The changing face of finance for businesses with no collateral

How age old finance methods may be the solution to the pressing problem of financing India's businesses

I’ve noticed how in the line of business financing, lenders in India are still unable to take the giant leaps forward compared to their European and American counterparts. And with right reason too, one may argue. After all, as a lender you are faced with the perpetual problem of having similar, if not equal downside as an equity owner, and a limited upside compared to an equity investor, who stands to gain from possibly unlimited upside. If you don’t believe me then look below.

The Loan Conundrum – limited upside

When an equity investor backs a business, the amount of equity invested in the business represents the amount of money which will be used for a variety of different, hopefully, revenue generating activities for the business. It could be hiring staff, buying equipment or even marketing activities. With the anticipation of increased revenue, comes the prospect of increased free cash flow for the investor in the future, and this is the prospect which ultimately leads to an increased valuation of the business, meaning that theoretically, an investor could sell the business for many more multiples than his initial investment was worth. Theoretically, the multiple could be infinite, if he can convince another investor that the free cash flow created from the business is indeed, infinite. However, should the free cash flows be zero now and into the future, the chances are that the valuation of the business is zero as well, and the investor will have ‘lost his shirt’.

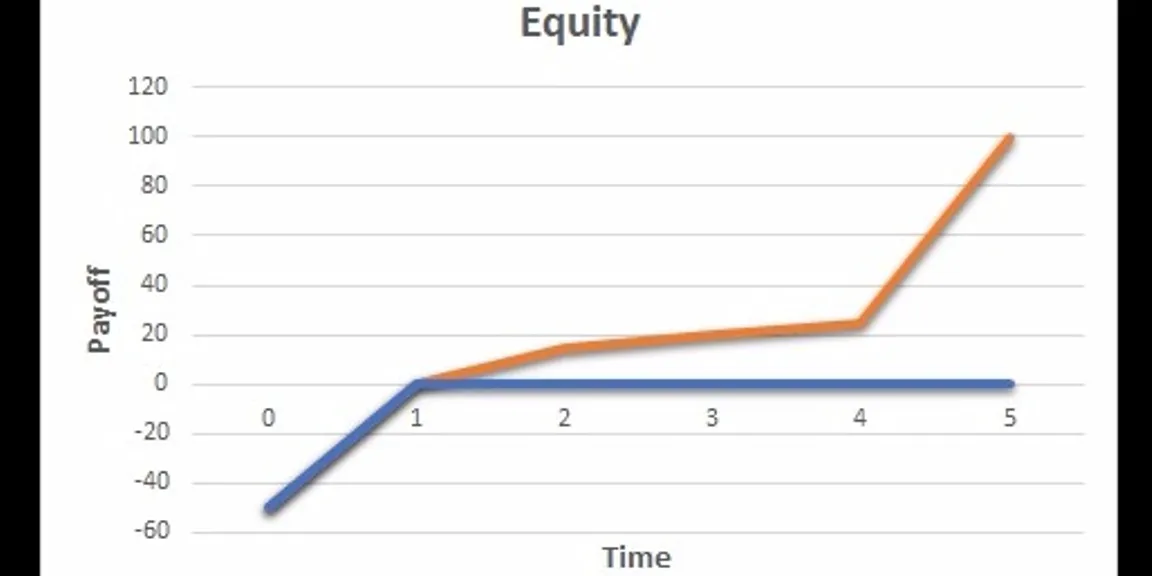

Equity investment - unlimited upside payoff potential

The diagram above represents the payoff associated with an equity investment in a business. The blue scenario shows the investment yielding no returns in a worst-case scenario, while the orange line shows a great situation whereby the investor gets back growing dividends in years 2, 3 and 4, before selling the business at a great premium in year 5. In theory, these dividends and sale could be an infinite payoff.

With debt investments (lending), the scenario changes slightly. When the lender disburses a loan, there is the anticipation that the loan will increase revenue generating activities for the business. However, the only compensation which is available for the lender is the interest that is due along with the principal sum of money lent. Therefore, there is a limited upside, limited by the amount of interest being charged to compensate for the risk of lending.

Lending - Limited upside potential and similar downside potential as Equity

The diagram above represents the payoff associated with an unsecured loanin a business. The blue scenario shows the loan getting no repayments in a worst-case scenario, while the orange line shows a situation whereby the lender gets back interest and premium through regular installments. Notice how, in a worst-case scanrio, the lender is in the same situation as an equity investor (ie – he has lost his shirt), but in a best-case scenario, whilst the equity investor stands to gain possible infinitely from his investment, all the lender gets back is a fixed return of principal and interest. So, it is a case of a limited upside, and similar downside vis-a-vis equity. Which is why, given this situation, a lender chooses to be more cautious in order to maximise the likelihood of getting back his principal and interest.

On the other hand, should the loan not materialize into increased sales, or worse, should the business experience declining sales, then there is a real risk of the amount of the loan not being repaid. In a hypothetical situation where sales go to zero, and the business is forced to liquidate, there is the very real risk that the lender could walk away in the same position as the equity investor. Having lost everything. True, because the lender is slightly above the equity investor in terms of hierarchy of liquidation preference, there is a chance that the lender could get back something from liquidation of net assets. But the lender can be behind a waiting list of creditors and staff, and the chances of recovering any amount is honestly just as remote as the equity investor getting his shirt back.

Lender Protection Methods

Lenders often look towards ways of protecting their investments

So, given this situation, it seems like lending is a very poor game to go into. However, as we know, it is a common practiced art. What lenders want is to minimize the chances of loan default. How have lenders protected themselves in the past?

1. Focus only on businesses with positive net worth - Positive net worth is defined as having an excess of assets over liabilities, or a capital buffer created through retained earnings or an injection of equity. This is done to ensure that there is liquidity in the business, and that should there be a liquidation event, that the assets cover the liabilities of the business.

2. Lend to businesses where there are tangible assets, and have a lien/first charge against them - This is often why lenders will not touch asset light businesses, as they want to secure their loan against some of the assets of the business, and thus protect themselves against the downside of not getting back the principal sum lent.

3. Look at businesses who are more than 3 years old -This helps lenders establish confidence that the business has been resilient and been able to cope and grow.

4. Lend only to those businesses which declare profits – Profitability implies that the business will have enough cash to repay the interest and principal repayments as and when they fall due

5. Have a Debt Service Coverage Ratio (DSCR) of more than 1 – Just because a business is profitable, does not mean that it has a positive cash flow. Lenders want to ensure that there is enough cash being generated to cover the principal and interest payments being made, and this is done through a calculation called the DSCR. With the DSCR, the lenders analyse whether net cash generated is enough to cover existing business loan repayments, plus any additional loan which the business may take on. If the ratio is greater than 1, it means that the business can take on more loans, as its net cash position implies that it can cover existing loan payments plus any additional repayments from new loans.

6. Have a CIBIL score of more than 700 – The above 5 methods show that there may be the ability to pay, but lenders also want to see willingness to pay by account of the business promotors’ CIBIL scores. This indicates to the lender that the business promoters have been honest and dedicated in repaying prior loans/credit card bills as they fall due. What this points towards is the level of honesty and integrity the promotors have.

Once lenders go through this arduous process of determining loan eligibility they will then assign a rate of interest as in indication of the level of risk that they are taking when providing the business with a loan.

A large demand for business loans – filtered out by stringent requirements

Isn’t it any wonder that business loans still take a long amount of time to be disbursed in 2017?

There are new lenders who claim that they have better, more refined methodology, as well as technology to help with disseminating loans. The likes of Lendingkart, Neogrowth and Capitalfloat represent a new breed of lenders who are taking on younger businesses which are not necessarily profitable, and providing them with newer products which provide accessible credit to those who could not have access to it previously.

However, the problem remains largely unsolved. Those who have low CIBIL scores and those who have a negative net worth are still being declined from borrowing, especially those who exist in asset light industries. Which is a lot of Indians and Indian businesses, particularly those who have recently started up. The age-old practice of lending against property or tangible assets such as vehicles continues to be the most accepted form of lending. And it is not only because the supply of such loans is high. Borrowers also seem to believe that getting a secured loan is the best route to take, because the amount of loan which will be disbursed is that much higher, and the rate of interest at a significantly lower rate than that of an unsecured loan. But this is a misnomer; the borrowers are still paying an exceedingly high rate of interest for a secured loan compared to what they actually should be paying (risk versus reward is skewed against them), and in addition, the loss of the asset should they not be able to repay the loan would mean that they ended up in an even worse off position than when they started.

Even unsecured loans are not in theory unsecured. All lenders ask the promotors to sign personal guarantees, as well as show evidence of a house or an office which they have bought, so that they cannot run off with the loan proceeds. It’s the lender’s way of having some security in case the business does not repay.

So then the question stands – are there any loan solutions which are unsecured, which help the borrower get access to an unsecured loan, which can take place irrespective of CIBIL score, and profitability? Are there any loan solutions which, at the same time, also provide a limited downside for lenders, meaning that their loan is more secure irrespective of having no security?

Bringing back old solutions in a modern world

Sounds like a difficult workaround doesn’t it. However, there are certain solutions at hand. There are age old lending solutions which have come back to fashion, which when coupled with technology, are providing the solutions to the questions above:

1. Group/community based lending – the notion of communities ensuring that loans are repaid is as old as when civilization started taking loans. From providing personal guarantees from well rated individuals to back up the application of the business. Other forms of lending facilitate around the pressure of a group of individuals, who are united with a common theme in mind. This sort of group creates pressure on one individual who has borrowed to repay the loan in a timely manner.

2. Loans against receivables/bill discounting/invoice discounting – Discounting is an age-old practice of financing whereby the borrower receives a disbursal of money with the interest already deducted from the advance. This is known as the discounted amount, set by the discount rate. Bill discounting is performed when the business has a bunch of credit worthy customers who it sells to, and these customers pay the business in 30, 60, 90 and even 120 days. Because of the number of days it takes for the customers to pay, the business can approach a lender to have the bill discounted, and some of the money advanced in lieu of the pending payment. When the payment comes through, the lender takes back the principal and an additional amount at the discount rate set. The credit risk is lowered

3. Sale and leaseback – Here, the business may own an asset which it is utilizing and generating revenue from a bunch of customers. To release cashflow, the business sells the asset to the lender, who leases it back to the business, with the lease amounts being paid by the business to the lender. At the end of the lease period, the asset’s ownership is transferred back to the business. The asset must be regularly generating revenue, and its ability to do so into the future must be viewed as probable, for this to work. It would also be helpful if there are contracts in place with the customers, and the customers of the business are viewed as credit worthy.

There are a host of old financing options which are coming back to the industry, leveraging upon new technology to close out any issues which may have existed with them in the past. These solutions can help asset heavy and light industries alike release cashflows to really help grow their businesses.

Sawan Shah is the Chief Financial Officer at MarketFinance India, an online platform which serves to provide financing solutions to businesses. The views expressed by him are his own.