KarmaLife’s digital karma delivers financial services to underserved gig workers

The fintech startup drives financial inclusion for gig economy workers, offering earnings-linked credit to help meet unexpected expenses and run their day-to-day lives more prudently.

Back in 2017, when Rohit Rathi was looking for a house near his new office and negotiating the security deposit, he was surprised at the readiness with which the landlord lowered his ask after learning that Sachin Tendulkar had invested in his previous startup.

Rohit pondered the incident for a while, and then came to the conclusion that trust networks were essential for humans to navigate society. If bank X gave you a loan, bank Y was likely to give you one too.

However, these trust networks, especially in formal spaces such as banks and insurance officers, were largely absent when it came to gig workers and low-income users.

Rohit realised that formal financial institutions largely operated on a "rejection" process, where people who did not meet stringent, fixed standards, and requirements were not allowed access to the most basic of services.

He came up with the idea for a platform that was the antithesis of everything a bank or a formal financial institution stood for; a platform to cater to low-income users who did not have credit scores, bank statements, or employment contracts.

In March 2020, he, along with Naveen Budda and Badal Malick, founded , a fintech platform that caters to financially underserved populations such as gig workers, contractors, self-employed individuals, entrepreneurs, and others.

Whereas a traditional bank would look at a set of fixed parameters to offer services such as loans, and affix insurance premium rates, KarmaLife’s model is predicated on dynamicity. It follows its users' journeys, their payment behaviours, and several other behavioural parameters, and, based on those readings, extends financial services.

KarmaLife borrows from the Indian cultural philosophy of Karma, which is the law by which good or bad actions determine an individual’s future, Rohit tells YourStory.

It addresses the financial needs of gig and blue-collar workers and helps them become financially resilient and grow their incomes by investing in their futures.

Why gig workers, specifically?

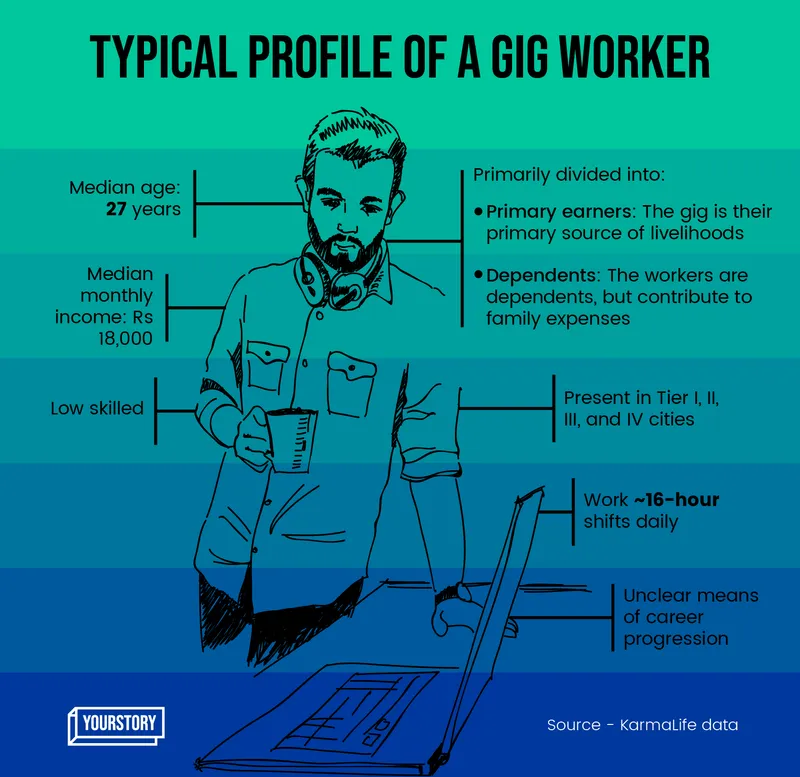

Gig workers, even though they comprise 85 percent of India’s workforce, have irregular cash flows, and any sudden expenditure can upend their stability. They don’t have access to financial products most people do, like credit cards or pre-approved credit lines from the horde of fintech apps we have on our phones.

The gig economy is also not the most regular when it comes to payouts. There are regular instances of payment delays, deferments of salaries, random cuts and additions to salaries, etc.

Banks don’t want to interact with this user base because it’s hard to underwrite them or assess how risky they are. Financial regulations prevent them from undertaking more risk than what is stipulated, and, moreover, formal institutions more often than not have pre-set criteria for different types of products and services.

For KarmaLife, these restrictions don’t really matter because the data points that it uses to understand and underwrite its customers come from their current behaviour, and not their financial histories.

For example, KarmaLife offers Earned Wage Access (EWA) — a financial product that gives people access to a portion of their salaries any time before payday; this is essentially like a small credit in the present, that is based on future earnings. This reduces the risk KarmaLife takes on its books, while also being able to provide its users access to quick loans.

A solution like KarmaLife helps this section of society access financial products not only more easily, but also more responsibly.

"We would like to be for the gig segment what a company like Cred aspires to become for the top 5 percent segment," Rohit says.

(Design credit: Aditya Ranade, Team YourStory Design)

Products and services

KarmaLife is a comprehensive fintech platform that records its users’ incomes and expenditures, as well as helps them invest.

Some of the products it offers include:

- Earned wage access

- Instalment-based loans, where the startup gives access to users who show strong repayment behaviours to multi-month, instalment-linked loans. Borrowers don’t have to worry about repaying loans immediately, and can instead split it over a few days, weeks, or even months so they still have access to liquidity.

- Digital liquid savings: For people able to save money or generate a financial surplus, KarmaLife offers to lock up the amount in an investment instrument that doesn’t require any minimum contribution, and allows one to liquidate funds on 24-hour notice.

The loans KarmaLife offers are purpose-driven or “end-use” loans, where the credit facility is extended to users only for specific purposes, like mobile phone purchases, bike repairs, purchase of essential items, medical bills, etc.

The startup is currently exploring micro-insurance products, such as health insurance and personal accident.

"We realise that finance, for anyone, is only a means to an end, and that ultimately users are best served when their core aspirations are served. Our long-term vision is to become the chosen ‘super app’ for all gig workers, so as to address all their financial and related commerce needs across their work lifecycle," Rohit says.

KarmaLife extends its services to users via partnerships with employers and aggregators of gig workers. The plug-and-play platform integrates with most HR management systems and does not require too much set-up time.

Users are started off on very small-ticket, short-duration credits, which, over time, increase based on their ability to repay.

KarmaLife’s clientele includes ecommerce, food delivery platforms, ride-sharing companies, flexi-staffing ventures, and general logistics organisations. It launched its beta with Flipkart in early 2020, and received positive feedback from the company and users who accessed the platform.

, , , and are some of its clients.

Revenue model

KarmaLife’s main business generator is earnings/wages-linked credit, and other small, short-term credit products. It lets users borrow money to cover that little period of time between the end of the month or a salary-credit cycle, and the day the salary is credited. It also allows users to borrow money during emergencies, such as medical exigencies, or auto breakdowns.

However, instead of charging a hefty interest rate on the line of credit, it levies a flat subscription fee, to be paid by gig workers availing of the loan.

(Design credit: Aditya Ranade, Team YourStory Design)

"This is in sharp contrast to interest rate models, which are complicated and cognitively taxing, or transaction-based pricing models, which tend to be ‘smoke and mirrors' as they charge higher prices for smaller value transactions," Rohit says.

The subscription fee is only levied on months when the credit is used — if a user has availed credit in January and February, but repaid it by March, they needn’t pay for the month of March.

To date, the startup says it has processed over 500,000 credit transactions, and business has grown 10X over the last nine months. Its KYC-compliant users have utilised 85 percent of the credit limit offered up until now, and its repeat rates are more than 80 percent.

Despite catering to a segment formal financial institutions generally deem 'risky', KarmaLife says its NPAs are less than 0.5 percent.

The Bengaluru-based startup raised $2.2 million in pre-Series A funding in February this year, from Artha Venture, Netgraph, LV Angel Fund, Singularity Ventures, and angel investors. Rohit says the founders are already in discussions for a follow-on Series A round this year.

Future plans and outlook

KarmaLife’s total addressable market is 100 million blue-collar gig and contract workers in India, it says. In South Asia, Southeast Asia, and the Gulf, where it wants to go next, those numbers are higher.

The startup’s ultimate goal is to become a one-stop financial ecosystem platform for gig workers with the addition of pension products, micro insurance, savings and investments, among others.

Because of the sheer volume of gig workers on the platform, Rohit envisions the product becoming something akin to a matchmaking website, where it could match gig workers looking for work opportunities with employers looking for people with specific profiles and skills.

From 7.7 million people in 2020-21, the gig workforce is expected to grow multifold to 23.5 million by the end of the current decade (2029-2030), according to a report by the NITI Aayog.

Fintech solutions like , which raised $82 million in funding from Tiger Global earlier this year, and KarmaLife can help drive financial inclusion for this vastly underserved population.

Edited by Teja Lele