5 ways RBI's latest data storage guidelines can impact customers and businesses

In its latest announcement, RBI disallowed ecommerce companies to store any consumers' payment details on their servers to protect unsuspecting customers from highly sophisticated cybercrimes.

Online shopping has made our lives very easy. Ecommerce offers almost everything that customers need – right at their doorsteps. The best and the most unique aspect is the convenience offered to customers at every step. Consumers don't have to keep cash or payment cards handy, as everything is just a click away.

If you are one of those shoppers, fond of shopping online, you just might need to memorise all your card details, including the 16-digit-long card number, every time you purchase something online. From January 2022 onwards, merchants such as Amazon, Flipkart, Myntra, and Netflix will not be allowed to store your payment details.

Why?

In its latest announcement, RBI disallowed ecommerce companies to store any consumers' payment details on their servers to protect unsuspecting customers from highly sophisticated cybercrimes.

What are the Impacts?

Initially, consumers and businesses will face a minor inconvenience with added layers of payment gateway. The move is likely to troubleshoot data privacy issues in the long run, with companies safeguarding consumer data with new-age technologies.

Broadly, there could be the following six impacts of RBI's latest data storage guidelines on customers and businesses:

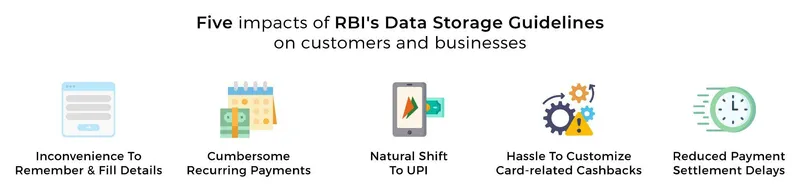

1. Inconvenience of remembering details

Since merchants won't store the consumer data, they will have to ask for card details to process the payment for every cycle. In other words, there will be a mandatory step to enter payment details to process the order.

Further, businesses will also have to do away with the one-click purchase option to comply with the norms. While this might be a major inconvenience to customers, who are now used to the transactions with just a tap, it will majorly reduce data hacking instances that we often keep hearing about.

2. Recurring payments will be harder for consumers and businesses

Consumers and businesses may face difficulty processing automatic recurring payments, especially for subscription-based services.

At present, recurring payments only require authentication through card verification value (CVV) or one-time password (OTP). Many payment gateways are developing new methods for accepting recurring payments for their existing companies.

3. A natural shift to UPI

The consumer is likely to move away from card transactions to a more seamless option like UPI for even larger payments up to Rs 2 lakh. Consumers would want an option that is faster, easier, and convenient. UPI is already a success in India and has seen an exponential rise, with as many as 2.8 billion transactions in June alone.

4. Offering card-related cashbacks would become difficult

Apart from consumer convenience, the stored consumer data also helps companies understand key demographics and offer personalised cashback.

Under the new norms, merchants won’t have access to all the payment details. Hence, they could find it challenging to curate personalised cashback offers for consumers.

5. Reduced delays in payment settlement for merchants

Every ecommerce platform has its own settlement processes, and more than often, merchants have to wait for days together for fund settlements.

The new guidelines will improve the process of seller payments by reducing the percentage of customers paying via credit and debit cards. Merchants will benefit from instant payment settlements, and the delays related to funds will reduce significantly.

The twin goals of catering to a massive online shopper and the need to ensure data security will allow the ecommerce industry an opportunity to discover the next-gen, innovative payment solutions. Businesses could leverage fintech to offer a range of payment solutions that have an added layer of security and further build a secure customer experience.

Edited by Kanishk Singh

(Disclaimer: The views and opinions expressed in this article are those of the author and do not necessarily reflect the views of YourStory.)