Zomato has greener pastures ahead

Operating in a duopoly, the food-tech unicorn thrives in an underpenetrated market – by global standards, which is slated to witness bumper growth.

As the count-down begins for Zomato’s Rs 9,375 crore initial public offering (IPO), opening on July 14 (Wednesday) with the price band of Rs 72-76 a share, brokerages have started doling out their recommendations by the dozen.

While a lot of brokerages have been sceptical about the ‘expensive valuations’ accorded to Zomato which has been loss-making, since its inception in 2010, analysts are not missing out on the growth opportunities that Zomato has on its way ahead, which would translate into gains for investors subscribing to Zomato’s IPO.

Mumbai-based Sneha Poddar, an equity research analyst at Motilal Oswal Financial Services, rightly highlighted that Zomato operates in a duopoly market, and has created strong entry barriers with a widespread network.

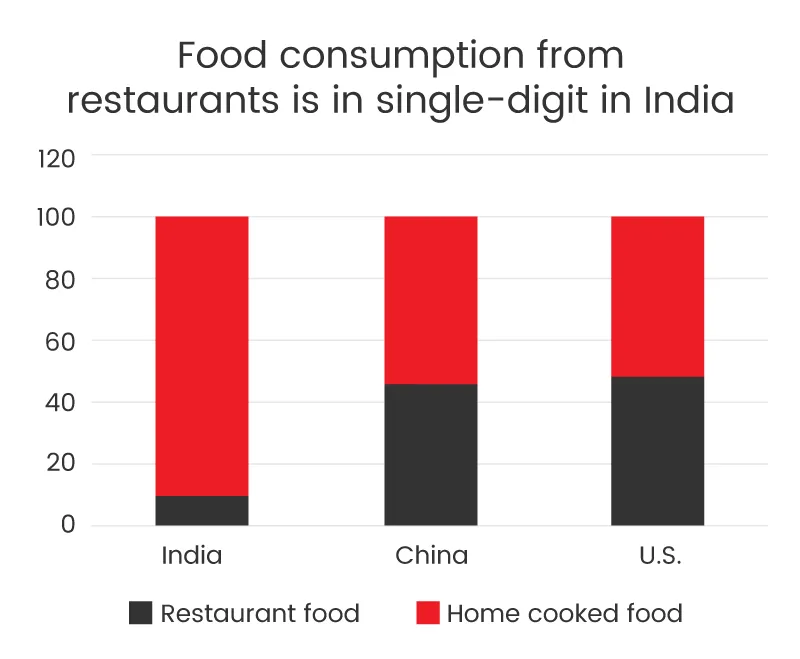

“It operates in a highly underpenetrated market where of the total food consumption in India, only 8-9 percent is from restaurants, of which only 8 percent is online food delivery,” Poddar penned in her recommendation note around Zomato’s IPO. “This is highly underpenetrated when compared it with bigwigs like US and China, where restaurant food - online food delivery matrix stands at 40-50 percent each.”

ALSO READ

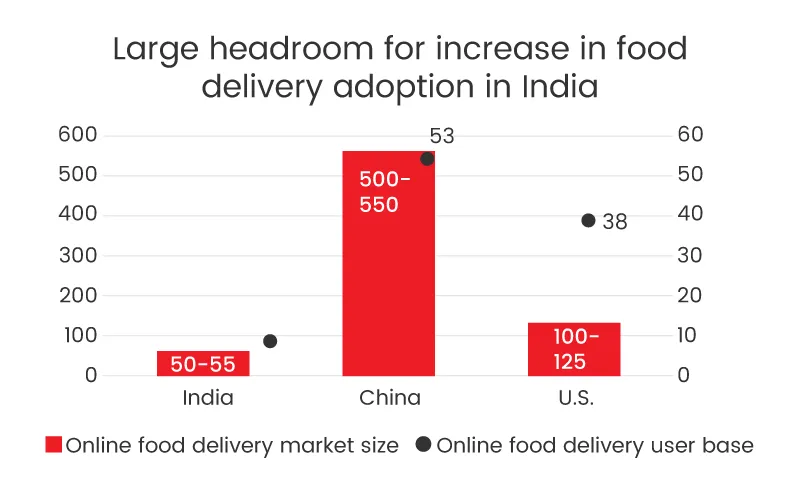

Poddar further pointed out the findings of RedSeer, the of-its-kind consulting firm which has an edge in understanding the consumer internet space. RedSeer has pegged the food services market in India to grow at a compounded annual growth rate (CAGR) of 9 percent from $65 billion in 2019 to $110 billion in 2025.

While food services in India is highly under-penetrated, it is likely to grow steadily, taking share away from home-cooked food as has been the trend in the past as well. Also, growth will be driven by changing consumer behaviour, reduced dependence of millennials on home-cooked food and kitchen set-up, increasing consumer disposable income and spending, and higher adoption among the smaller cities.

“Thus, the sector provides a huge opportunity for Zomato to grow,” Poddar asserted.

Poddar also added that Zomato with its first-mover advantage is placed in a sweet spot as the online food delivery market is at the cusp of evolution.

“It enjoys a couple of moats and with the economics of scale started playing out, the losses have reduced substantially,” Poddar said.

ALSO READ

And then comes the caveat from Poddar, who does not mince with words as she jots down that predicting the growth trajectory at this juncture is a little tricky for the next few years. Poddar uses enterprise value-to-sales ratio for the comparison.

Enterprise value-to-sales is the financial ratio that measures the cost to purchase the value of a business relative to its sales. A lower multiple indicates that the business is undervalued, and hence more attractive.

The valuation also appears expensive at 25 times enterprise value-to-sales for 2020-21, compared to an average of 9.6 times for global peers and 11.6 times for Indian quick service restaurants (QSRs.)

While there is merit in comparing Zomato to its global peers with a similar operating model, the QSR comparison makes for very little business sense.

Because, unlike the QSRs which demand a lot of management bandwidth and capital for operations as well as expansion, Zomato has a presence across 525 Indian cities and nearly 3.90 lakh active restaurant listings, both at the end of March this year.

Poddar does not seem to be ruling out these logical ends, as she affirmed that valuing such early-stage businesses on plain vanilla financial matrix might not give the right picture and may look distorted.

“Investors with a high-risk appetite can subscribe for listing gains, given fancy for unique and first of its kind listing in the food delivery business,” Poddar advised.

While analysts have a varying degree of reservations on Zomato’s valuations, none have opted to advise their investors to stay away from Zomato’s IPO. As such, a host of anchor investors are reported to have made beeline for buying a piece of Zomato ahead of the IPO, where the bids exceeded over 35 times the quantity reserved for anchor investors.