What is blockchain? Blocks, distributed ledgers and nodes explained in simple terms

Since Bitcoin was implemented in 2009 as one of the earliest use cases of blockchain, many blockchains have been created, with a wide range of use cases for each. Here’s all you need to know about the basics of the emerging technology.

In the last few years, interest in blockchain technology has skyrocketed, as it emerges to be a transformative force in private and public sector operations.

Besides enabling cryptocurrency transactions, blockchain tech can be applied for facilitating cross-border payments and building digital asset marketplaces to supply chain management, etc.

According to Grand View Research, the global blockchain technology market size was valued at $3.67 billion in 2020, and is expected to grow rapidly at a compound annual growth rate (CAGR) of 82.4 percent from 2021 to 2028.

If you’re interested in learning the basics of blockchain, and understanding what are blocks, nodes and distributed ledger technology, here’s all you need to know:

Blockchain basics

In its simplest form, a blockchain is a chain of blocks. When data is added over time in blocks, new blocks are built on top of previous ones.

Each block contains a cryptographic hash (a piece of information linking the new block to the previous one), a timestamp and transaction data.

And with the hashes holding the blocks together, a chain of blocks is formed, giving rise to a blockchain.

The transactions involved are recorded on multiple computers or devices across the world (also referred to as nodes). These characteristics make it impossible to retrospectively alter a block without altering all subsequent blocks.

Another feature of blockchains is that they are managed by a peer-to-peer (P2P) network of users.

In the P2P network, there is no central server or administrator. When a user wants to exchange information with a peer, they can send it directly to the recipient, without having to go through a centralised system or database.

Decentralisation

When many parties hold copies of the public ledger containing transaction data, the blockchain is said to be distributed. Blockchains are inherently distributed, but this doesn't always imply they are decentralised.

In a decentralised network, any user can participate and transact on the blockchain. And mechanisms must exist to ensure accuracy of transactions and address any vulnerabilities that may arise from this design.

In the case of Bitcoin - the first cryptocurrency built on blockchain technology - mechanisms such as mining (creating new Bitcoin by solving a computational puzzle) and proof-of-work (proving a specific computational effort has been expended) exist to preserve the integrity of the ledger and prevent corruption of the system.

Bitcoin is therefore considered revolutionary for proposing blockchain technology, and laying the foundation for the growth of the industry.

Infographic design by Manash Pratim

Importance of Bitcoin

In the Bitcoin whitepaper in 2008, pseudonymous founder Satoshi Nakamoto referred to it as a “purely peer-to-peer version of electronic cash” that would “allow online payments to be sent directly from one party to another without going through a financial institution.”

Describing the first blockchain, Nakamoto wrote:

“The network timestamps transactions by hashing them into an ongoing chain of hash-based proof-of-work, forming a record that cannot be changed without redoing the proof-of-work. The longest chain not only serves as proof of the sequence of events witnessed, but proof that it came from the largest pool of CPU power.”

If a majority of computational power (51 percent and more) is controlled by nodes that do not harbour a malicious intent to cooperate to attack or corrupt the network, the blockchain grows longer and outpaces attackers.

The white paper also noted that nodes can leave and rejoin the network, and have to accept the longest chain as proof of transactions that occurred while they were gone.

Transactions on a blockchain - an example

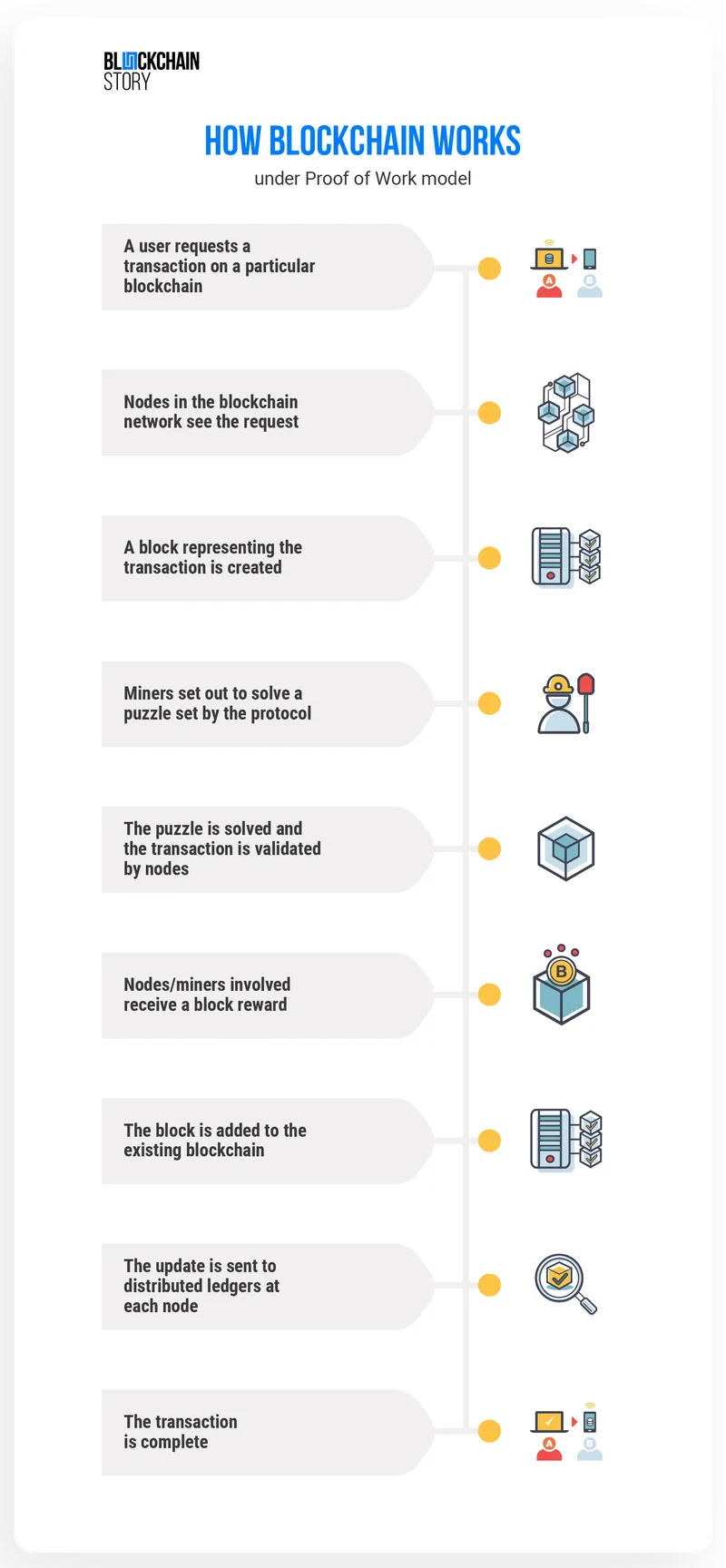

To understand more about how transactions work on the blockchain, let’s look at a simple example about how the Bitcoin blockchain is programmed to function:

Conventionally, if Priya wants to send Rs 1,000 to her friend Ankit, she notifies her bank (a centralised entity) by initiating the transaction.

After verifying that Priya has the funds to perform the transaction, the bank updates its database.

Priya’s bank balance in the database is reduced by Rs 1,000 and Ankit’s balance is increased by the same amount. In this example, it is assumed Ankit uses the same bank as Priya.

If Priya wants to perform a similar transaction, but send Bitcoin instead, the process is different. Here, a centralised entity like a bank does not perform checks, and does not update balances.

There is no singular entity responsible for this. Instead, all the nodes of that particular blockchain will have to be involved in the transaction, due to its decentralised design.

For her to send one Bitcoin to Ankit, Priya must first know Ankit’s public key (explained later) and then broadcast a message in the network so that other nodes can see it.

The nodes, or the users, then set out to solve a puzzle set out by the protocol, which requires them to hash transactions and other information in the block.

This is referred to as mining, and those performing this task are called miners. The miners must keep hashing data (slightly modified each time) until a valid solution is found to the puzzle and the Bitcoin can be sent to Ankit.

Finding a valid solution for the successful transfer of Bitcoin creates a new block, and generates a block reward for the miner responsible.

Once the transaction is added to the Bitcoin blockchain, all other nodes can see and validate it, and update their copies of the ledger to reflect it.

At the same time, Priya’s crypto wallet (where she stores her Bitcoin) is updated to show it has sent one Bitcoin, while Ankit’s crypto wallet is updated to show it has received one Bitcoin.

Further, as the network knows about the transaction, Priya is prevented from sending the same Bitcoin to somebody else (known as double-spending).

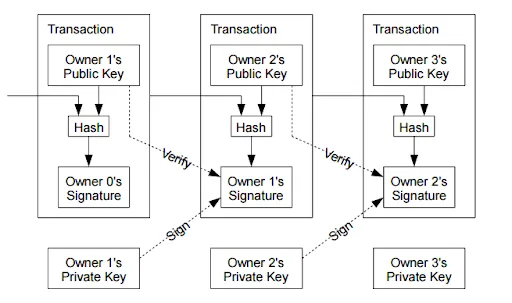

The blockchain network design proposed in the Bitcoin whitepaper

Public and private keys

To receive Bitcoin or any other type of funds/cryptocurrency on the blockchain, Ankit needs a public key as well as a private key.

Public-key cryptography proves ownership of funds, and in this case, Priya needs to know Ankit’s public address (generated from the public key) so she can send him the Bitcoin.

Ankit’s private key, however, must be kept a secret and unknown to anyone besides him. The private key is like a password which allows its owner to access and spend funds.

The public key is derived from the private key, and it is near-impossible for anyone to reverse-engineer the process to get the private key. If Ankit has not disclosed his private key, he alone can access and spend the Bitcoin sent to him by Priya.

Other blockchains

After Bitcoin’s design was implemented in 2009, several other blockchains have been created, with a wide range of use cases for each.

For instance, Ethereum - one of the most popular blockchains - is a distributed, decentralised blockchain that allows users to run programming code of decentralised apps.

Ripple, which enables real-time gross settlements, currency exchange and remittance through blockchain technology, is another popular example.

More about these blockchain projects and their tokens (cryptocurrencies) will be explained in future explainer pieces.

YourStory’s flagship startup-tech and leadership conference will return virtually for its 13th edition on October 25-30, 2021. Sign up for updates on TechSparks or to express your interest in partnerships and speaker opportunities here.

For more on TechSparks 2021, click here.

Applications are now open for Tech30 2021, a list of 30 most promising tech startups from India. Apply or nominate an early-stage startup to become a Tech30 2021 startup here.

Edited by Anju Narayanan