The new BNPL: How will the business change post RBI crackdown?

Following RBI’s June notification on prepaid payment instruments, many BNPL operators have been forced to rethink their business models. We take a look at what the industry’s thoughts are around the circular, and the options they’re considering to become RBI-compliant.

A founder at a well-known Buy Now, Pay Later (BNPL) startup said the company hasn’t switched off the lights at his offices since late June when the Reserve Bank of India (RBI) released a circular banning nonbanks from loading prepaid instruments—digital wallets, or cards—using credit lines.

The startup, which requested anonymity given regulatory sensitivities, has had to not only rethink its product innovation but also its business model.

"We’re evaluating multiple new models to pivot to but there’s no doubt that, inevitably, the latest directive forces us to move away from our core mission, which has been to provide credit to people who don’t have great credit scores, or have low credit scores… people who have, till now, been excluded from the credit industry because of risk-related reasons," he told YourStory.

BNPL was often touted as the first step to getting Indian users started on credit products. After all, not many Indians have the required credit score or income records to be eligible for a credit card. In fact, only 6% of Indians have a credit card today.

The informal lending sector, on the other hand, is a different kettle of fish.

Most Indians who can’t get loans from banks and non-banking financial companies (NBFCs) find themselves at the behest of unscrupulous lenders who charge high-interest rates and use brute force for recoveries.

Sociologically also, most Indian kids grow up with a “debt is bad” mentality. We even have an epithet to that effect, which roughly translates to “stretch your legs according to the coverlet”.

But BNPL positioned itself as the antithesis of it all.

Card-based pay-later startups said they were offering small, manageable, sachet-sized credit that could help users build their credit profiles, provide a safety net in times of emergencies, and, more importantly, help people understand the way credit works—all via a card.

, in its various press releases, has called itself a “credit card challenger”, while fintech startup launched Ring, a “credit-backed card” in June that “intends to be the credit card challenger for a large base of customers who are otherwise seeking convenience in their transaction.”

For BNPL players, including card-based ones, the next step was turning people to personal loans that generally carry higher interest rates and have bigger principal amounts.

To be fair, the RBI does not mind people accessing credit lines; it just wants companies to call a spade a spade.

(Design credit: Aditya Ranade, Team YourStory Design)

A chief risk officer at a fintech startup told YourStory that RBI’s bone of contention is with startups essentially repackaging and marketing a credit card-like product as “something new, something different.”

“The RBI has no problem if a company offers a credit line and does not charge interest on it for three months; it would probably welcome it, because, as a regulator, it always has the best interests of the ‘little guy’ in mind. The problem arises when you take a product that exists, add some bells and whistles and slap a new name on it,” she added.

There are several other “theories” as to why RBI cracked the whip on BNPL companies making the rounds, including one that says it was mostly to placate banks that are losing business to fintech startups.

A report by The Hindu BusinessLine, citing sources, said RBI has asked banks to trim their tie-ups with third-party fintech apps, especially where it is a lender, an equity investor, or holds a substantial interest.

But the theory that RBI may want the banks to power card-based pay-later companies is gaining more credence as partnerships with banks is being touted as the easiest pivot for these card-led pay later companies in a regulatory quandary currently.

What does the RBI want?

Most sources YourStory spoke to requested anonymity given the sensitive nature of the topic, but unanimously agreed that while the RBI’s statements are never equivocal—including the current notification on prepaid payment instruments (PPIs)—there is confusion around whether solutions and pivots being explored sit right with the regulator, and what some terms used in the release connote.

To begin with, while “credit line” is clear as day, there are questions about whether “credit line” in the notification refers to just revolving credit, or non-revolving credit, such as loans.

Secondly, there’s little clarity on the entity RBI is trying to regulate: the shadow banks/NBFCs, card-based pay-later companies, or PPIs.

"If RBI can tell us exactly what it has an objection to, it would help us narrow down the options we’re currently exploring and comply better with the financial regulator," said one of the CXOs quoted earlier in the story.

A business head at another popular pay-later company opined that the RBI’s problem is not with any parts of the entire payment chain, but the "optics".

“Somewhere in the middle of it, the optics changed and we started being called mirror credit cards or credit card challengers…various parts of the entire chain, including the media, the end-users, our competitors said pay-later was something like a credit card product, and these things started coming to the RBI’s attention, which is why it needed to step in,” said the CXO.

Pay-later innovation was one of the reasons the PPI industry was able to survive despite the dent UPI made, and the circular essentially kills two industries, i.e., PPI and BNPL, in one go, at a time when credit penetration is finally increasing, she add.

But Vishwas Patel, Chairman of the Payments Council of India said the RBI was forced to step in because it was not happy with the way credit was being used.

The media is rife with stories of lending apps and companies using reprobate recovery methods such as brute force, contacting the borrowers’ phone list, showing up at people’s homes at odd times, calling incessantly, and threatening with legal notices within days of late payments, etc.

“Formal lending is only at 28% in the country…there’s no denying that there’s a big credit gap which pay-later companies are obviously able to plug. At the same time, credit is a highly regulated space, and (the RBI felt) those regulations were being bypassed,” Vishwas added.

Moreover, because fintech companies cannot blacklist or reduce a borrower’s CIBIL score in the event of non-repayment, bad borrowers can return to the system.

“Regulation is a necessary thing to weed out bad apples,” said Anuj Kacker, executive committee member of the Digital Lending Authority of India (DLAI), and the co-founder of Freo.

He pointed out that one point of contention for the central bank was the use — or misuse — of a PPI as a credit instrument.

“Prepaid means money has to be yours first...credit is not your money; it, by definition, has to be paid back,” he said.

However, the DLAI has made representations to the Reserve Bank of India asking, on behalf of pay-later card companies, for a way of out this situation — within the guardrails of the regulator’s law.

“We’re asking ‘What is the fundamental point that you're trying to solve? Is it customer protection? What is the exact issue?’,” he said.

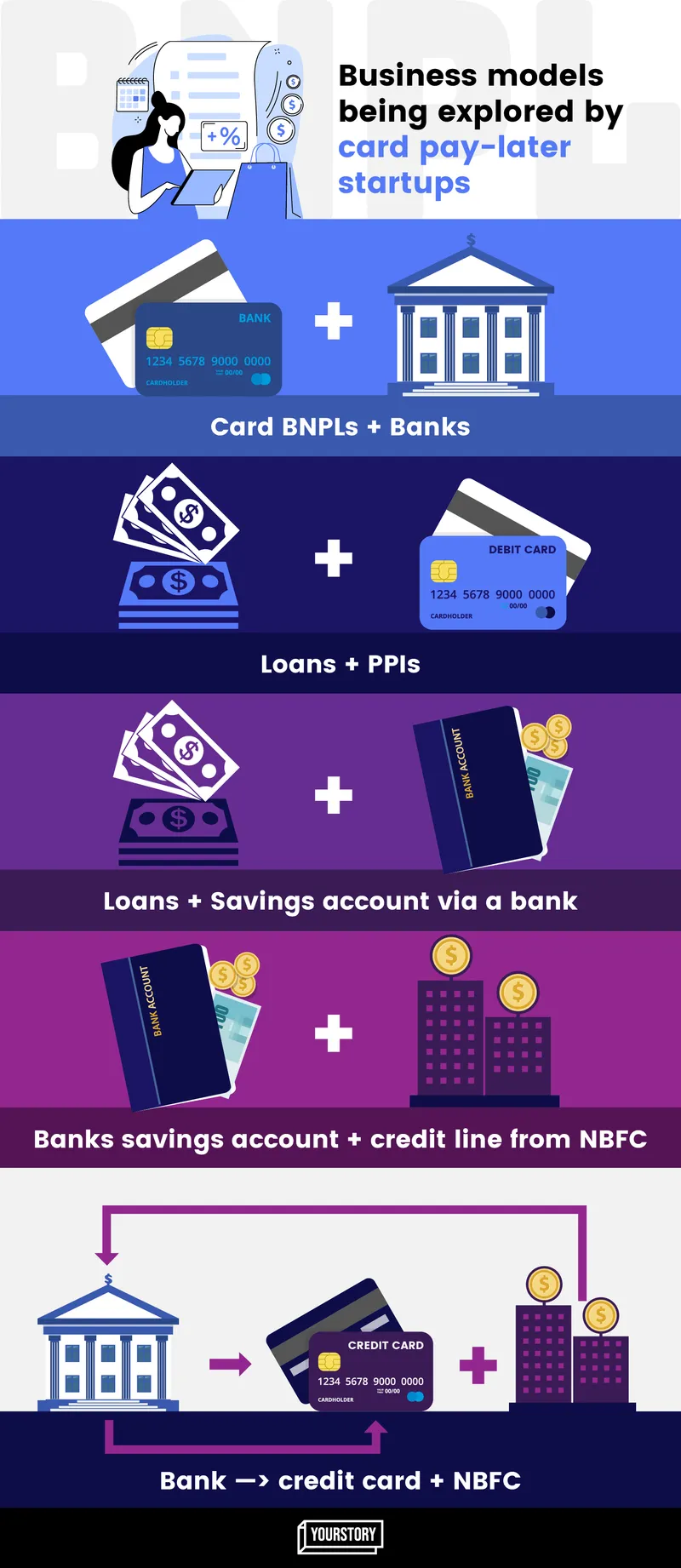

Business models gaining traction

In YourStory’s discussions with BNPL players—all of whom requested anonymity—most called out four-five business models being mulled by the industry, at large, right now:

Tying up with a bank

The RBI stated that nonbanks can no longer load prepaid instruments using credit lines, which makes it seem like the regulator would not have an objection to BNPL startups giving this a go in partnership with banks.

The concern the industry has with this model is that banks come with increased regulatory oversight, and more scrutiny. This means no more issuing credit to people who don’t have stellar credit scores, or are new to credit.

“This is essentially back to square one. Banks don’t want risk; we don’t either. But the reason we’re able to serve the segment that banks typically wouldn’t lend to is because we have superior, AI-based underwriting. We look at a customer holistically—their expenditure, their repayment, etc.—not just as their credit scores,” said one of the founders quoted above.

Also, a bank backing a card that comes with credit is essentially what credit cards are, and that’s a model that pay-later card companies have been trying to distance themselves from.

“Credit cards are the most elite form of credit that’s given out to creme-de-la-creme of borrowers—the polar opposite of what we’ve been trying to do with pay-later cards,” said the business head of the lending division at a large fintech company, speaking to YourStory on the condition of anonymity.

Considering that credit cards have the lowest penetration rates compared with other forms of transactions—UPI, net banking, etc.—issuing a card in collaboration with banks would basically be replicating the credit card model.

Anuj from the Digital Lending Authority of India (DLAI), however, disagreed. He said that if fintechs are able to prove their underwriting prowess and convince banks that they’re taking well-calculated risks by lending to people who are new to credit, banks shouldn’t have a problem with issuing a credit or a loan-funded card.

Disbursing loans via prepaid payment instruments (PPI)

The RBI has been quite careful with its wording in the June notification. It does not want “credit lines” to be disbursed via PPI. “We’re asking if we could disburse loans via PPI instead,” said a founder quoted above.

Industry experts are confused about whether the RBI has an issue with the NBFC issuing the credit loan, i.e. if it wants shadow banks to become more prudent about their credit, or if it just has a problem with the type of loan or credit being disbursed, ie credit line versus a loan, both of which operate quite differently.

A loan, for example, is non-revolving, which means the borrower borrows how much they require, uses the funds, and then makes payments (including interest) until the debt is paid off. Interest is levied on the entire amount of the fund.

A credit line is continuous, which means the borrower can use however much they want—up to their available credit limit—and then make regular repayments. Borrowers don’t have to use the entire credit line immediately, or in one go.

(Design credit: Aditya Ranade, Team YourStory)

Extend loans via a savings account

With a savings account, BNPL companies will be able to disburse funds via loans, into people’s accounts directly, and users can use their debit cards to make payments on the go.

A bank savings account + an NBFC credit line

A full know-your-customer (KYC) banking account, which is funded by an NBFC credit line, seems like a legitimate, doable workaround for BNPL companies.

Banks become the PPI issuer

A source told YourStory recently that SBM Bank, which has tied up with several neobanking players and other fintech startups, is currently mulling issuing a payment instrument—a card, basically—funded by an NBFC that could park its funds in an escrow account with the bank. The bank could then channel the money into the payment instrument it has issued, and the fintech could act as the face of the operation.

SBM declined to comment.

Calls for more oversight

Most BNPL and fintech founders YourStory spoke to seem to concede that, whether it’s on NBFCs that extend the credit lines, the prepaid payment instrument issuers, or pay-later companies themselves, the RBI should, rightfully, regulate the industry more so that interests of the “little guy” are protected.

The three industries have already made supplications to the central bank in recent times for additional governance, as well as for guidance on how to move forward.

“I think the biggest thing has been an acute lack of communication between the industry and regulators. The RBI is always quite happy to engage, and the next step, we think, is making a representation to the regulator to truly understand where it sees us hurting the end-user,” said one of the sources.

Two others added that the RBI directive was to rein in the penetration of NBFCs, especially following the liquidity squeeze in 2018-2019 that started with Infrastructure Leasing and Financial Services Limited (IL&FS) and led to the unravelling of Dewan Housing Finance Corporation (DHFL) and Reliance Anil Ambani groups.

The Payments Council of India (PCI) said it has already written to the central bank and government officials seeking a reversal of the order, especially given that pay-later companies fully comply with KYC norms.

In fact, RBI’s draft guidelines on digital lending is expected to come soon. According to a source in the know, the RBI is contemplating issuing special licences to pay-later companies.

Top digital finance companies and BNPL have also petitioned the regulator to clarify some doubts about future models and wordings used in the notification, as well as lay out a roadmap for them to follow in terms of what the RBI thinks the new model should look like.

Shortly after the RBI notification, the DLAI wrote to the RBI asking for a minimum of six months of extension to comply with the notification. The RBI is expected to release detailed guidelines any time this week, according to a source in the central bank.

The industry right now

Slice, a prominent player in the BNPL space, updated its terms and conditions in a notification to its users, saying users would have to pay monthly interest for dues not paid off in the first month—basically doing away with the 1/3rd model where users could split payments into three, and pay them off at 0% interest rates over three months.

Last week, the Tiger Global-backed startup announced a new product called 'Purchase Power', and switched to term loans from credit lines.

In a tweet, ex-BharatPe founder Ashneer Grover said the RBI circular is “aimed at protecting bank’s lazy credit card business from fintech’s potent BNPL business. It’s a flex move by banks — rent seeking.”

PayU-owned , , , and and temporarily suspended their BNPL offerings too. LazyPay could switch from a prepaid card to a credit card, a source who requested anonymity told YourStory.

There’s also growing scepticism around not just the way BNPL-led credit is used—sometimes as leverage to purchase cryptocurrency, or to gamble online—but also some of the terms and conditions most people don’t bother reading through.

A recent study by Chennai-based policy research institution Dvara Research ‘The costs of using Buy Now, Pay Later (BNPL) products’ says first-time consumers of BNPL services may not be able to comprehend what they are signing up for. In some cases, customers may find it difficult to even locate and access T&Cs; this gets exacerbated when BNPL products are embedded as a payment option that customers can use to make payments at the point of sale.

According to the findings of Dvara’s report, the Key Facts Statement (KFS) and important terms provided by BNPL players are not always available or even reliable.

In some cases where KFS was provided, it omitted key details such as pricing, customer obligations, and penalties. This contravenes the Reserve Bank of India's (RBI) Circular on Display of Information by banks, the report said.

The findings further disclosed that most of the players place the “burden” of ensuring the “suitability of the credit” on the buyer. Some providers like Pay Later and explicitly place the responsibility of assessing the suitability of the credit line on the customer.

“This ‘buyer beware’ approach is problematic and contravenes the Right to Suitability that customers have under the RBI Charter of Customer Rights Provisions; these can compound customer protection concerns,” the report states.

Given that Indians don’t understand most credit products, or bother to look for the T&C, there’s a common misconception that these BNPL cards are payment products—like a debit card that comes loaded with funds. The misnomer “credit card challenger” is also harmful because it dilutes the fact that what consumers are ultimately using is credit, and this misunderstanding has led to many borrowing beyond their means or ability to repay.

There are also unspecified processing fees, and random miscellaneous fees that make it hard for borrowers to truly understand the cost of borrowing.

Ultimately, whether the industry likes it or not, RBI is doing the job it was meant to do with the PPI circular — and industry operators allude to it too.

“The RBI doesn’t care if it kills off an innovation completely; as long as it is still doing the job of protecting people, it will be happy,” said the co-founder of an SME lending startup.

(The story was updated to correct a typo and clarify a few quotes by Anuj Kacker from the DLAI)

Edited by Saheli Sen Gupta