Indian fintechs find sweet spot in SEA market

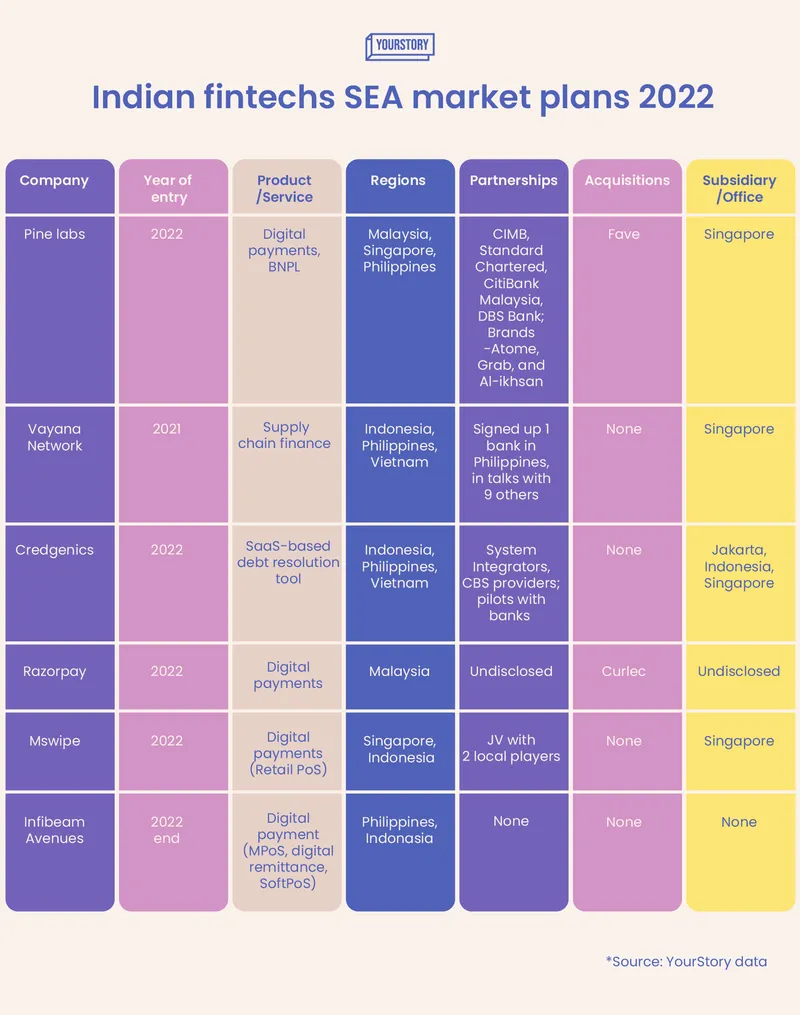

Top Indian fintechs like Pine Labs, Credgenics, Vayana Network, Mswipe, Infibeam Avenues, and Razorpay are looking to replicate their business models in the SEA market, with similar but yet different strategies.

The South East Asian (SEA) market has been on the radar of many Indian fintechs as they enter a stage of maturity and gear up for international rollouts.

While digital payments (mostly retail PoS) and BNPL (buy now, pay later) are the most popular segments, players in debt collections and supply chain finance are also making inroads. Among major players are , , , , (CC Avenue), and Credgenics attempting to capture a piece of the pie in their respective segments.

Why swim in the SEA?

Firstly, the market has all the right elements—a burgeoning young and mobile-first population, easier government policies, tax benefits, accelerated venture capital investments, favourable demographics, low financial penetration, and so on.

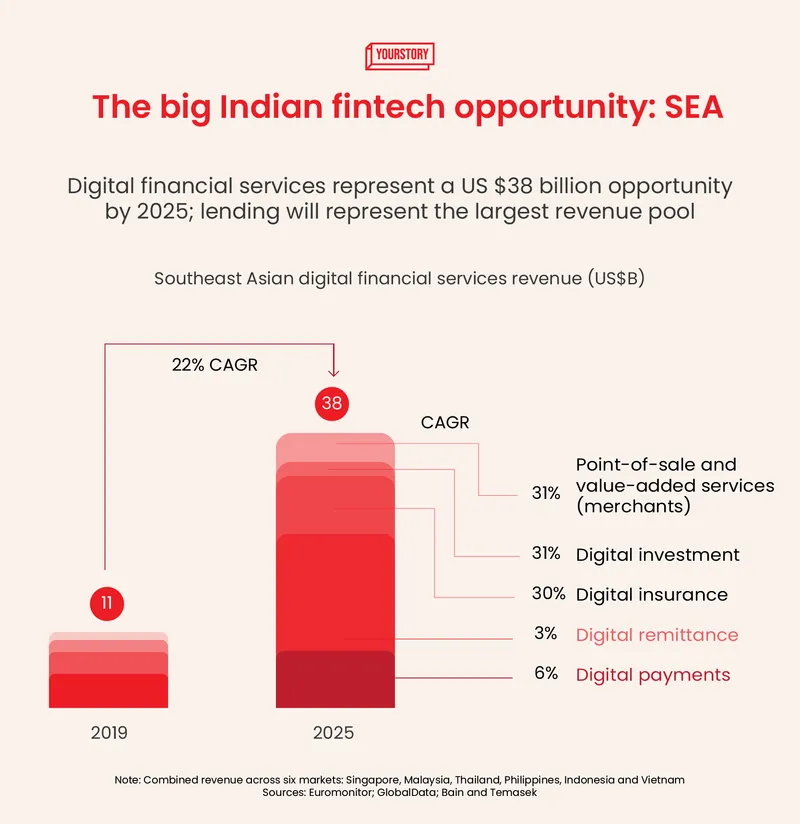

With a population of 570 million and a GDP (Gross Domestic Product) expected to reach $4.7 trillion by 2025, the six biggest countries in Southeast Asia (Indonesia, Malaysia, Singapore, Vietnam, Philippines, and Thailand) represent one of the world’s largest and fastest-growing regions, reveals a report by Bain and Company, Google, and Temasek.

Digital payments in the region are expected to exceed $1 trillion in transaction value by 2025 while other services—lending, investment and insurance—are still emerging, and are projected to grow by over 20% annually through 2025.

On the regulatory side, experts explain dedicated fintech regulators—like Financial Services Authority (OJK) in Indonesia—are making the entry of foreign fintechs smoother.

“Setting up a business in SEA is as easy or difficult as in India. Regulations are everywhere but you do need someone to help you understand and implement them better,” says Ketan Patel, CEO at Mswipe.

Also, the growing sentiment around cutting down dependency on one dominant player (China) has come as an opportunity for Indian counterparts to expand operations in the region.

“While Chinese tech platforms Alibaba and Tencent served as strategic investors in SEA in the past, the regulatory crackdown on Big Tech in China has slowed their global expansion, says Sampath Sharma Nariyanuri, fintech analyst at S&P Global Market Intelligence.

“With US payments companies such as PayPal and Block (formerly Square) typically limiting themselves to developed markets with high levels of credit card penetration rates, Indian fintechs have a unique opportunity to move into emerging markets and increase global footprint,” he adds.

Taking the JV route

Most fintechs are looking to take the Joint Venture (JV) route to enter the market i.e., either “help” a local fintech expand into value-added services like loyalty programmes and business management software, or offer their own tried, tested, and proven products in the new market with the help of a local partner. Either way, collaboration is the best possible way to go about the SEA market.

“We have come up with a simple strategy—we go in with our platform and domain knowledge and do a JV with a local partner who understands the market and people well. Otherwise, it would take about 2-3 years to understand the market, connect with locals, develop relationships, evaluate potential partners, and so on,” says Ketan from Mswipe.

The company, which has signed two JVs to date, said it’s too early to share numbers as it has just entered the market. The Falcon Edge-backed startup began by launching its flagship Point of Sale (PoS) terminal for the retail segment in Singapore and Indonesia.

On the other hand, Mswipe, which offers BNPL to SMEs and insurance which merchants can sell via PoS (soon to be launched), is looking to launch one product at a time in the new market.

“We will establish ourselves as a player out there and then see if we can push lending. A lot of fintechs have used this (international foray) as bait to raise money. Most of them have not been able to get their stories right. Now, the investors are also seeing through this. We want to take it slow,” says Ketan.

Get a guide

To enter the SEA market, the choice is between building on your own and forming a JV with an established partner. The former would make sense only if you have the management bandwidth and local knowledge. However, you would still need a “guiding partner”.

Like Mswipe, trade finance platform Vayana Network is clear about taking the partnership approach and is working with strategic partners. These are ‘market entry specialist/consultancies’ that help foreign startups enter the market.

“These people know the regulations in and out. They would help you get the doors opened and have that first informed conversation. Otherwise, it is a little tough. You will end up making wrong judgments,” says Vinod Parmar, Global Head, Sales and Marketing, Vayana Network.

This is specific for fintechs directly dealing with traditional banks and corporates (unlike new-age ecommerce and tech platforms) that may not be very open or welcoming.

Though the firm set up its subsidiary in Singapore in 2020, the real efforts and work commenced only last April. At present, Vayana is in advanced talks with five banks in Indonesia, three in Vietnam, and one in the Philippines (one signed), to enable credit to MSMEs in the said regions.

“By the end of 2022, we expect to be live with at least five banks across the market and support supply chain finance through our platform,” says Vinod.

Acquisitions for a leg up

Besides JVs, players are expected to enter into strategic acquisitions to increase leads or gain a competitive advantage.

According to Sampath, the M&A (mergers and acquisitions) path becomes a more attractive growth option for companies with access to capital as lower valuations make it easier to jump into newer categories.

“Acquisition priorities will be driven by the need for expansion (product, geographic), rebalancing the customer portfolio composition (large corporate customers versus small businesses), enhancement of risk modelling capabilities (fraud analytics), and value-added services (loyalty programmes, commerce enablement services, BNPL offerings),” he explains.

Take, for instance, Pine Labs, which acquired Malaysian startup Fave, which offers promotions/cash back/loyalty points for online purchases. The deal would help the former’s merchants drive sales from existing customers.

Pine Labs is also one of the few players that stepped into the competitive, crowded, and one of the fastest growing BNPL segments. As per reports, a lot of other Indian fintechs are looking to explore the opportunity and are already building operations.

However, BNPL would be a tough nut to crack as the competition rises. Many fintech companies, including regional giants GoTo, Sea, Razer, Grab, Gojek, and Oriente have launched their BNPL products along with pure-play regional outfits, such as Akulaku, Atome, Hoolah, and Kredivo. Australian BNPL player, Afterpay, also entered Southeast Asia by acquiring EmpatKali, a BNPL provider focused on Indonesia.

The demand is ripe for players like Pine Labs to take advantage of. The Sequoia-backed fintech is offering BNPL service to retailers in Malaysia followed by its recent network-based ‘Pay Later’ product in Singapore and the Philippines through a partnership with Mastercard and DBS Bank.

It has tied up with banks like CIMB, Standard Chartered, and CitiBank Malaysia, and is working with brands, including Atome, Grab, and Al-Ikhsan, to offer the same.

On SEA plans, Dheeraj Chowdhry, Chief Business Officer and Head–Pay Later– Southeast Asia, Pine Labs, says the company’s next destination includes Indonesia, Thailand, and Vietnam, where the Pay Later programme would be launched.

“The Pay Later proposition unlocks some large white spaces that were previously not offered in the BNPL space. Besides the proven segments like electronics and consumer durables, new segments like wellness, beauty treatments, tyres, and even insurance are being purchased in instalments. BNPL will continue to be a major focus area for us in our SEA strategy,” he adds.

The company refused to divulge its target numbers for the market as of now.

Even Razorpay—which acquired a majority stake in Malaysian fintech firm Curlec in February—is looking to build payment products for the market and then explore other regions in Southeast Asia. Curlec builds new-age tech solutions on top of existing payments infrastructure to make it easier for companies to collect recurring payments and take control of their cash flows.

The acquisition will help both companies build and scale their payment solutions. Razorpay will also slowly adapt and build products tailored to the region.

The company did not respond to YourStory’s questions on its SEA strategy and current operation status.

Pushing new launches

Launching in the same space, listed startup Infibeam Avenues will soon offer its flagship mobile PoS, near field communication (NFC), and contactless card technology, starting with the Philippines and Indonesia, via its brand CCAvenue. This would be simultaneous to its plans for Australia, where it recently opened a wholly-owned subsidiary ‘Infibeam Avenues Australia Pty Ltd’ to tap the burgeoning digital payment space.

The company already has international operations in the UAE, Saudi Arabia, Oman, and the United States.

“We expect to capture a 5% market size of the digital payment segment in the Philippines and Indonesia in the next three years,” says Vishal Mehta, Managing Director, Infibeam Avenues Ltd.

On scouting partnership opportunities, the MD adds, “As of now, we have no plans for acquisitions and will focus on organic entry and growth in these markets. But we are not averse to them for growth.”

The company has recently launched its SoftPoS payment technology—CCAvenue TapPay—and will push the same in both the new markets.

Challenges galore

Given the economic and demographic similarities in the markets, replicating the business model for Indian fintech is not much of a challenge.

As far as market receptivity is concerned, the retail and merchant ecosystem has matured quite fast while banking or the corporate ecosystem, at large, is still adapting to the change. Hence, fintechs in the B2C space have it a bit “unchallenging” to penetrate as compared to B2B.

“The banking practices in some of the SEA regions are just starting to digitise. It takes a little extra effort for the B2B ecosystem to engage in this market. You need to do some homework with corporates and banks,” says Vinod of Vayana Network.

This is where local partnerships come to play.

Next, comes the infrastructure challenge.

Like the government of India, SEA authorities insist on local hosting and warehousing of data. While cloud-based data systems are in place, the backend infrastructure is yet to become strong. The regions have local providers, but they are not that “straightforward” when compared with global names.

Companies are used to working with providers like Amazon Web Services and Microsoft Azure due to certain reasons, particularly security and reliability, explains Vinod.

“The usual setup process takes more time in some markets, given the regulatory differences and data localisation challenges. The archipelagic structure of Indonesia and the Philippines adds to the complexity, as distribution and maintenance expenses in these markets are higher,” says Rishabh Goel, Co-founder and CEO, Credgenics.

However, this is not an insurmountable challenge and tech teams can work on it, says a sector analyst on the condition of anonymity.

Credgenics has been in the SEA market since January, and is currently in various stages of discussion, including some in the advanced stage and some pilots, with a few large banks and multi-finance companies (MFCs) in Indonesia. It has set up primary offices in Jakarta, Indonesia, and Singapore, and is aiming for a million loan accounts in 12 months.

The region has similar issues in collections that lenders face in India as a developing market. The NPLs (nonperforming loans) are high, and collections have largely been tackled with manual and archaic processes. There are limited SaaS (Software-as-a-Service) collections platform players in SEA and globally too,” says Rishabh.

Localisation is another major challenge for companies that have to service their product to the audience. Certain markets, like Vietnam, completely operate in the local language. From a technology standpoint, a startup hence needs to be multilingual to be able to cater to the market.

“Our business (B2B) involves servicing the MSMEs, unlike a B2C tech provider. Local engagement becomes an essential part of our business,” says Vinod.

Face the competition

While Indian fintechs have all the leverage, scale, and demand to expand in the region, they will face competition from local fintech giants and new emerging players who are upping the game.

While regional tech players like Grab and Gojek have pushed into financial services, Chinese tech companies like WeChat and Alipay have entered through local partnerships. Pure-play fintechs such as Funding Societies, InstaReM, PayMaya, and StashAway offer digital financial services in specific verticals like lending, remittance, payment and investment.

According to a report by S&P Global, fintech startups in Southeast Asia netted $4.70 billion across 217 transactions in 2021, up from $1.13 billion across 118 deals in the prior year.

“The market is a sweet spot for Indian fintechs who are in a ripe position to leverage their scale and experience in operating in a low-cost payment infrastructure. However, they would need to be careful with how they roll out products and with whom,” says the analyst.

“Also, regulations in different countries using different sets of laws could deter a fintech company from expanding beyond a single SEA market. Keep a close eye on SEA regulations,” he signs off.

Note: YourStory reached out to 20 major fintech players in the market to understand their SEA plans. While some—mostly BNPL players—remained unavailable for comment, , , , , , and responded saying they are not looking at the region as of now.

Edited by Saheli Sen Gupta