Calculating the Interest on FDs before investing can help maximise savings

Understanding the formulas to calculate interest on FDs allows you to compare various options and choose the one that maximises your returns.

Fixed Deposits (FDs) are known for their reliability and guaranteed returns in India. These investments are typically preferred by risk-averse individuals or those looking for fixed income through the flexible interest payout option. However, it's crucial to know how to calculate the estimated FD interest to maximise returns effectively.

The fundamentals of FD interest rates

Interest rates are the backbone of any FD. They represent the percentage of your principal amount (the initial deposit) that the bank or NBFC pays you as a return on your investment over the tenor.

Understanding the formulas to calculate interest on FDs allows you to compare various options and choose the one that maximises your returns. There are two main ways interest is calculated on FDs:

01.Simple Interest (SI)

In the simple interest method, interest is calculated only on the initial principal amount throughout the FD term. It's a straightforward calculation, ideal for short-term FDs with shorter tenors.

Here’s how it works,

SI = (P * R * T) / 100

Here,

P = Principal amount (initial deposit)

R = Interest rate (as a decimal)

T = Tenor (in years)

02.Compound Interest (CI)

Compound interest calculates interest on both the initial investment amount and the interest earned. This creates a snowball effect, leading to a higher overall return compared to simple interest.

Here’s a quick look at how the formula works:

Maturity Amount (A) = P * [1 + (R/100)]^T

Here,

P = Principal amount (initial deposit)

R = Interest rate (as a decimal)

T = Tenor (in years)

Power of Compound Interest: Why it Matters for FDs

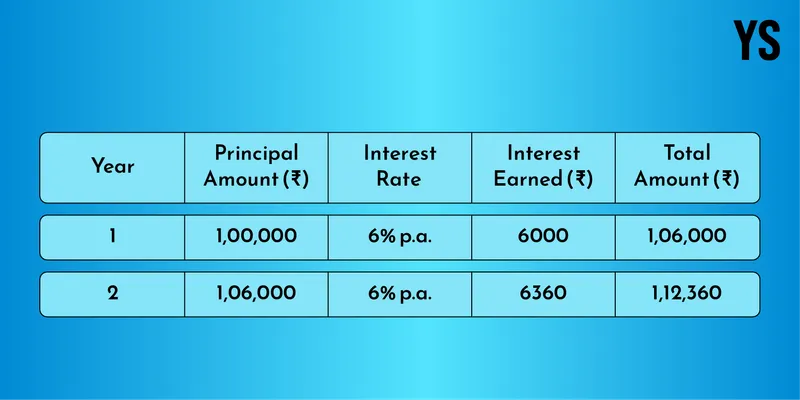

Let's illustrate the power of compound interest with an example. Imagine you invest Rs 100,000 in an FD at 6% per annum. for two years. You can earn the following compound interest:

Even with a short FD term and a moderate interest rate, compound interest adds an extra ₹360 to your overall return. This difference becomes even more significant with longer FD tenors and higher interest rates.

Leveraging online FD calculators for convenience

While understanding the formulas is valuable, online FD calculators can simplify the process. Most banks and NBFCs offer user-friendly FD calculators. These tools allow you to input your principal amount, FD term, and interest rate.

The calculator then displays the estimated maturity amount, including the accrued interest. This allows you to quickly compare different FD options and identify one that aligns with your investment goals and maximises your potential returns.

Factors affecting FD interest rates

Here’s a look into the key factors that influence the interest rate offered on your FD:

> FD tenors: Generally, longer FD tenors (e.g., five years or above) command higher interest rates compared to shorter tenors (e.g., less than one year). Issuers reward you for parking your money in for a longer period with a higher return.

> Deposit amount: In some cases, banks or NBFCs might offer slightly higher interest rates for larger FD deposits. This strategy incentivises customers to invest a higher amount.

> Credit rating of the bank/NBFC: The creditworthiness of the bank or issuer can also influence FD interest rates. Those with a higher credit rating might offer slightly lower rates due to their perceived lower risk profile.

> Special FD schemes: Banks and NBFCs may introduce special FD schemes with higher interest rates for specific customer segments, such as senior citizens or salaried individuals.

Maximising your FD returns

By understanding the factors affecting FD interest rates, you can strategically plan to maximise the returns:

01. Compare different rates: Don't settle for the first FD option you come across. Look for banks or NBFCs offering competitive rates that align with your desired tenor and deposit amount.

02. Negotiate: It may be possible for you to negotiate the interest rate on your FD, particularly for larger investments, with your preferred bank or NBFC.

03. Consider ladder deposits: Instead of investing a lump sum in a single FD, consider an FD laddering strategy. Here, you invest your money in FDs with varying maturities. This allows you to benefit from potentially higher interest rates of longer-term FDs while also maintaining some liquidity with shorter-term FDs that mature periodically.

04. Explore tax benefits: FD interest earned up to a certain limit qualifies for tax deductions under Section 80TTA of the Income Tax Act, 1961. This can further enhance your overall returns.

05. Invest for long-term goals: When choosing an FD tenor, align it with your long-term financial goals. Locking your money in for a longer term with a higher interest rate can be beneficial, but ensure the maturity date coincides with your need for the funds.

Understanding the intricacies of FD interest calculations, the power of compound interest, and the factors affecting FD interest rates helps make informed investment decisions.

Strategically planning your FD investments, comparing options, and considering factors like tenor and tax benefits, could help you maximise returns and achieve your financial goals.