, there is a daily struggle that demands relentless vigour, diligence and patience. Take it from those who started businesses when the word startup wasn’t cool.

So how do you build a successful business in India?

“(With) patience and diligence,” answers Deep Kalra, Founder and CEO of MakeMyTrip, among the handful of survivors of the first generation of internet companies established in India around the turn of the century.

It survived because it read the market right. “We were building online for a market that just didn’t exist,” recalls Deep, “People didn’t trust online payments and credit cards; they would look for what they wanted online and buy it offline. We then focused on the NRI market.”

The idea, he explains, is to not be patient and wait, “but to be patient and build a business based on what the market needs and requirements are”.

Deep Kalra, Founder MakeMyTrip at MobileSparks 2016The scenario was similar for another company that nearly went under in the first dotcom bust: Ashish Hemrajani’s BookMyShow, founded a year earlier in 1999. Back then, BookMyShow got more phonecalls than online bookings and was one of the few companies to allow cash on delivery.

“The toughest part has been not giving up when everyone else around you was (doing just that),” admits Ashish.

“We have survived two dotcom busts. The first time I had to look 144 people in the eye and let go of them because we couldn’t keep our business afloat. It was probably the hardest thing I ever had to do. I negotiated severance packages for them, helped them find jobs. People, your teams, your employees, and even your customers are a business’s greatest asset,” he adds.

Though BookMyShow received funding from NewsCorp in 2001, the dotcom bust saw the team whittled down to six people and shifting from a 2,500 sq ft office to a house in the suburbs. When it eventually regained traction, it became a near-monopoly (till Paytm decided to enter the event ticketing business) and is still going strong by venturing into different verticals.

While India is a market that has over 1.3 billion people, and a relatively open market at that, the Indian consumer is a tough nut to crack.

“It is important to understand that India is a land of many nations that are put together - each with its own distinct geographies, cultures, languages, and preferences. The one-size-fits-all strategy does not work here; your business has to be nimble and capable enough to adapt to the needs of each demographic you wish to cater to,” says Ashish.

Arokiaswamy Velumani, who set up diagnostics company Thyrocare Technologies in 1996, believes that in India, it takes a minimum of five years to gain initial trust.

“In the first five years, you are just convincing the market to buy your product or service. The Indian consumer doesn’t trust anything that is new,” he explains.

Velumani started up in Mumbai, a market notorious for killing businesses because of high costs. He knew that the only way to stay afloat was to grow slowly yet steadily. “We would work without salaries and never borrowed a single penny,” he points out. “There were competitors and naysayers, but the idea was to keep at it, sell to the first few customers, and get word of mouth going.”

Paytm founder Vijay Shekhar Sharma too faced a tough time in the beginning. He recalls, “I gave away 40 percent of my business for Rs 8 lakh because I didn’t know better then.”

(Where is) the ease of doing business in a complex market?

Building a business in a country with a population of 1.3 billion is challenging. It isn’t the size of the market that makes it difficult, it is the market itself. According to a NASSCOM report released last year, 45-50 percent startups die even before securing seed funding.

As of last year, India ranked 100 in the World Bank’s ‘Ease of Doing Business report.’ It may have climbed 30 spots from the previous year, but we have a long way to go. Areas like enforcing contracts, dealing with construction permits, and starting a business needing the most attention. In fact, media reports have suggested that it takes longer to enforce a contract today than 15 years ago.

‘India’s Missing Middle Class,’ an article in The Economist, said companies that have tried to tap the Indian opportunity have found that returns fell short of the hype.

“A lot of its middle class has little money to spend. There are many rich people in India, but they number in the mere millions,” the article states.

Scalability-related issues topped the NASSCOM report. Factors like low market demand and stiff competition slow nearly 49 percent of startups’ march towards building scale.

You’ve got to be in it for the long haul

And yet, these entrepreneurs did not let any of these roadblocks hold them back, at least not for long. They just believed in their vision, bet on their ideas, and built substantial businesses that have stayed relevant and are leaders in their respective verticals.

“When I started Thyrocare Technologies, there weren’t any events on entrepreneurship, no venture capital, or even startup capital. Ease of doing business was a distant dream. I started out just because I felt there was a need in the market that had to be addressed,” says Velumani.

Ashish was doing something similar – identifying a need and finding a solution to a problem. Given how slowly or rapidly the ecosystem can change in our country, he says that one of two things can happen:

“Either this solution can come ahead of its time in which case you have to be patient for the right time to come and then scale it. Or you take longer to find the solution; this means you have to work that much faster and innovate that much more to make your presence felt.”

In the case of MakeMyTrip, regulatory shifts had started by 2005 – IRCTC started opening up online train ticketing, and low-cost air carriers like Deccan Air and Spicejet started advertising flights at Rs 199 to Rs 299.

“We tied up with offline businesses because they didn’t want to sell those tickets. We were more than happy to sell those to the domestic consumers,” Deep says. Setting up travel stalls in Kolkata, Bengaluru and other cities also helped.

“This built awareness, recall, and trust. We realised that the Indian traveller needs trust and control.” While the digital revolution spelled success back then, today it also means companies can be built in a couple of years and disappear even faster.

“In that kind of an environment, it is important that you keep yourself going. Your obligation as an entrepreneur is to build a great product that will continue to keep end users happy and satisfied. That is your only obligation; the rest will follow,” Ashish adds.

That’s pretty much what Vijay Shekhar Sharma did. Paytm was not only an early mover in the digital wallets space, it also went on to become the dominant player in the sector. Its parent company, One97 Communication, how has several different verticals and the investor who held the 40 percent eventually gained a stupendous return on his investment. Today, Vijay is lauded as one of the few entrepreneurs who still holds double-digit stake in his company (reportedly valued at $12-16 billion after it raised funding from Berkshire Hathway).

“You cannot fear the big companies and give away your opportunity to someone else on a platter. If you are ready to fight the war, let me tell you there are 10x more resources available. So, if you don’t take the chance to go big, you are definitely going home,” he told the audience at TechSparks recently.

And going big means having a long-term vision Every founder/CEO will tell you one thing: businesses should not to be treated as sprints; in fact, building a business is like running a marathon. You have to be in it for the long haul.

Sleepless nights, cold sweats, tough calls, team management, getting others to believe in your vision, challenging naysayers everyday…an entrepreneur’s life isn’t an easy one. And yet, they get up every morning and move ahead with the same vigour, tenacity, and enthusiasm they had when they first started.

"My Monday mornings are as exciting for me as Friday,” says Ashish.

Velumani reportedly still lives in company quarters at Thyrocare’s headquarters. He still owns 64 percent stake in the company he founded, took public in 2016, and continues to run.

“We were frugal when we started with no money. Now that we have some money, we are more frugal,” he tells me over the phone in his trademark down-to-earth style.

In retrospect, would these founders change anything?

Deep says if he were to start the journey again, he would probably start up by getting a co-founder with complimentary skillsets: “It just makes the journey faster and easier,” he reckons.

For Vijay Shekhar Sharma, it is about trying harder and faster: “It is one life and you just need to hit harder. I wish I could do it better.” Ashish feels his journey has taught him the power of innovation: “There is a silver lining each time you fail; all you have to do is find it.”

Velumani says wouldn’t change a single thing: “I would be born in the same village, to the same poor parents, marry the same woman, and go through the same struggles of unemployment. Because if any of this changed, life wouldn’t have been this thrilling journey. I wouldn’t have had this drive.”

So, while we celebrate and laud the success of a fundraise and the birth of new unicorns, let’s not forget what it takes to run a company that is built to last.