This is a user generated content for MyStory, a YourStory initiative to enable its community to contribute and have their voices heard. The views and writings here reflect that of the author and not of YourStory.

The Next Trillion Dollar Opportunity in Fintech

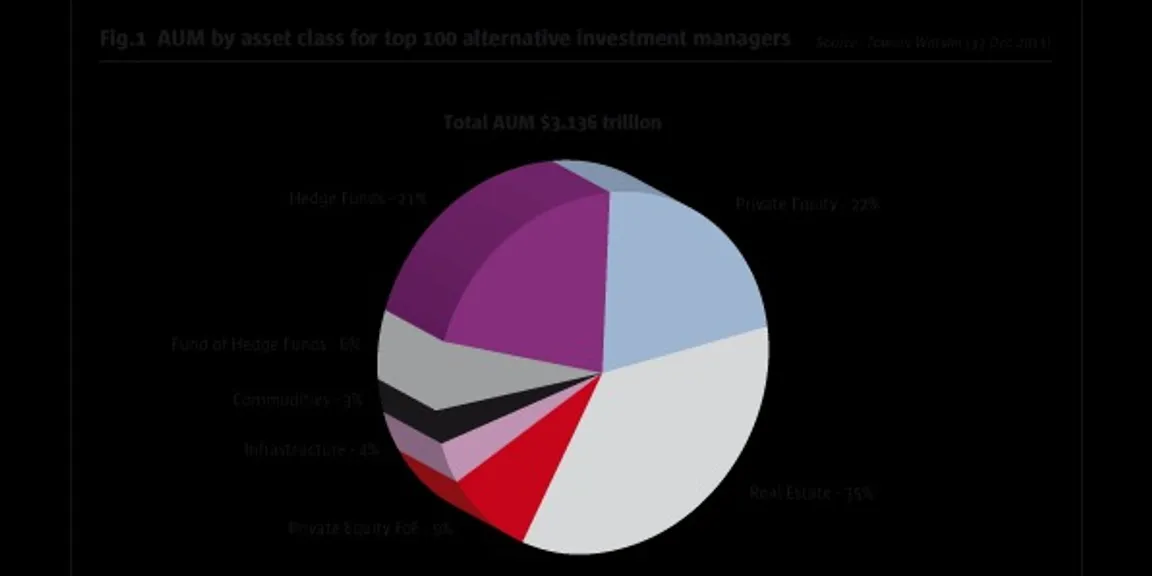

Asset Management and how Data Science Geeks can disrupt it