FamPay has distanced itself from its teen-focused roots. Will its blanket bombing strategy finally land a blow?

Once a promising fintech, FamPay has veered away from its teen-focused branding after its breakup with IDFC last year triggered a costly botched platform transition. With investors turning cold on the sub-sector, can FamPay stage a comeback, or will it succumb to the fate that befell its peers?

Until a year ago, FamPay was hailed as a promising new kid in a sector that investors believed had largely consolidated into the top four to five players.

Spurred by the large cheques investors had cashed when the likes of , , , etc., grew, early backers were excited to get in on the next big use-case in the eternally sunshine fintech sector—an app that catered to a largely ignored population, teenagers.

's proposition was to create a pocket money, wallet-type app for children, with a numberless card linked to it. The app had two interfaces—one for teenagers and another for parents to transfer money and keep a check on their kid’s credits and debits.

The idea was to get children under the age of 18 hooked to a simple platform for small digital payments and leverage it to transition them to the adult version of the fintech app, which would offer a host of services, including digital loans, co-branded credit cards, insurance, and capital market investments.

However, FamPay has moved away from its youth-focused plans to position itself as a transaction or payments wallet. Its website—once featuring youngsters flaunting their personalised FamPay cards—now proclaims it’s a “spending account for everyone”.

The app has also done away with its teen-focused curated ecommerce feature it had introduced on an experimental basis. Nonetheless, gaming and Google Play giftcards and recharge coupons are available to buy on the app.

The startup’s ‘spray and pray’ policy—which seemed to have worked for it in the past—is not panning out this time around. An investor with first-hand knowledge of the matter tells YourStory that FamPay has been finding it hard to drum up funding, even from its existing investors.

The unwinding of FamPay

Things were going swimmingly for FamPay until January 2023. It grew from 1.35 million users in 2021 to over 10 million in 2022—all this while raising funding from Elevation Capital, Peak XV, and Y Combinator.

In fact, investors cut FamPay the biggest Series A cheque worth $38 million in 2021—a feat only paralleled by and .

Then, in February 2023, IDFC—the banking layer on top of which FamPay had built its product—decided to cut ties with the startup after banking tech company Zeta scrapped its Fusion programme, which IDFC was a part of.

“All of FamPay’s users one day woke up to a message from IDFC saying they were going to stop supporting FamPay’s operations, and that everyone had to utilise their credit balance by March 31, 2023,” a source close to FamPay founders, who sat in most of the company’s high-level discussions, tells YourStory.

Although it was a tough situation to find oneself in, FamPay decided to play its trump card—Tri O Tech—a non-banking financial service company it had acquired using funds from its $38 million Series A round.

“Tri O Tech was essentially a dormant company that didn’t do much, but it held a prepaid payment instrument (PPI) license from the Reserve Bank of India (RBI). For FamPay, at that point, it was a lifeboat,” the source says.

For co-founders Sambhav Jain and Kush Taneja, it was like a fresh start. The startup rebuilt its tech and slowly migrated users to the new Tri O Tech-powered platform by re-doing all the KYC and reissuing new cards starting March 2023—which, of course, strained the company’s financial resources.

And it rubbed investors the wrong way.

“It was like they were starting all over again after raising tens of millions of dollars,” says an investor who worked at Elevation Capital at the time.

“You want to see progress as an investor, not a race back to square one. The hypothesis they had sold FamPay on was becoming more and more distant,” adds the investor, who has since moved on from the venture capital company.

FamPay did not respond to YourStory’s queries for comments on the story.

Investors turn sour

To say nothing of the chaos that IDFC’s message caused among its users, FamPay’s switchover to the Tri O Tech-based platform was haphazard and glitchy.

Users reported that, despite redoing their KYC for Tri O Tech, they could not access the balance in their IDFC-backed accounts. Several others said their wallet balance had turned into a Tri O Tech gift card without their consent.

Also, users who wanted to quit FamPay weren’t allowed to access their funds or transfer their balances to another account.

To add to FamPay’s woes, scamsters decided to capitalise on the prevailing chaos by masquerading as FamPay customer service executives and swindled thousands of rupees from these digital wallets by asking users to reveal confidential information, user testimonials online reveal.

“Roughly, we estimate that we lost around four lakhs or at least 30% of the total users we had before the IDFC migration,” another high-level source, presently part of FamPay’s core firefighting team, tells YourStory.

“Sadly, it was also at this point that Kush went on an extended leave, and that sort of shook investors’ faith in the company,” the source says.

For FamPay, it triggered a domino effect.

Reputational damage aside, a decline in user engagement, the abrupt surge in expenses, and the ensuing notoriety stemming from the transition to the new platform, exacerbated by the unfortunate timing of a funding winter, significantly dampened investor enthusiasm for the company.

“Sambhav had been talking to investors around the time, and they were not happy with how things had gone down in March and how much money was spent on the migration. The market was also bad, and so, even the warm investors he had turned cold,” the source at FamPay said.

“We were offered funds at a lower valuation than our previous round, but Sambhav didn’t want to go for it,” the source said, adding, “In March 2023, the company only had 13-14 months of runway remaining.”

By the start of the first financial quarter (around April 2023), FamPay started axing jobs to cut costs. Multiple sources say that people in senior leadership positions were asked to leave. One source characterised these layoffs as “done least amicably”.

In August, the company did another round of layoffs and let go of mid and entry-level employees. Media reports suggest that FamPay laid off 50 employees in one round and 18 in another, totalling 68.

Around this time, Jain again approached existing investors for funding, “but he was asked to show an improvement in balance sheets and a way forward”.

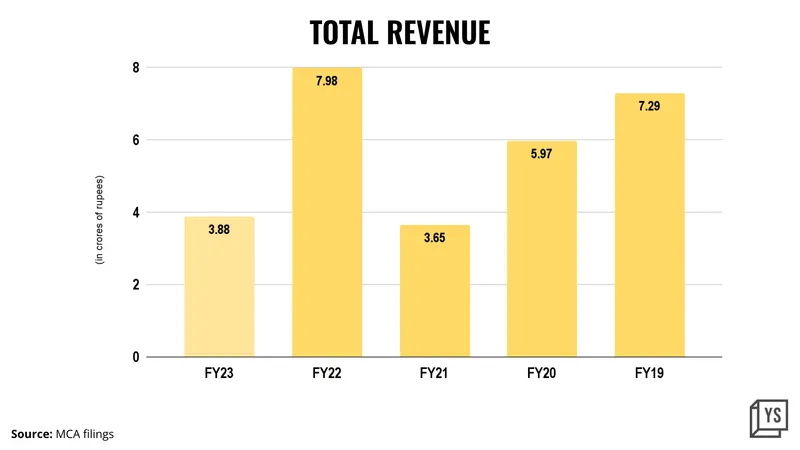

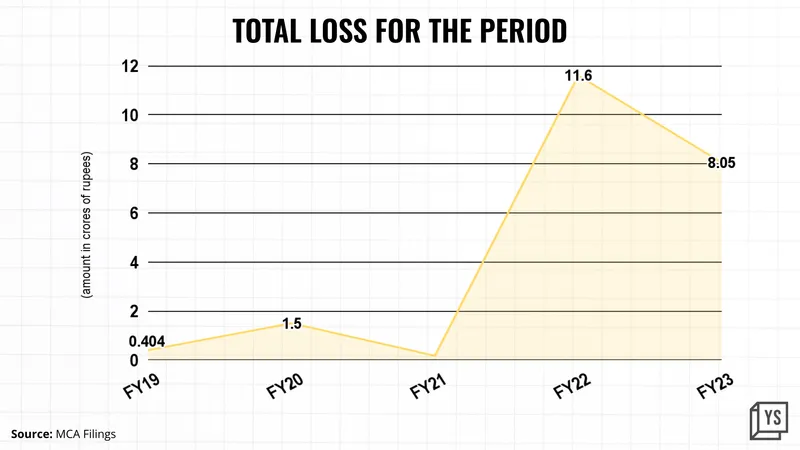

In FY23, before the layoffs and the migration to Tri O Tech, FamPay clocked a total revenue of Rs 3.87 crore—down 51.5% from the previous year. It reported a total loss of Rs 8.05 crore in FY23 versus a loss of Rs 11.60 crore in FY22.

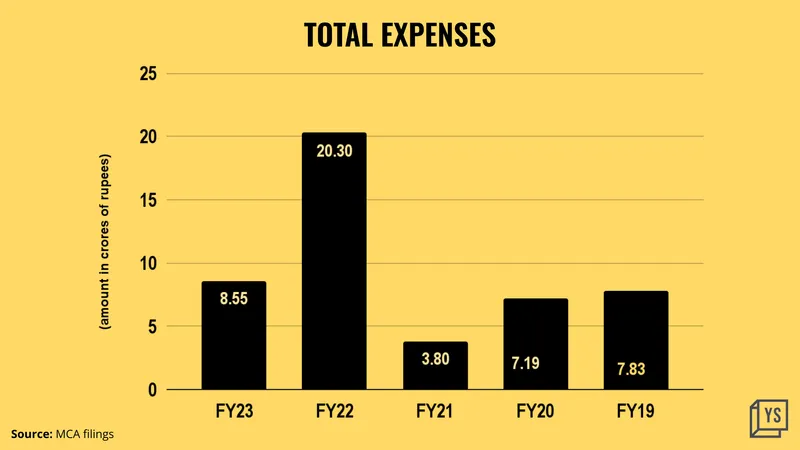

Legal expenses, one of its biggest costs in FY22 at Rs 1.3 crore, fell to Rs 62.5 lakh in FY23.

FamPay also drastically reduced its employee-related expenses, including salaries and wages, by 19% in FY23. This led to a 33.6% drop in total employee benefit expenses. Advertising expenses also nearly halved in the year, contributing to a 58% YoY reduction in total expenses, which amounted to Rs 8.55 crore in FY23.

Culture death

According to the company source, FamPay managed to extend its runway to 48 months owing to the restructuring exercises, but it came at the cost of a cultural loss. High attrition rates plague the company even today.

As per the seven current employees YourStory spoke to, the sentiment internally is quite bad, and the morale is low. “We don’t have job security here…everyone knows they can toss you out whenever things get tough again,” says an employee.

FamPay’s woes are also expounded by the fact that a handful of its peers in the teen-centred neobanking space— and Y Combinator-backed —have had to shut operations.

is the only player that still has a razor-sharp focus on this demographic, with M2P Finance as its infrastructure partner and Transcorp as the banking partner. It offers a student debit card in partnership with RuPay.

So far, FamPay has raised $42.7 million in funding from investors, including Elevation Capital, Venture Highway, Peak XV, and Y Combinator.

The lingering question looms: does FamPay possess another Hail Mary pass, or is it inevitably charting a course towards the graveyard of defunct teen-focused fintech apps?

(The story was updated to correct a factual error)

Edited by Suman Singh