Wait and watch in private secondaries market amid push for discounts

This year has seen a steep rise in inquiries to sell shares in Indian technology startups in the private secondary market as buyers drive a hard bargain.

Everybody loves a good bargain, more so when it is a buyer’s market.

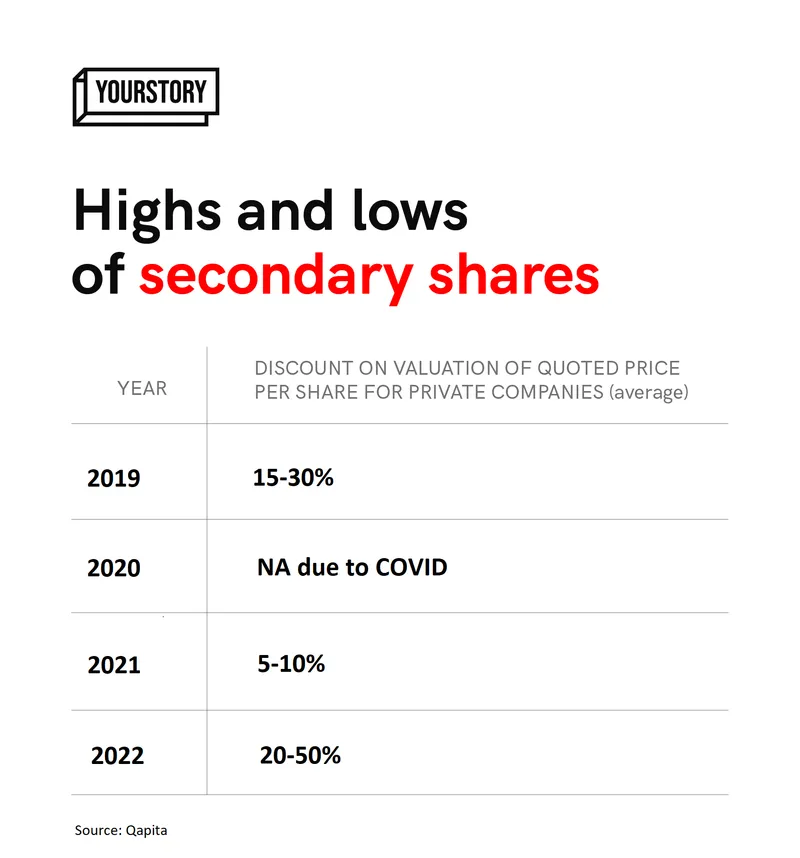

The private secondary market for Indian technology startups right now is in price discovery mode, with growth-stage startups and startup unicorns trading at a discount ranging from 20% up to 50% in some cases from their primary market valuation for comparable shares.

Investment bankers and secondary market experts for growth-stage companies peg this on market correction as well as funds from 2015-16 vintage looking to exit their illiquid assets.

While 2021 saw hardly any discount between primary market and secondary market value of comparable shares, unicorn startups such as , , and IPO-bound companies such as and API Holdings, owner of , have seen a steep haircut in Over-The-Counter (OTC) secondary market for private companies.

Some startup unicorns are trading at higher-than-average discounts in the OTC secondary market.

YourStory reached out to these companies for their comments on the movement in share value. While boAt said that as a policy, the company doesn’t comment on its past, present, and future share price, others were yet to respond to queries till the time of publishing the article.

“The valuation of technology companies has come down since the IPO. This, followed by a drop in liquidity and attrition, has impacted secondaries of deemed-public companies. We are seeing an average of 25-30% discount on secondaries for these companies,” Ranjit Jha, Managing Director-CEO at investment advisory firm Rurash Financials, tells YourStory.

The drop in valuation of startups in sectors such as edtech, fintech, and consumer brands, which went through a hyper-funding cycle last year, has resulted in an increase in enquiries to sell.

However, negotiations have been difficult to close, as buyers continue to be in price-discovery mode, says Skanda Jayaraman, CEO of Qapita Marketplace, which facilitates liquidity solutions for startup stakeholders via a digital marketplace.

The big picture

“The big contrast from 2021 is that demand outstripped supply, allocation to buyers was the problem to solve. Today, there is a glut of supply out there in the market and demand has fallen sharply (to peak-COVID time/demonetisation levels) because the 'fair price' of an asset is not easy to establish,” Skanda says .

Skanda adds that even companies that are public (yet unlisted), whose shares are traded freely, have seen erosion in value for investors, and in margins for intermediaries. "The problem with offering steep discounts in private companies is that founders would not like (and therefore unlikely to allow) steep discounts to set a long-term pricing benchmark for others, thus stalling the closure of trades/deals.”

The way around for the platform has been to work on deals selectively, which are more likely to be approved by the company.

Discounts in Indian private secondary markets

Market inquiries and discounts are also dependent on the runway a startup has, with a shorter runway being directly proportional to steep discounts on the price of secondary shares.

Deals being driven by fund houses

“Funds of 2015-16 vintage are already thinking of their Multiple on Invested Capital (MoIC) and Distribution to Paid-In Capital. It is natural for funds to evaluate exits after the fourth year of a fund spread over a seven plus two-year lifecycle,” says Sumir Verma, Founder and Managing Director at investment banking firm Merisis Advisors, which focuses on technology and consumer sector.

He adds that General Partner (GP – in charge of managing the fund portfolio) led secondaries are also on the rise, as funds look for liquidity. GPs select a few of their portfolio companies to create a basket on offer to secondary funds with the promise to manage them till the eventual exit.

“Typically, these portfolio companies are those that are not likely to go for a liquidity event in a short period of time, either because they are already profitable and don’t need money, or because of market conditions,” he says.

“The proceeds from such sales are then returned to the existing Limited Partners (LP – investor in the fund). Such deals could have higher discounts than a direct secondary, but funds are alright as liquidity is equally important and these portfolio companies are typically already returning more than the targeted hurdle rate,” Sumir says.

Merisis gave an exit to Fosun in two of its portfolio companies–Ixigo and Kissht–in the $30-50 million transaction bracket earlier this year.

Better times ahead?

The secondary market for private tech companies is likely to see only select deals closing over the next six months, designed mainly to give an exit to vintage funds and AIFs.

According to Qapita’s estimates, nearly $70 billion worth of transactions happened in the private market in India in FY22, of which nearly a third were from secondary trades, including Private Equity, Venture Capital, Family office, and HNI exits.

In the current fiscal, the overall deal pie is expected to shrink to around $40 billion due to a steep correction on account of valuation and deal volume. The company did not comment on the estimated contribution of secondary trade.

“Decision making on both sides has stalled, and is likely to be a temporary phenomenon, given the quantum of capital committed by PE funds to this geography,” says Skanda of Qapita Marketplace.

He adds, “The better run businesses and higher quality companies will be the first to go off the block and attract capital, and progressively it should cascade into the ecosystem as a whole.”

This is seconded by Ranjit Jha of Rurash Financials, who says the demand for secondaries is likely to be weak over the next six-odd months.

With large capital allocations and new funds committed to India, it is a matter of time for the markets to return to an even keel.

Edited by Megha Reddy