This insurtech startup offers an ‘insurance-in-a-box’ solution to insurers, distributors

Mumbai-based insurtech startup Riskcovry uses the insurance-in-a-box model to create a one-stop shop platform and cater to business’ digital insurance needs.

India hasn’t embraced insurance the way the sector expected the country to, largely on account of penetration and associated expenses, a lack of trust and understanding, and a gap in the claims process.

According to the India Brand Equity Foundation (IBEF), India’s insurance penetration was a mere 3.76 percent, with life insurance products at 2.82 percent and non-life penetration at 0.94 percent, as of FY20.

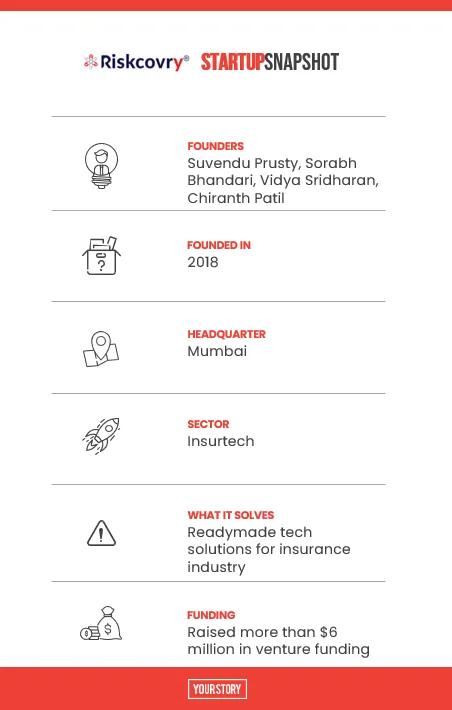

Suvendu Prusty, Sorabh Bhandari, Chiranth Patil, and Vidya Sridharan were keen to solve India’s insurance problem by offering digital infrastructure for any company to offer insurance to end users. In 2018, they launched Mumbai-based insurtech startup Riskcovry, which is essentially a 'financial infrastructure' stack for insurance distribution in India in a bootstrapped mode.

The founders, a mix of individuals with experience in the insurance, financial services, and technology industries, decided to offer an ‘insurance-in-a-box’ solution for any company, enabling “any insurance product from any insurer across any customer engagement channel”.

“Insurance is a very push kind of product and we pivoted to an idea where we become a one-stop technology shop for the distribution of these products,” says Chiranth in a conversation with YourStory.

began by presenting insurance policies in digital formats, aiming to provide curated products and “make it digitally simple for a consumer to take a decision”. The team soon realised that it was getting traction, but there was still a lot of hesitancy to buy.

Their idea was to remove all technological complexities associated with an insurance product - from the point a company comes with a policy and how it is given to distributors.

The focus area

Insurance policies are largely sold through three channels: bought directly by a consumer, via agents or distributors, or embedded with another product.

The technology platform developed by Riskcovry is in the form of APIs, which makes it simple for insurance companies to provide their products to distributors. In turn, distributors also find it easy to reach a wider set of consumers.

“We work with insurance companies to digitise their products and make them API-friendly to push into distribution,” Chiranth says.

He adds that distributors of insurance products do not want to engage with multiple tech platforms as they have to meet a lot of compliance requirements and “Riskcovry is able to provide all solutions in a single box”.

He says Riskcovry can integrate the insurance product with a distributor in a matter of days through its technology platform; previously, this would have taken months.

The insurtech startup acts as a technology integrator between the insurance company and the distributor.

“For us, every insurance product is an API that can be connected to the distributor,” Chiranth says.

The tech solution also brings in numerous benefits for the ultimate insurance policy buyer as it makes the entire process smooth.

The advantages it offers

Riskcovry’s customers range from mainstream distributors like banks, NBFCs, and brokers, to alternative players who are new to insurance distribution such as retail, payment networks, and digital, telecom, fintech, and tech startups. It claims to have around 50 clients as of now.

The advantage it offers is that all those engaged with the insurance industry do not have to invest in building technology infrastructure.

Citing an example, Chiranth says a large distributor works with multiple insurance companies and each product comes with its own set of features suited to a particular type of customers. “We can simplify all of these to make it digitally presentable to buyers,” he says.

According to Chiranth, there is a three-fold benefit for the insurance industry while engaging with them. Firstly, Riskcovry’s technology platform enables faster go-to market of insurance policies; secondly, there is better efficiency as distributors have a real-time view of how policies are being sold; and lastly, it also works out cheaper for insurance companies and distributors.

“Give us any insurance product and we can take it to the distributors using technology at lower cost,” Chiranth says.

Today, Riskcovry offers three key solutions for the insurance industry: APIs, software to manage all the data flow, and a third-party distributor licence that allows businesses to sell insurance products.

This tech startup enables the sale of around 35,000-40,000 insurance policies every month and receives a certain percentage of the premium payment for every policy sold.

Market insights and more

This close engagement that Riskcovry enjoys with insurance companies and distributors has given the team key insights into market requirements. For example, if there is a particular insurance need in the market that a distributor sees but there is no policy available, the startup engages with the insurance company to come out with such product.

“We help in insurance product discovery, commercialisation, technology integration, product-channel fit among many other things,” Chiranth says.

“We are growing at 100 percent every year as the need for insurance has increased given the pandemic and everybody wants to distribute this product digitally.”

Riskcovry has raised three round of funding, which includes a $5 million Series A round in March last year led by Omidyar Network India.

The startup, aware of the fact that insurance is a highly regulated industry, claims that high standards of data security and privacy are maintained.

The insurance market in India is quite sizeable. According to IBEF, the insurance industry is expected to grow at a CAGR of 5.3 percent between 2019-2023.

S&P Global Market Intelligence data, in a note in May last year, noted that India has the second largest insurtech market in the Asia-Pacific region next to China. Its market accounts for 35 percent of the $3.66 billion of venture capital in the sector’s region.

As part of its future plans, Riskcovry aims to go overseas. It has already launched operations in UAE, and aims to leverage its technology platform to enable the issuance of insurance products in segments where the insurance industry is yet to make a business case - roadside assistance, doctor on call, or the outpatient department in hospitals.

Riskcovry will “continuously look at adding further capability to the technology infrastructure layer” for the entire insurance industry.

“We will not only go digital but also build digital to grow digital,” Chiranth says.

Edited by Teja Lele