[Startup Bharat] A bank account for pocket money: Paysack is making finances ‘Funq’ for students

Kochi-based fintech startup Paysack launched its student banking platform Funq to enable financial institutions to launch and build in-class solutions.

![[Startup Bharat] A bank account for pocket money: Paysack is making finances ‘Funq’ for students](https://images.yourstory.com/cs/2/3fb20ae02dc911e9af58c17e6cc3d915/800x400-v-1602588529785.png?mode=crop&crop=faces&ar=2:1?width=3840&q=75)

Going away from home for higher education is not as simple as it seems. Students have to figure out accommodation, learn to be independent, and more importantly — manage their own finances.

“The student community requires a robust but flexible solution for fee payments, automatic reconciliation, digital campus payment, and lending solutions,” says Ricky Jacob, Co-founder of Kochi-based fintech startup Paysack.

To address this problem, Ricky and his brother Nicky launched what it claims to be the world’s first student banking platform Funq in February 2020. Targeting academic institutions and the student community, the platform helps banks and fintech companies to build and launch in-class solutions.

Illustration courtesy: YS Design

Shifting gears

Founded in 2015, Paysack was initially bootstrapped and based out of Bengaluru. In 2016, to cut down expenses, the startup moved its base to Kochi. Moving forward, between 2015 and 2018, Paysack raised a total of $100,000 funding from friends and family, and a pool of angel investors

Understanding the importance of having a team that sticks together in the long run, the startup has designed a flexible environment to work in — with a lot of learning.

“We don’t have the challenges of trying to make sure we don’t lose our team members to a heavily funded startup who could offer over the top paychecks we could never match,” Ricky adds.

Ricky, Nicky, along with two other co-founders have earlier founded KRED, which is a neobank-as-a-service platform for enterprises.

“We had various use cases come to us — a digital campus, a white-labelled cards platform, fee payment, and auto reconciliation, among others. We saw an opportunity in bringing it all under a standardised open platform to allow future integrations with other offerings,” says the co-founder.

The core team at Funq

How does it work?

Money management is a life-skill that should be picked up early, and Funq wishes to ensure just that by re-imagining student banking in India.

“It is almost like the first bank account for pocket money,” Ricky explains.

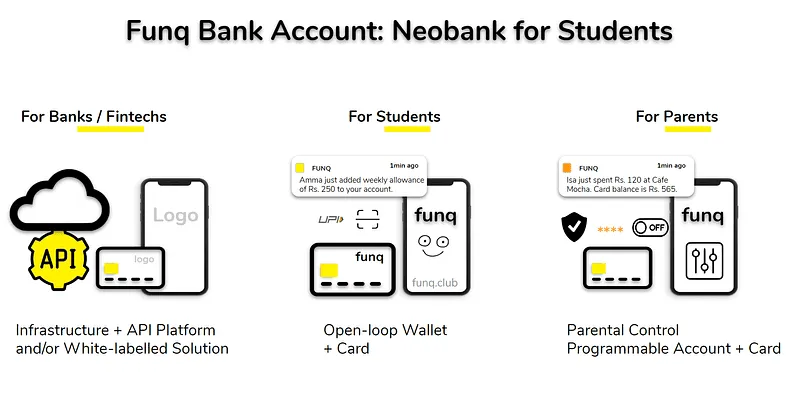

Funq enables students to have a zero-balance account, and provides a mobile application and card. This ensures that parents do not have to connect their accounts or share their cards with their children. For students below the age of 18, Funq allows parents to have full control.

Funq targets all the stakeholders in the student banking sector — banks, educational institutions (schools/colleges), ERPs, fintech companies targeting the student sector (with neo-banking, lending payments, fee collection, among other solutions).

Image Source: Team Funq

“We have a bank as our first customer who intends to deploy it at educational institutions that have their current account with it,” Rickey says.

Funq works on a SaaS model. Banks or financial institutions can use its white-labelled solutions such as contactless payments on campus or take it to educational institutions. “This includes contactless closed-loop payment systems – NFC cards, QR code, and mobile number,” Ricky says.

Alternatively, Funq has pre-integrations with various banking and non-banking entities, enabling one to connect with its APIs. Thus, financial institutions can use the closed loop payments system as APIs. It charges a setup cost and monthly or annual service fee per user.

Funq also provides card management services for RuPay, MasterCard, and Visa. For this, it offers a transaction-based revenue share model, besides the SaaS play.

Image Source: Team Funq

The fintech market

Statista suggests the largest segment in the Indian fintech market will be digital payments, with a total transaction value of $74,036 million in 2020. The number of users in the digital payment segment is expected to hit 929.44 million by 2024.

Various players have launched financial solutions around the student category — API platforms that provide a broader offering for collection such as , or banking as a broad category such as Zeta, and other players that provide prepaid card management such as and M2P. More recently, players like and have also been targeting teens.

However, Ricky believes that Funq has a differentiator to offer. “Funq brings student banking as a wholesome experience to help build and launch use cases targeting the segment — a combination of one or more features that can be integrated easily to existing solution providers,” he adds.

Going ahead, Ricky plans to establish Funq as a global student banking platform. It is working in partnerships for distribution in other geographies — Latin America, the Middle East and Southeast Asia.

Funq is also in talks with US-based investors to raise funds.

Edited by Saheli Sen Gupta

MOST VIEWED STORIES