Value Chain Innovation in Ecommerce

Breaking the spell of the pessimism around Ecommerce these days, a more positive spin lies around the fact that growth of ecommerce in India will require stand alone companies to help them with revenue enhancement and operational efficiencies. A careful look into the problems provides a lens:

- There are hundreds of E-tailers across various verticals and all of them are in a contest to get in front of potential customers. Naturally, the cost of acquisition has gone up

- The cost of acquisition can ideally be amortized over time through customer retention above a threshold buying frequency, but we haven’t reached that equilibrium yet

- To add to this, Ecommerce being an inherently low-margin business in most verticals, means the industry needs to attain certain efficiencies that will keep this ship from sinking until equilibrium is reached – and here lies the opportunity

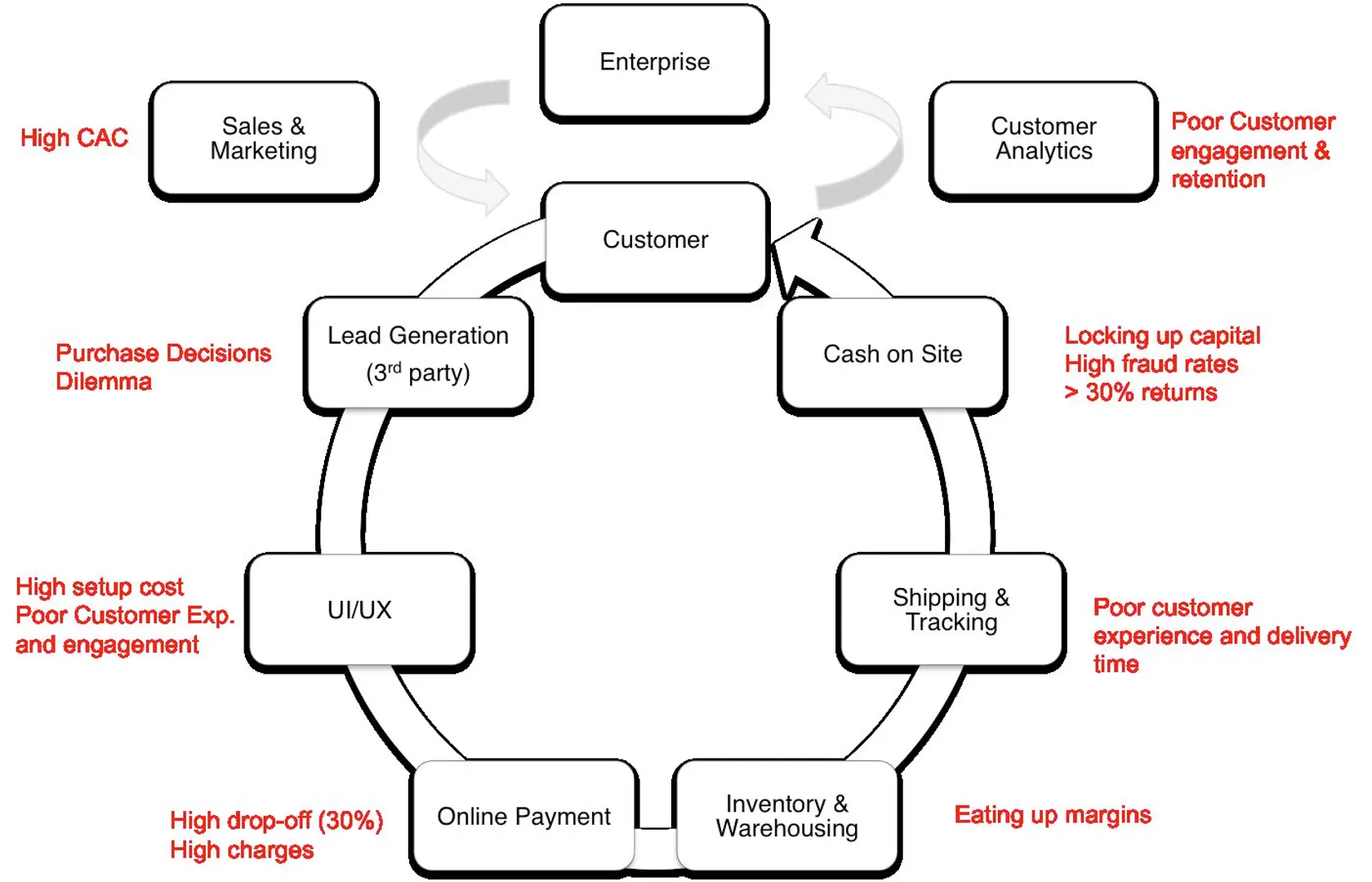

While US and China operate at higher operational efficiencies and service levels that justify higher margins, India has a long way to evolve before the ecosystem is friction-free. As a result, the industry is spiraling upwards into rising Customer Acquisition Cost (CAC) while operating under lower margins until some large player slow bleeds to death and the rest of the market share is up for grabs once again by the survivors. This was also the story of the emerging Ecommerce industry in US. Below is an image of the Ecommerce value chain and the key issues facing Indian E-tailer today.

Logistics: This part of the value chain is the biggest margin-eater for Indian E-tailing. US and China have supremely efficient logistics in place (despite their wider coverage) where some shipments even arrive before scheduled delivery date but are still not delivered to avoid future expectations of over-performance. While on the other hand, India lags well behind as we expand into the uncontested markets of the tier II and III cities. It is common knowledge now that some large companies even operate on a negative margin on deliveries in tier II cities. To add to this, courier companies cover only 30-40% of India’s zipcodes. Customer experience is egregious – courier agents don’t check with the customer’s availability, they lack training in dealing with returns, and their presentation fails to carry the brand’s image. All the above reasons point at a huge untapped potential. The logistics market alone is INR 300 Cr with a 33% growth-projections that makes it INR 600 Cr in less than 3 years. Players like Delhivery and Chhotu are getting their tier 1 cities mapped in entirety while Mudita and Holisol are honing their intercity performance.

Tip:

Logistics is an “all or none” market. The benefit of shifting to a newer Ecommerce-specific service is justified only when all the zipcodes in an area are covered, else a company would rather opt in for volume discounts with a superior courier co. Some players have considered tie-ups with brick and mortar outlets to a hybrid model to reduce returns and that get into loops.

Lead Generation: refers to any 3rd party service that helps in providing leads to ecommerce sites. Traditionally they exist as price comparison engines (mysmartprice), review sites (reviews42, reviewgist), and/or other innovative models (deal aggregators for example). Lead monetization is achieved with 3rd party services of OMGPM or Tyroo. This is a business that is entirely technology driven with low marketing spend and a good target for acquisition, making it slightly attractive for VC play.

Tip:

There’s much one can innovate in this space – image matching for clothing, fare prediction, closed group lead gen sites, 3rd party auctions, etc.

UX and Analytics: refers to any company than helps in improving the site user experience to drive sales. This is the grease on the wheels for Ecommerce in the US. There are hundreds of companies in the US help in performance improvement – sales, experience, engagement, deals etc. Conversion Marketing is an emerging field in India where Webengage has gained traction, with newer entrants like Runa and Nudgespot. Offergrid is a service that puts you in front of high-intent customers while Salorix is a big data firm specializing in converting ‘social signals’ into insights. In the same space is Unbxd, which provided intelligent tools that can be customized on your site.

Tip:

This domain probably has the highest prospects of technology innovation. This is technology driven and data intensive – something Indians are all good at. The US has plenty of startups in the same space, many of whom are Indian-origin founders. Eg: Hiten Shah of Kissmetrics.

Online Payments: Imagine having to spend Rs. 1200 on acquiring a paying customer who account for less than 1-2% of your daily site visits, and then having the payment gateway fail on your customer. You lost your sale and your acquisition cost (average total of Rs. 2300). Not just for 1-2 of them, but as much as upto 20-30% of all attempts. The technology is not perfected yet, but has improved drastically since the time payment gateways used to be a ‘commodity’. Nowadays gateways help you retrieve your dropped payment so you can continue where you dropped off and finish your payment. This has considerably reduced drop-off rates. PayU, Zaakpay, Citrus, EBS let you customize your gateway. Paytm payments lets you make mobile payments. Given the push for better payment systems from RBI, the challenges with COD and travel ecommerce market, the market is large, growing and favorable.

Tip:

Only 1 or 2 players have a name for good consistent performance. Risk management solutions and interface customization is the generally preferred direction. While payment channels are highly regulated, it is still possible to learn from the US and Chinese at newer methods. One such example from India is OnmobilePay and Mswipe – India’s reply to ‘Square’.

Offline Payments: Cash Payments is still a very small market being 1/10th the size of online payments largely used in E-tailing. The industry is lacks technology differentiation, and makes it unattractive for tech VC play. On one hand you have large E-tailers insourcing their logistics while the market is continuously expanding into tier-2 cities. Technology can be key to differentiation in this business – think NFCs.

Sales and Marketing: For a early stage E-tailer which hasn’t attained equilibrium yet (most E-tailers in India), their spend can be upto 50-60% of their revenue. This means the market for “sales and marketing” is massive, much of it coming from digital marketing services. Similar to Kenshoo, the automated SEM provider, is Sokrati which has many favorable reviews from E-tailers. While SEO players are more fragmented, it’s easier to identify the good ones (while googling for top seo firms in India if you don’t find them in top organic results, they probably aren’t good!).

All in all, India has a long way to go before we reach efficiencies to make Ecommerce value chain friction-free. And this means a ton of opportunities for startups. This article is meant to give you a precursory write-up of the major pain points in the E-tailing value chain and a hint at the innovative business models startup are using to solve these problems. By no means does the comprehensively capture the startups out there. If you’d like to add more startups, please comment below or shoot me an email.