The billion-dollar opportunity the Indian OTT industry is missing

India currently has around 40 OTT platforms. While having so many platforms is good as it enables more investment, it poses a different kind of problem for the consumer as to how many platforms will they subscribe to.

Historically, we have been consuming content on three platforms. We have been watching cinema since the 1880s, television since the 1930s, and the digital streaming platforms since 2000.

While I’m sure 2019 was a momentous year for India for many reasons, one phenomena that has possibly gone unnoticed is this – a five-year-old industry overtaking a 106-year-old industry in market size.

Between 2018 & 2019, India’s digital streaming (also called OTT) industry eclipsed India’s film industry in size. This is not a flash-in-the-pan. The trend has been so since 2016. India’s Over the top (OTT) industry has jumped a whopping 240 percent between 2016 and 2019.

In case you are wondering why the digital content streaming industry is called the ‘OTT’ industry, here’s a factoid – ‘OTT’ as an industry term emerged at a time when television used to reach people homes through physical cables & boxes and digital content was disseminated over the internet ‘over the top’ of the cables & the boxes. And the name just stuck. Also, an ‘OTT platform’ is what you would call a streaming service like Disney+Hotstar, Netflix, Alt Balaji, or Zee 5.

The OTT industry has two products – the content and the subscribers or viewers it has. While it may seem counterintuitive that consumers of the first business line become products of the second business line, let me assure you it is not.

While the OTT platform pays for content, owns it, and streams it to viewers, the platform also ‘owns’ all the data that its subscribers / viewers generate through their views. This data, combined with their demographics, is put through Big Data analysis engines to come up with consumer profiles.

Of course, all this is done without giving up individual users’ information. The platforms then monetise this data for advertising of products / services and additional content to these viewers either through straightforward ads or through suggested watching lists.

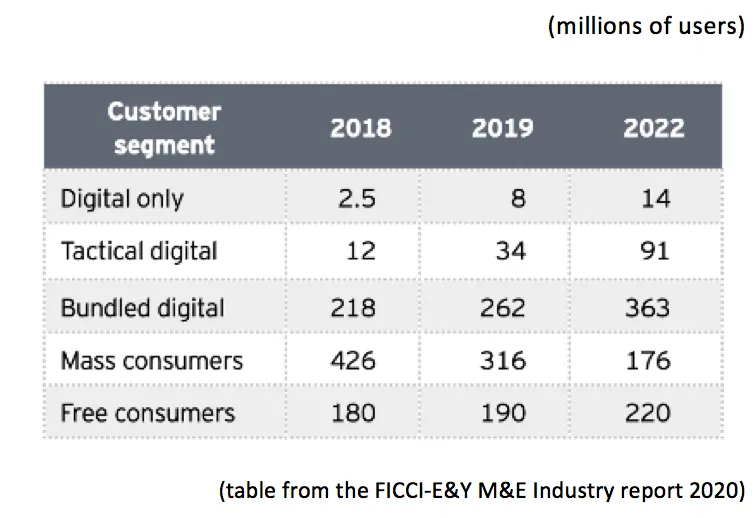

If you look at India’s customer segmentation through the lens of paying consumers across TV and digital, this is the chart:

Digital only – consume content only on digital platforms, do not access television.

Tactical digital – Consume Pay TV and at least one paid OTT service

Bundled digital – Consume Pay TV and generally only telco-bundled content

Mass consumers – Consume Pay TV & occasionally some free OTT content

Free consumers – Do not pay for content

India currently has around 40 OTT platforms. While having so many platforms is good as it enables more investment, it poses a different kind of problem for the consumer, which is – “How many platforms am I going to subscribe to?”

Here, there is a massive opportunity that all the platforms are missing.

As a consumer, if you want to watch a show or a movie on any of the platforms, you cannot do so without subscribing to it. You have to subscribe to the platform, albeit for at least a month. If you like one show each on five platforms, you will need to subscribe to all five of them for a month, at least.

The average ticket size is Rs 99 per platform, making it approximately Rs 500 for five shows. That, for most people, is a lot. There is no mechanism where you can pay for watching just that one show on a platform without subscribing for a period of time.

The platforms’ current strategy is to use the premium content (film premieres, edgy shows, etc.) they have as a hook to get people to subscribe to their platforms for a period of time. Now, since they have no other option, some people will do the same. These are likely to be regular theatre goers and people who fall within the first two categories mentioned in the table (tactical digital & digital only).

But these platforms that do not have a pay-per-show micro transaction model end up leaving the consumer with an all-or-nothing choice. This strategy ends up leaving out the 500 million+ people in the ‘Bundled Digital’ and ‘Mass Consumers’ groups (see table) from their business model.

Why they would do that is a mystery to me. I can only assume they are doing so since they want the consumer to become their subscriber, and hence they can own (and monetise) their consumption / demographic data as well.

Alternatively, it could be because their customer acquisition cost is high, and they need to ensure that every time they ‘get’ a customer (s)he pays an amount that at least covers the acquisition cost. However, there are cases where there is little or no customer acquisition cost, like in the telco bundled content users. They don’t offer the pay-per-view option there too. Wonder why?

Take a scenario where the platforms did allow a pay-per-view model of Rs 25/- per show and Rs 40/- per movie. Even if only 15 percent of the 500 million people end up watching two shows + one movie each month, it is over a billion dollars a year. This opportunity is being currently squandered by our OTT platforms.

The second benefit for the OTT platforms in this pay-per-view structure is the increased exposure that their content and brand receives. Once a new consumer has sampled some of the platform’s content on a pay-per-view mode, and has enjoyed it, chances are that (s)he is likely to become a regular subscriber to the platform, thereby increasing ARPU as well as reducing its customer acquisition cost.

There surely isn’t a lack of a mechanism for doing this. There already exists a similar mechanism in mobile usage. A mobile subscriber gets X benefits in a monthly package including x mins of calls and x min of data with a pay-per-use cost for everything above that. That same structure can be replicated across content as well.

If the platforms don’t want to use the mobile route, they could all get together and set up an aggregated search and discovery + micro-transaction platform (akin to the Amazon Firestick) and get all the platforms to be present on the same. Surely that can’t be so difficult. If they set up a jointly-owned aggregator platform and invest even $50 million a year to maintain it and promote it, the revenue benefits would outweigh the cost 20:1.

Further, they could all also share all the data being generated for all the viewers through said platform.

Imagine a scenario where, just like you receive your mobile bill, you receive a ‘content bill’ and it has two sections – Fixed costs, where you are able to watch any two shows and any one movie on any OTT platform for Rs 100/- per month, and over and above that, there is an itemised cost listing for all the content you have consumed over and above the package.

If implemented, it would be a win-win for everyone. Each consumer gets the ability to pay for just what they consume, and the OTT platforms earn a billion dollar a year more, with the potential of more.

Why it is currently not happening, is a mystery to me!

Edited by Megha Reddy

(Disclaimer: The views and opinions expressed in this article are those of the author and do not necessarily reflect the views of YourStory.)