This is a user generated content for MyStory, a YourStory initiative to enable its community to contribute and have their voices heard. The views and writings here reflect that of the author and not of YourStory.

Is FinTech the Next Big Thing or a Flavour of the Season?

Decoding the wildly exciting collaboration between Finance and Technology

This is a user generated content for MyStory, a YourStory initiative to enable its community to contribute and have their voices heard. The views and writings here reflect that of the author and not of YourStory.

“Fintech is changing the finance sector just like the Internet changed the written press and the music industries. In what is a stagnant sector monopolized by banks, finance is ripe for innovation and fintech is unquestionably the catalyst needed for change.” - Philippe Gelis.

Overview

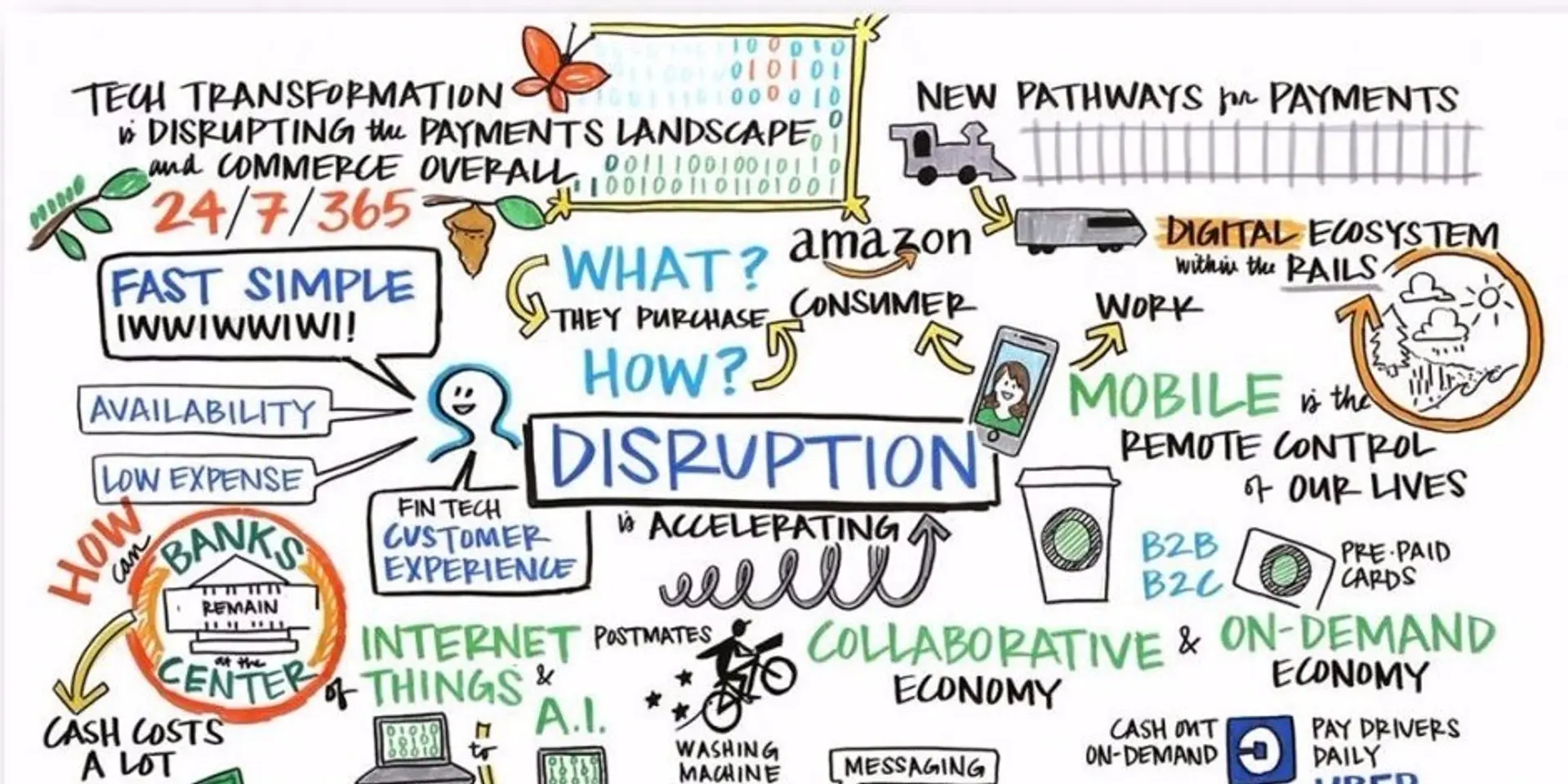

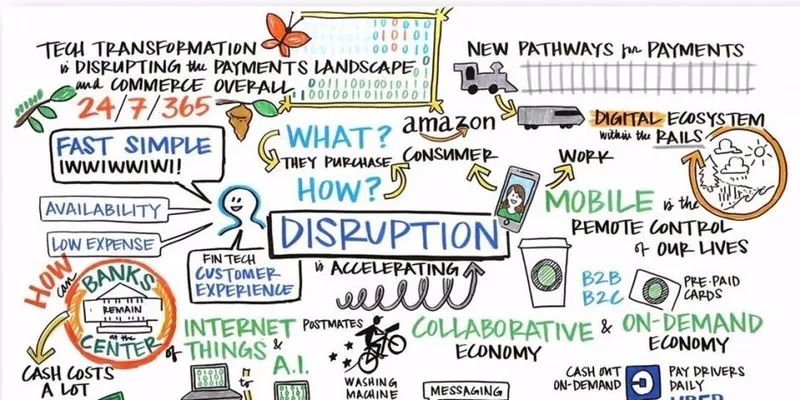

Fintech represents a novel cohort of progressive enterprises that leverage cutting edge technology to deliver financial products and solutions that are far more agile and innovative compared to conventional services provided by traditional financial institutions. It is, in essence, a new generation of tech-savvy firms backed by disruptive technologies such as behavioral and transactional analytics, machine learning, blockchain, biometrics, cloud, and mobile, that enables, compete and collaborate with orthodox market participants to reimagine the age-old processes, operating model, and infrastructure ultimately transforming the end user experience.

The FinTech sector which is time and again regarded as a battle between the old and the new, is perceived by many as the next wave of disruption that will change completely the way banking is done and financial services are rendered. FinTech start-ups have also been quicker than banks to take advantage of rapid advances in digital technology, forging path-breaking business models with a focus on customer-centric innovation, creating a new market that previously did not exist.

FinTech vis-à-vis BFSI – Disruptor, Distractor or Enabler

Fintech is stirring up Finance and everyone from banks, to retailers, to customers, are being impacted alike, and those that don't jump on the bandwagon will be rendered obsolete by the financial technology (r)evolution. Banks, which are not really known for being early adopters of state-of-the-art technologies are desperately trying to reposition themselves to survive the transition and slowly adopting a "can't beat them join them" mentality.

"Banking is necessary, banks are not." – Bill Gates

While one of the unique challenge faced by FinTech enterprises is to capture and cultivate innovation without compromising the integrity and preserving the stability of the BFSI network, the biggest challenge for long-established players is their organizational culture’s ability to embrace a collaborative approach with radical innovators and shake themselves out of institutional complacency. The strengths and weaknesses of both banks and FinTech start-ups signify that both will orchestrate a much-needed change and create a win-win situation for all by co-operating rather than competing. Such partnerships offer the ability for FinTech ventures to immediate scale, existing players to better serve customers, and consumers to reap the benefits of the new services at a cheaper cost.

“While the use of technology in finance is not new, nor are many of the products and services that are offered by new entrants to the sector, it is the novel application of technology and its speed of evolution that make the current wave of innovation unlike any we have seen before in financial services.” – World Economic Forum

Call it a disruption of technology or a distractor or a mere technological advancement, FinTech revolution is not just a flash in the pan or a buzzword du jour, rather a change agent digitally transforming the financial world by reimagining the way banking is done and finances are managed.

The Future of FinTech in India

India, which happens to be the fastest emerging and the third largest base of technology start-ups, is gradually moving up the FinTech growth ladder backed by robust ecosystem, the abundance of easy-to-hire tech talent, internet savvy customers and smartphone penetration. According to YourStory Research, in 2016, the Indian FinTech startup ecosystem witnessed more than USD 687 million poured into the space across 88 deals. While numbers highlight the immense potential of FinTech in India, there are several factors in play that support phenomenal growth.

• Technology and Internet Penetration – The pro-technology and innovation driven ecosystem is a key enabler in the growth of FinTech as the cost of starting a business have declined drastically backed by easier access to cutting edge technology, cloud-based storage, and availability of cheaper talent. Moreover, the surge in smartphone adoption, internet penetration, and growth of rural telephony further complements the already booming sector.

• Favorable Government Policy – The government’s widely publicized agenda of “Digital India”, flagship programs such as JAM (Jan Dhan, Aadhar, and Mobile), cashless payment tools such as UPI, BHIM, and BharatQR as well as the recent demonetization has turned the spotlight on the FinTech start-ups.

• Thrust on Financial Inclusion – It’s an open truth that India still has the largest share of the world’s unbanked population. Having said that, it is also the only country that is bridging the gap at a phenomenal pace, thanks to the strategic initiatives from the government and RBI such as the grant of Payments bank licenses, Direct Benefit Transfer (DBT).

• Massive Working Population – India’s young and tech-savvy working class provides a sizeable customer base to FinTech firms and have a far greater enthusiasm to avail services offered by such companies. Gone are the days when people had to bunk office and stand in queues, filling out piles of papers just to access a financial service.

• Needs of SME and Unorganized Sector – The SME and unorganized sector which usually finds it challenging to raise capital from banks due to stringent lending norms, longer processing times, ridiculously high interest rates and rigid terms and conditions can now raise smaller working capital loans much faster and cheaper.

Conclusion

FinTech is fast evolving as the most promising industry. Today, anyone with a smartphone can lend, borrow or invest money, make payments, seek financial advice and manage portfolios at the swipe of a screen. This presents significant growth opportunities for firms who are capable of developing sustainable and scalable business models, comprehensive financial products on a single platform with a customer centric engagement strategy while navigating the regulatory challenges, awareness and trust issues that they will eventually face.

Undoubtedly, FinTech is currently the most exciting business to be in, a multi-billion dollar opportunity offering tremendous potential to build the next financial behemoth (a la unicorns). According to a research report published by KPMG in India, the transaction value for the Indian FinTech sector is expected to reach a whopping USD 73 Billion by 2020 from the current approximate level of USD 33 Billion.

Even ice cream in the Bangalorean summer doesn’t melt that fast!

-------------------------------

The author also blogs at www.rupeshmaheshwari.com

Copyright © 2017: Rupesh Maheshwari. All Rights Reserved.